SPVs in Startup Fundraising: A Clear Guide for Founders

Key Takeaways

SPVs simplify cap table management by consolidating multiple small investments into a single entity on your cap table, reducing administrative overhead and making your startup more attractive to institutional investors in future funding rounds.

Access a broader investor base through SPVs by aggregating smaller checks from angel investors who might not meet minimum investment thresholds—Allied Venture Partners accepts investments as low as $1,000, democratizing startup investing.

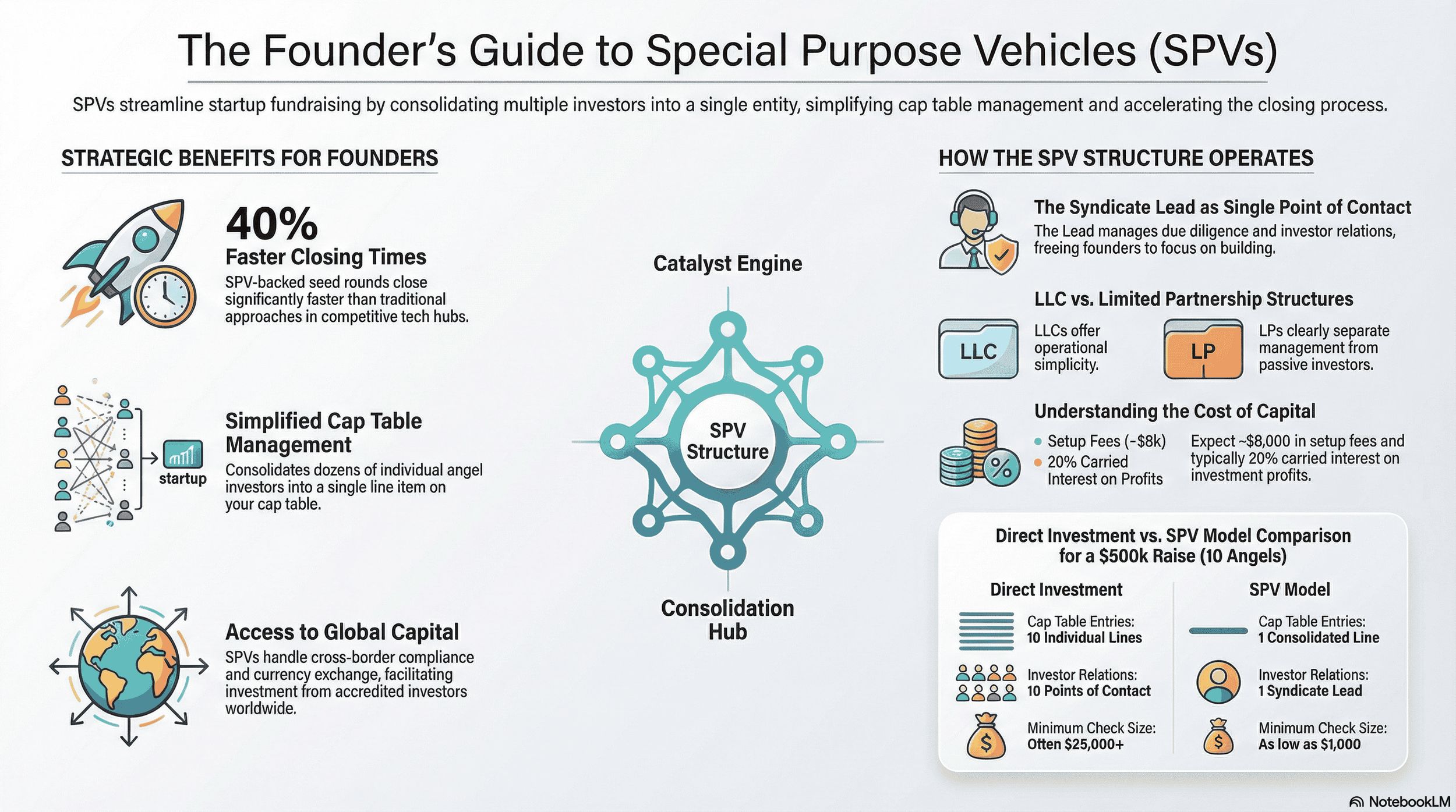

SPV-backed seed rounds close up to 40% faster than traditional approaches in competitive tech hubs, giving startups a speed advantage when quick capital deployment is critical.

Two primary legal structures dominate: Limited Liability Companies (LLCs) offer operational simplicity and pass-through taxation, while Limited Partnerships (LPs) clearly separate management (General Partner) from passive investors (Limited Partners).

Understand the cost structure: SPVs typically involve setup fees ($8,000 at Allied/AngelList), potential management fees (1-2% annually), and carried interest (typically 20% of profits), though costs should be weighed against benefits like faster closing and broader capital access.

The Syndicate Lead is your single point of contact, acting as fund manager to handle due diligence, investor relations, legal documentation, and ongoing compliance—freeing founders to focus on building their business rather than managing dozens of individual investors.

SPVs excel in specific scenarios: large numbers of small investors, bridge rounds, international fundraising, "friends and family" rounds, and pre-seed stages where speed and investor aggregation are paramount.

Not a one-size-fits-all solution: For very small rounds, single-lead investors, or when simplicity is paramount, direct investment may be more appropriate than introducing the SPV structure and associated costs.

Strategic value beyond capital: Smaller angels participating through SPVs often become powerful advocates, making customer introductions, assisting with hiring, and providing referrals to larger downstream investors.

Long-term benefits include cleaner exits: When your startup is acquired or goes public, distributing proceeds through a single SPV is far more efficient than managing distributions to hundreds of individual shareholders.

Global reach made simple: SPVs streamline international investments by handling foreign currency exchange, tax implications, and cross-border compliance—Allied Venture Partners now has 2,000+ LPs across two dozen countries.

Set minimum direct investment thresholds: Based on experience with dozens of SPVs, founders should consider requiring a $25,000 minimum for direct investments, pooling smaller checks into an SPV to minimize cap table complexity.

Introduction: Navigating the Fundraising Landscape with SPVs

Navigating the labyrinthine world of startup fundraising can feel like an expedition into uncharted territory for many founders. The journey from inception to securing growth capital is fraught with complexities, not least of which is managing investor relations and the ever-critical capitalization table. In this dynamic landscape, where global venture funding reached $91 billion in Q2 2025 [DemandSage, 2026], innovative financial instruments are crucial for success.

One such instrument that has gained significant traction is the Special Purpose Vehicle (SPV). While often discussed, the practical application and strategic benefits of SPVs for founders can remain elusive. This guide aims to demystify SPVs, providing a clear, actionable framework for founders to leverage them effectively in their fundraising efforts. We'll delve into what SPVs are, why they are becoming indispensable tools, how they operate, and crucially, when and how founders should consider integrating them into their capital-raising strategies. The aim is to equip you with the knowledge to transform fundraising complexities into opportunities for growth.

The Founder's Dilemma: Complex Cap Tables and Diverse Investors

Founders embarking on a fundraising journey quickly encounter a common set of challenges. The primary among these is the management of the capitalization table, or "cap table." As a startup secures its initial funding, typically from a diverse group of angel investors and early-stage venture capital firms, the cap table begins to proliferate. Each investor, no matter how small their check size, represents a unique entry, requiring individual tracking, communication, and administration. This can quickly become a significant administrative burden, diverting precious time and resources away from core business operations.

Beyond the sheer volume of entries, the diversity of investors presents its own set of hurdles. Angel investors, for instance, often invest smaller amounts than institutional venture capital funds. While crucial for early-stage momentum, aggregating a substantial sum from numerous individuals can lead to a highly fragmented ownership structure. This fragmentation complicates decision-making, future funding rounds, and even exit scenarios.

Furthermore, the landscape of potential investors is increasingly global, with accredited investors from various jurisdictions seeking opportunities in promising startups. Managing these international relationships, navigating different regulatory frameworks, and facilitating cross-border transactions adds another layer of complexity. The sheer number of individual investors, each with unique expectations and reporting needs, can strain a lean startup team. This is where innovative solutions like SPVs emerge as not just beneficial but often essential.

What This Guide Will Cover: Empowering Your Fundraising Strategy

This guide is designed to equip startup founders with a comprehensive understanding of Special Purpose Vehicles (SPVs) and their strategic application in fundraising. We will dissect the fundamental nature of an SPV, clarifying its definition and distinguishing it from more traditional investment structures like VC Funds. The guide will then pivot to the core value proposition for founders, detailing the many benefits SPVs offer, particularly in taming cap table management chaos, expanding the investor pool by aggregating angel investors and smaller checks, and facilitating deal syndication.

We will then delve into the operational mechanics of how SPVs function within the startup fundraising ecosystem, outlining the key players involved, from the fund manager to the Limited Partners (investors). The practical aspects of setting up and administering an SPV will be covered, including choosing the appropriate legal structure, navigating administrative steps, and managing investor onboarding and ongoing compliance.

Crucially, this guide provides a critical decision-making framework, exploring the ideal scenarios for SPV utilization and, equally important, situations where an SPV might not be the best fit. Finally, we will touch upon the potential challenges and how to mitigate them, as well as the long-term implications of using SPVs for a startup's future growth and fundraising trajectory. Our objective is to provide actionable insights that empower you to make informed decisions and enhance your fundraising success.

Understanding the Basics: What is a Special Purpose Vehicle (SPV)?

At its heart, a Special Purpose Vehicle (SPV) is a financial and legal entity created for a very specific, singular purpose. Unlike a broad investment fund that might hold a diversified portfolio of companies, an SPV is typically established to hold a single asset or engage in a single transaction. In the context of startup fundraising, this "special purpose" is almost invariably to make an investment in a particular company, often for a specific funding round. This dedicated nature is what sets SPVs apart and makes them such powerful tools for founders navigating complex investment scenarios.

Defining an SPV: A Dedicated Legal Entity for Investment

An SPV is essentially a legal entity designed to isolate financial risk and achieve specific transactional objectives. It can take various forms, such as a Limited Liability Company (LLC) or a Limited Partnership. The core idea is to create a distinct legal wrapper that acts as a conduit for investment.

Instead of a group of individuals directly investing in a startup, they collectively invest into the SPV, and the SPV, in turn, invests the aggregated capital into the startup. This legal entity shields the individual investors from direct liability beyond their investment amount and consolidates their holdings into a single entity from the startup's perspective. While the term "Special Purpose Entity" (SPE) is broader, in the startup world, "SPV" is the commonly used designation for these investment-focused vehicles.

SPV vs. Traditional VC Fund: Key Distinctions for Founders

Founders often draw parallels between SPVs and traditional VC Funds, but key distinctions are vital for strategic decision-making. A traditional VC fund is typically a large, pooled investment vehicle with a mandate to invest in a diversified portfolio of companies across various stages and sectors, often over a 10-12 year lifecycle [Forbes, 2022]. These funds are managed by professional fund managers who raise capital from institutional investors and high-net-worth individuals, known as Limited Partners.

An SPV, conversely, is usually established for a single investment opportunity. While a VC Fund seeks diversification, an SPV is laser-focused on a particular startup. This singular focus allows for greater agility and speed. For instance, SPV-backed seed rounds can close up to 40% faster than traditional approaches, especially in competitive tech hubs [AngelSchool.vc, 2025]. Furthermore, SPVs often offer quicker distribution of returns, with some SPVs distributing capital in approximately 2 to 3 years compared to the much longer horizon of traditional VC funds [Forbes, 2022]. This difference in scope, lifecycle, and investment strategy makes SPVs a distinct tool, often used to supplement rather than replace traditional VC financing.

Common Legal Structures for SPVs: LLCs and Limited Partnerships

The legal structure chosen for an SPV is critical and influences its governance, taxation, and operational flexibility. The two most prevalent structures for SPVs in startup fundraising are Limited Liability Companies (LLCs) and Limited Partnerships (LPs).

Limited Liability Companies (LLCs): LLCs are popular due to their flexibility. They offer limited liability protection to their members (the investors), meaning their personal assets are protected from business debts and liabilities. LLCs also offer pass-through taxation, where profits and losses are passed directly to the members and taxed at their individual rates, avoiding double taxation at the entity level. This structure is often favored for its administrative simplicity compared to LPs.

Limited Partnerships (LPs): An LP structure involves at least one general partner (GP) and one or more limited partners (LPs). The GP manages the SPV's operations and makes investment decisions, bearing unlimited liability (though this is often mitigated through other means or by the GP itself being an LLC). The LPs are passive investors who contribute capital and benefit from limited liability, with their risk capped at their investment amount. This structure is common when a professional fund manager or a more experienced investor takes the lead as the GP.

At Allied Venture Partners, we structure each of our investments as an SPV and use AngelList to manage all SPVs. AngelList syndicate SPVs are formed as Delaware series limited partnerships under a master Delaware limited partnership, with AngelList designated as the general partner (GP) and the limited partners (LPs) as investors. Our investment team at Allied, organized as a U.S. LLC, acts as the syndicate lead, making all investment decisions and advising AngelList on each company we invest in.

Why the "Special Purpose": Aggregating Investors for a Single Goal

The "special purpose" in SPV is the defining characteristic. It means the entity's existence is tied to a singular objective: to invest in a specific company for a specific funding round. This is particularly valuable when a startup needs to raise capital but faces the challenge of aggregating smaller investments from a large number of investors. For example, a startup might find itself with a strong interest from several angel investors willing to contribute $25,000 each, but not enough to meet its funding target with only these smaller checks. Instead of managing each individual investor, a syndicate lead (like Allied Venture Partners) can establish an SPV. This SPV then collects $25,000 contributions from multiple angels, consolidating them into a single, larger investment by the SPV into the startup. This aggregation streamlines the process for both the startup and the investors, creating a clear path for capital deployment towards a shared goal.

Why Founders Should Consider an SPV: Key Benefits in Fundraising

The adoption of SPVs in startup fundraising is not merely a trend; it's a strategic response to the evolving demands of the investment landscape. For founders, SPVs offer a compelling suite of advantages that can significantly smooth the fundraising process, broaden investor reach, and enhance operational efficiency. These benefits address some of the most persistent pain points faced by early-stage companies seeking capital.

Streamlining Cap Table Management: Conquering the Cap Table Chaos

One of the most significant advantages of using an SPV is its impact on cap table management. Without an SPV, a startup that raises, for instance, $500,000 from 10 individual angel investors would have 10 separate entries on its cap table. If these investors are accredited but not necessarily institutional, this can lead to complications in future funding rounds, shareholder communications, and ultimately, an exit.

An SPV consolidates these 10 individual investments into a single entry representing the SPV itself. This dramatically simplifies the cap table, reducing administrative overhead and making it cleaner and more manageable for the startup. This consolidation is especially valuable as companies scale and prepare for larger funding rounds, such as Series A or Series B, where sophisticated investors scrutinize cap table health. The median SPV on platforms like Carta managed $2.17 million in assets in 2023, an increase from $1.18 million in 2016, indicating the growing scale and importance of SPVs in managing these investments [Carta, 2024].

Aggregating Angel Investors and Smaller Checks: Expanding Your Investor Pool

SPVs are instrumental in democratizing access to startup investing for a broader range of investors, particularly angel investors. Many angels, while willing and able to invest, may not have the capital for the minimum check sizes typically required by institutional investors. An SPV allows a syndicate lead to pool smaller contributions from multiple angels to meet the startup's funding goals. This is particularly effective in sectors like technology, healthcare, fintech, and AI, which attracted 68% of angel investments in 2025 [CoinLaw, 2025]. For founders, this means access to a much larger pool of potential capital that might otherwise be out of reach. It transforms a fragmented group of smaller commitments into a substantial, consolidated investment, making the fundraising process more efficient and less demanding on the founding team's time.

At Allied Venture Partners, we have led and managed dozens of SPVs over the past six-plus years. We have seen firsthand the power of SPVs in enabling smaller angels to participate in startup investing. For instance, our minimum investment to participate in an Allied SPV is $1,000, opening the door to many high-value angels who might otherwise not be able to invest.

Sometimes, the smallest angels become the biggest advocates and supporters for a startup—making customer introductions, helping with sales and marketing, assisting with hiring, and providing referrals to larger downstream investors. In one instance, we saw an angel who participated in a company’s seed round with a $1,000 check make an introduction to a VC firm that led the company’s Series A round with a $400,000 investment. When it comes to angel investors, never discount someone based on the size of their check.

Facilitating Deal Syndication: Bringing Strategic Investors Together

Deal syndication, the process of bringing multiple investors together to fund a single deal, is significantly enhanced by SPVs. A syndicate lead can structure an SPV to bring together a mix of investors, including angels, family offices, and even smaller institutional funds, for a specific startup's funding round. This lead investor (often referred to as the General Partner or fund manager for the SPV) takes on the responsibility of due diligence, negotiation, and managing the investment on behalf of all participating Limited Partners. For the startup, this means dealing with a single point of contact for the entire syndicate, streamlining negotiations and legal documentation. This efficient approach is crucial in fast-paced fundraising environments where speed can be a significant competitive advantage.

Simplifying International Investments: Opening Doors to Global Capital

Navigating international fundraising can be a complex undertaking for startups due to varying legal, tax, and currency regulations. SPVs provide a structured way to onboard international investors. By establishing an SPV, a startup can effectively deal with one legal entity that handles the foreign currency exchange, tax implications, and compliance for its international backers. The SPV acts as a shield, absorbing the complexities of cross-border investment. This allows founders to tap into a global talent pool of accredited investors who might otherwise be deterred by the administrative hurdles of investing directly into a foreign company. This expands the potential funding base and can attract investors with unique strategic insights or market access relevant to the startup's growth.

For example, at Allied Venture Partners, we now have a global LP network of more than 2,000 people across two dozen countries. The power and breadth of this network runs incredibly deep, and it is almost always willing to help make introductions when a portfolio company expands into new geographies.

Maintaining Clean Investor Relations: A Single Point of Contact

One of the most immediate and tangible benefits for founders is the simplification of investor relations. When a startup raises capital through an SPV, it typically engages with the syndicate lead or the fund manager of the SPV. This single point of contact acts as the intermediary between the startup and the SPV's investors (the Limited Partners). Instead of managing communications, updates, and reporting for dozens or even hundreds of individual investors, the startup only needs to communicate with the SPV representative. This significantly reduces the administrative burden, frees up founder time, and ensures consistent messaging. This streamlined approach fosters stronger relationships with the SPV itself, which can be a valuable partner in subsequent funding rounds.

At Allied Venture Partners, our Managing Director, Matt Wilson, acts as the syndicate lead, working with founders and investors to facilitate streamlined communication. When a portfolio company shares an update with us, the founder only needs to provide it once, and we then share it with participating LPs (at the founder’s discretion). Likewise, when LPs have a question for the founder, those questions are first filtered and consolidated before being sent on, in order to protect the founder’s time.

How SPVs Work in Startup Fundraising: The Operational Mechanics

Understanding the operational framework of an SPV is crucial for founders to effectively partner with them and leverage their benefits. The mechanics involve several key players and a defined flow of capital and responsibilities. While SPVs offer simplicity from the startup's perspective, the underlying structure involves a clear division of roles and a structured investment process.

The Players Involved: Startup, SPV, Syndicate Lead, and Limited Partners

In a typical startup fundraising scenario involving an SPV, several parties play distinct roles:

The Startup: The company seeking to raise capital.

The SPV (Special Purpose Vehicle): The legal entity created specifically to invest in the startup. It's the direct investor in the startup.

The Syndicate Lead (or Fund Manager): This is often an experienced investor, a venture capital firm, an angel group leader, or a dedicated SPV service provider. The Syndicate Lead organizes the SPV, vets the investment opportunity, negotiates terms with the startup, and manages the SPV's operations. For the SPV, this role is akin to a General Partner (GP) in a Limited Partnership.

Limited Partners (LPs): These are the individuals or entities (e.g., angel investors, family offices, other accredited investors) who contribute capital to the SPV. They are the ultimate beneficiaries of the investment but typically have no direct involvement in managing the SPV or the startup.

The Syndicate Lead's Role: The General Partner of the SPV

The Syndicate Lead is the linchpin in the SPV structure. Acting as the de facto fund manager or General Partner, they are responsible for the entire process of setting up and operating the SPV. This includes identifying promising investment opportunities, conducting thorough due diligence on the target startup, negotiating the investment terms (share price, valuation, etc.), and presenting the deal to potential Limited Partners. They also handle the legal setup of the SPV, manage investor onboarding, and ensure ongoing compliance. For the startup, the Syndicate Lead is the primary point of contact, streamlining negotiations and communication. Their expertise is invaluable in structuring the deal and bringing the necessary capital together.

The Investment Flow: From Limited Partners to Your Startup

The capital flow in an SPV-backed fundraising round is a structured progression. First, potential investors (Limited Partners) commit capital to the SPV. This commitment is often formalized through a subscription agreement. Once sufficient commitments are secured, the SPV, through its Syndicate Lead, transfers the aggregated capital to the startup. The startup then issues shares or its equivalent equity instrument to the SPV, not to each individual investor. This single transaction simplifies the startup's cap table. When the startup eventually achieves a liquidity event (e.g., acquisition or IPO), the proceeds are first distributed to the SPV. The SPV, in turn, then distributes the net proceeds to its Limited Partners according to their respective ownership stakes, after accounting for fees.

Carried Interest and Management Fees: Understanding the Cost Structure

Like traditional VC Funds, SPVs involve costs associated with their operation and the management of investments. These typically include:

Management Fees: The fund manager or Syndicate Lead may charge an annual management fee, often around 1-2% of the committed capital, to cover operational expenses and compensate for ongoing management.

Carried Interest ("Carry"): This is a share of the profits generated by the investment, typically paid to the Syndicate Lead or fund manager upon a successful exit. It's commonly structured as 20% of the profits above a certain threshold (the "hurdle rate"). This aligns the interests of the manager with those of the investors.

SPV Setup and Administration Fees: There are initial costs associated with setting up the SPV's legal structure, legal documentation, and ongoing administration. These can range from a few thousand dollars to a percentage of the investment amount, depending on the complexity and the service provider. Some platforms charge between 2.5% to 4% of the investment as an admin fee.

Founders must understand these costs as they can impact the net capital received by the startup and the overall return for investors. At Allied Venture Partners, we do not charge a management fee. We only charge 20% carried interest as a success fee if the investment returns a profit to investors, plus a flat, one-time setup fee of $8,000 (charged by AngelList) to cover the initial SPV formation and ongoing administration.

Legal Documents and Agreements: What Founders Need to Know

Several key legal documents govern the relationship between the startup, the SPV, and its investors:

Subscription Agreement: This is the contract between an individual investor (LP) and the SPV, where the investor commits a specific amount of capital and agrees to the terms of the SPV's investment.

SPV Operating Agreement (or Partnership Agreement): This document outlines the internal governance of the SPV, defining the roles and responsibilities of the Syndicate Lead (GP) and the Limited Partners, how decisions are made, and how profits and losses are distributed.

Investment Agreement (or Term Sheet): This is the agreement between the startup and the SPV, detailing the terms of the investment (valuation, equity stake, investor rights, etc.), similar to what a startup would negotiate with a direct investor.

Private Placement Memorandum (PPM): For more formal SPVs, especially those involving a larger number of investors or crossing jurisdictional boundaries, a PPM may be required. This document provides detailed information about the investment opportunity, the risks involved, and the SPV's structure, akin to a prospectus for public offerings.

If you’re setting up your own SPV as a founder, we highly recommend working closely with legal counsel to ensure all documents are properly drafted and aligned with your fundraising objectives. If you’re working with a syndicate lead, such as Allied Venture Partners, these documents are created and managed by our SPV administrator, AngelList.

Setting Up an SPV: A Practical Guide for Founders

While the Syndicate Lead typically handles the intricacies of SPV formation, founders need to understand the key steps and considerations involved. This knowledge empowers them to select the right lead, collaborate effectively, and ensure a smooth setup process.

Choosing the Right Legal Structure: LLCs vs. Limited Partnerships

As previously discussed, LLCs and Limited Partnerships are the primary legal structures for SPVs. The choice often depends on the Syndicate Lead's preference and the nature of the investor base. An LLC might be chosen for its operational simplicity and pass-through taxation benefits, making it attractive for smaller, more direct angel syndicates. A Limited Partnership is often preferred when a professional fund manager is acting as the GP, as it clearly delineates responsibilities between the managing partner and passive investors. Founders should understand which structure is being used and any implications for governance or taxation, though the primary responsibility for this decision typically lies with the Syndicate Lead.

Key Administrative Steps: Incorporation, EIN, and Bank Account

Once the legal structure is decided, the SPV must be formally established as a legal entity. This involves:

Incorporation/Formation: Filing the necessary documents with the relevant state or jurisdiction to legally form the LLC or LP.

Obtaining an Employer Identification Number (EIN): The SPV needs its own tax identification number from the IRS, distinct from the startup's or the Syndicate Lead's.

Opening a Bank Account: A dedicated bank account is essential for the SPV to receive funds from Limited Partners and disburse them to the startup. This ensures clear financial separation and transparency.

These administrative steps are crucial for the SPV to operate legitimately and professionally.

Essential Legal Documentation: Operating Agreements and Investment Contracts

Beyond the formation documents, the SPV needs its governing legal agreements. The Operating Agreement (for LLCs) or Partnership Agreement (for LPs) dictates how the SPV will be run internally. Simultaneously, the Syndicate Lead negotiates the Investment Agreement with the startup. This contract specifies the terms of the investment from the SPV into the startup. Founders must ensure these agreements accurately reflect the negotiated deal terms and are legally sound. Working with experienced legal counsel is paramount during this phase.

Managing Investor Onboarding: Accreditation and Capital Calls

A critical part of the SPV setup is onboarding the Limited Partners. This involves:

Accreditation Verification: For most private investments in startups, investors must meet the definition of an accredited investor as defined by securities regulations. The SPV's manager is responsible for verifying that each LP qualifies.

Capital Calls: Once the SPV is set up and the investment terms are agreed upon, the Syndicate Lead will issue "capital calls" to the Limited Partners. This is a formal request for them to wire their committed funds to the SPV's bank account, typically for the amount needed for the investment round.

Efficient management of these processes ensures the timely deployment of capital.

Ongoing SPV Administration: Reporting, Tax Filings (K1 Forms), and Compliance

The SPV's responsibilities don't end after the investment. The Syndicate Lead or their designated administrator must handle ongoing tasks:

Investor Reporting: Providing regular updates to Limited Partners on the startup's progress, financials, and any significant developments.

Tax Filings: SPVs are typically pass-through entities, meaning they don't pay corporate income tax. Instead, profits and losses are passed through to the LPs, who then report them on their individual tax returns. The SPV must issue K1 forms to each LP detailing their share of income, deductions, and credits.

Compliance: Ensuring the SPV adheres to all relevant securities laws and regulatory requirements, particularly concerning investor communications and solicitations.

Founders should be aware of these ongoing administrative requirements, even though the direct burden usually falls on the SPV manager.

When to Use an SPV (and When Not To): A Founder's Decision Framework

The decision to utilize an SPV for fundraising is strategic and should be based on a clear assessment of its benefits against potential complexities and costs. SPVs are powerful tools, but they are not universally applicable. Understanding when they are most effective, and when simpler approaches suffice, is key to optimal capital raising.

Ideal Scenarios for SPV Utilization: Specific Fundraising Use Cases

SPVs shine in several specific fundraising contexts:

Large Number of Small Investors: When a startup anticipates securing capital from many angel investors or small funds, an SPV drastically simplifies cap table management.

Bridge Rounds: For companies needing to raise capital quickly between larger funding rounds, an SPV can expedite the process.

Specific Strategic Investors: If a startup is targeting a particular strategic investor who prefers investing via an SPV, or if multiple strategic investors want to co-invest in a specific deal.

International Investor Base: To streamline onboarding and compliance for accredited investors from different countries.

Accelerated Seed Rounds: SPV-backed seed rounds can close significantly faster, which is crucial for startups in competitive markets [AngelSchool.vc, 2025].

"Friends and Family" Rounds: For founders looking to raise from a broad network of acquaintances and family members, an SPV can provide structure and professionalization.

Pro tip: Based on our experience running dozens of SPVs at Allied Venture Partners, we recommend that founders set a minimum direct investment of $25,000 for any individual investor; smaller checks are best pooled into an SPV to reduce cap table clutter and administrative complexity. If you're unsure, learn more about our roll-up offering to help minimize cap table complexity.

When an SPV Might Not Be the Best Fit: Simplicity Over Complexity

Despite their advantages, SPVs introduce an extra layer of structure and cost that might be unnecessary or detrimental in certain situations:

Very Small Funding Rounds: If a startup is only raising a small amount from one or two investors, setting up an SPV would add unnecessary complexity and expense.

Sole Investor or Lead Investor: When a single investor (like a prominent VC) is leading the round and taking a significant stake, directly negotiating with that investor is often more straightforward.

Founders Prioritizing Absolute Simplicity: If a founder highly values minimal administrative overhead and has a clear path to securing funding from a few direct investors, an SPV might be overkill.

High Cost Sensitivity: The fees associated with SPVs (setup, management, legal) can add up. If the cost significantly outweighs the benefits for a particular round, alternative methods may be preferable.

Existing Complex Structures: If the startup already has intricate ownership structures, adding another layer might not be the most efficient solution.

A careful cost-benefit analysis, considering the size of the round, the number and type of investors, and the startup's stage, is essential.

Potential Challenges and Mitigation Strategies

While SPVs offer significant advantages, founders should be aware of potential challenges and proactively plan to mitigate them. Approximately 90% of startups ultimately fail [Startup Genome, 2019], making careful financial planning and risk management paramount, and SPVs are no exception.

One primary challenge is the cost. SPVs incur setup fees, administrative costs, and potentially management fees and carried interest for the Syndicate Lead. These costs reduce the net capital received by the startup and the ultimate return for investors. Mitigation involves selecting a Syndicate Lead and service provider with transparent and reasonable fee structures, and ensuring the benefits of using an SPV (like faster closing or access to more capital) outweigh these expenses.

Governance and control can also be a concern. While the SPV streamlines investor relations, the Syndicate Lead, acting as the GP, wields significant influence. Founders must conduct thorough due diligence on potential leads to ensure alignment in vision and strategy. A strong, experienced lead can be an invaluable asset, but a misaligned one can create friction.

The administrative burden, while reduced compared to managing individual investors, is not entirely eliminated for the startup. The founder still needs to manage communication with the SPV, provide necessary information, and ensure compliance. This requires active engagement with the SPV manager, not passive delegation.

Finally, regulatory considerations are paramount. For private markets professionals, responding to regulatory changes is a major challenge when setting up and running SPVs, particularly in Europe [CSC Blog, 2024]. Founders and their chosen SPV managers must ensure strict adherence to securities laws and reporting requirements to avoid legal repercussions.

Choosing an SPV Provider/Administrator

Selecting the right SPV provider or administrator is as crucial as choosing the right Syndicate Lead. These platforms offer varying levels of service, from pure legal formation to comprehensive investor management and reporting. When evaluating platforms like Carta, Sydecar, AngelList, Vauban, or Vestd, founders and their leads should consider:

Efficiency and Speed: How quickly can they set up and manage the SPV?

Cost Structure: Transparency on all fees, including setup, administration, and any platform fees.

Investor Experience: The platform's ease of use for LPs in subscribing, funding, and receiving updates.

Compliance and Legal Support: The provider's expertise in navigating regulatory requirements.

Reporting Capabilities: The quality and frequency of reports provided to both the startup and the LPs.

Integration: How well does the platform integrate with other cap table management or accounting software?

Some founders opt for a "DIY" approach with legal counsel and a dedicated administrator for maximum control, while others leverage full-service platforms for comprehensive support. The decision depends on the startup's internal resources, the complexity of the deal, and the chosen Syndicate Lead's preferences.

Pro tip: Based on our experience running dozens of SPVs at Allied Venture Partners, we recommend choosing a full-service platform with transparent fees and pricing, rather than simply optimizing for the lowest-cost administrator. In our view, partnering with a slightly more expensive but well-established SPV administrator, such as AngelList, is well worth the additional cost. Think of it as peace-of-mind insurance: you’re working with a provider that is unlikely to go out of business and is less inclined to cut corners to save on costs.

Long-Term Impact of SPVs

The decision to use an SPV extends beyond the immediate fundraising round and can shape a startup's future trajectory. The clean cap table generated by an SPV simplifies subsequent funding rounds. Venture capital firms often prefer companies with manageable cap tables, as it reduces their due diligence efforts and potential complications in negotiations. This can lead to smoother and faster future fundraising processes.

Furthermore, the SPV structure can impact liquidity events. When a startup is acquired or goes public, distributing proceeds through a single SPV is far more straightforward than managing distributions to dozens or hundreds of individual investors. This efficiency can accelerate exit processes.

The evolution of SPVs is also worth noting. As the financial landscape shifts, technologies like tokenization and blockchain are beginning to be explored for SPV administration, promising even greater efficiency and transparency. While traditional methods remain dominant, understanding these emerging trends can position startups for future innovation in capital raising.

Summary: What Are SPVs in Startup Fundraising?

Special Purpose Vehicles (SPVs) have emerged as a powerful and increasingly indispensable tool in the modern startup fundraising arsenal. For founders navigating the inherent complexities of securing capital, SPVs offer a strategic advantage by streamlining cap table management, aggregating diverse pools of investors (including crucial angel investors), facilitating deal syndication, and simplifying international investments. They transform a fragmented landscape of individual backers into a cohesive, single investment entity, thereby reducing administrative burdens and freeing up valuable founder time.

While the operational mechanics of SPVs involve key players like the Syndicate Lead acting as a fund manager and the collective capital of Limited Partners, their core benefit lies in simplification. Understanding the common legal structures like LLCs and Limited Partnerships, the investment flow, and the associated costs such as carried interest and management fees, is crucial for founders to engage effectively. The practical steps of setting up an SPV, managing investor onboarding, and ensuring ongoing compliance are typically managed by the Syndicate Lead or a dedicated administrator, but founders must be aware of these processes.

Critically, SPVs are not a one-size-fits-all solution. Founders must employ a strategic decision-making framework to determine if an SPV is indeed the right choice for their specific fundraising needs, weighing its benefits against the associated costs and complexities. By thoughtfully considering ideal use cases—such as rounds with numerous small investors or the need to tap into global capital—against scenarios where simpler approaches suffice, founders can optimize their capital-raising efforts. Proactively addressing potential challenges, such as fees and governance alignment, and diligently selecting a reputable SPV provider or administrator, will further enhance the effectiveness of this financial instrument. Ultimately, when strategically deployed, SPVs empower startups to access capital more efficiently, build stronger investor relationships, and lay a more robust foundation for future growth and liquidity. Mastering the nuances of SPVs is an investment in a smoother, more successful fundraising journey.

Frequently Asked Questions About SPVs in Startup Fundraising

General SPV Questions

What is an SPV and how does it work in startup fundraising?

A Special Purpose Vehicle (SPV) is a dedicated legal entity created to make a single investment in a specific startup or funding round. Unlike traditional funding sources such as venture capital funds that invest across multiple companies, an SPV pools capital from multiple investors (Limited Partners) and deploys it as one consolidated investment. This structure appears as a single entry on the startup's cap table, dramatically simplifying investor management while enabling participation from angels who might not meet minimum check sizes for direct investment.

Are SPVs only used in startup fundraising, or can they be used in other contexts like real estate?

While this guide focuses on startup fundraising within the startup ecosystem, SPVs are versatile vehicles used across many investment types. They're commonly deployed in real estate transactions, structured finance deals, and private equity investments. The fundamental principle remains the same: creating a dedicated legal entity for a specific investment purpose, whether that's acquiring a commercial property, funding a startup's pre-seed round, or participating in a corporate acquisition.

How do SPVs differ from traditional corporations or Limited Liability Partnerships?

SPVs are typically structured as LLCs or Limited Partnerships rather than traditional corporations, primarily for tax efficiency and flexibility. Unlike corporations that may face double taxation, SPVs usually employ pass-through taxation where profits and losses flow directly to investors. While Limited Liability Partnerships serve similar asset protection purposes, SPVs are uniquely designed for a single investment objective. The governance rules for SPVs are also simpler, with a clear division between the Syndicate Lead (General Partner) and passive Limited Partners, whereas corporations have more complex board structures and shareholder voting requirements.

Structure and Setup

What are the most common legal structures for SPVs?

The two primary structures are Limited Liability Companies (LLCs) and Limited Partnerships (LPs). LLCs offer operational simplicity and pass-through taxation, making them popular for smaller angel syndicates. Limited Partnerships feature a General Partner who manages operations and Limited Partners who are passive investors with liability capped at their investment amount. At Allied Venture Partners, we use Delaware series limited partnerships under a master Delaware limited partnership, with AngelList as the General Partner. The choice between structures depends on the deal flow complexity, investor base, and the Syndicate Lead's preference.

Can SPVs be used as roll-up vehicles to consolidate existing investors?

Yes, SPVs can function as roll-up vehicles to clean up cap tables by consolidating multiple existing small investors into a single entity. This is particularly valuable when a startup is preparing for a Series A or later funding round and institutional investors flag cap table complexity as a concern. Allied Venture Partners offers a roll-up service specifically designed to minimize cap table complexity by pooling smaller existing shareholders into one SPV entry, making future fundraising smoother and reducing ongoing administrative burden.

What documents do I need to sign, and can I use an electronic signature?

Key documents include the Subscription Agreement (between investors and the SPV), the Operating Agreement or Partnership Agreement (governing the SPV internally), and the Investment Agreement (between the SPV and your startup). Most SPV administrators, including platforms like AngelList, support electronic signature for all documents, streamlining the process significantly. This digital approach accelerates the closing timeline, which is why SPV-backed seed rounds can close up to 40% faster than traditional approaches in competitive tech hubs.

Costs and Economics

What fees are associated with SPVs, and what is carried interest?

SPVs typically involve three types of costs: setup/administration fees (ranging from a few thousand dollars to 2.5-4% of investment), management fees (often 1-2% annually of committed capital), and carried interest. Carried interest is a performance fee—typically 20% of profits above a certain threshold—paid to the Syndicate Lead upon a successful exit. This aligns the lead's interests with investors, as they only profit when the investment generates returns. At Allied Venture Partners, we charge 20% carried interest as a success fee plus a flat $8,000 setup fee, but no ongoing management fees.

How does the regulatory treatment of SPVs affect tax implications and capital gains?

SPVs are typically structured as pass-through entities for favorable regulatory treatment. This means the SPV itself doesn't pay corporate income tax. Instead, profits, losses, and capital gains flow through to the Limited Partners, who report them on their individual tax returns. The SPV issues K-1 forms annually to each investor detailing their share of income, deductions, and capital gains. This structure avoids double taxation and provides tax efficiency, though investors should consult their tax advisors about how capital gains from startup exits will be treated based on their individual circumstances and holding periods.

Strategic Considerations

When should a founder consider using an SPV versus other funding sources?

SPVs are ideal when you're raising from numerous small investors (especially in a pre-seed round or seed stage), need to accelerate a bridge round, want to tap international capital, or are aggregating "friends and family" investments. They're particularly effective for crowdfunding-style raises where you're accessing broader angel networks. However, if you're raising a small amount from one or two institutional investors, or a single lead investor is taking a significant stake, direct investment is typically simpler and more cost-effective than introducing the SPV structure.

How do SPVs facilitate strategic partnerships and joint ventures?

SPVs can serve as vehicles for strategic partnerships by bringing together investors who offer more than just capital—such as industry expertise, market access, or operational support. When multiple strategic investors want to co-invest in a specific deal, an SPV provides structure for this joint venture while maintaining a clean cap table for the startup. The Syndicate Lead can curate a group of Limited Partners who collectively bring strategic value, creating a powerful network effect that benefits the startup beyond the financial investment alone.

What investment risk considerations should founders and investors understand about SPVs?

The primary investment risk factors mirror those of direct startup investing—approximately 90% of startups ultimately fail—but SPVs add specific considerations. Investors must trust the Syndicate Lead's judgment and due diligence, as they have limited governance rights. Fees can reduce net returns, and the concentrated exposure to a single company means no diversification within the SPV itself. For founders, misalignment with the Syndicate Lead or excessive costs can be problematic. However, experienced leads often add value through due diligence, terms negotiation, and ongoing support that can actually reduce overall investment risk compared to fragmented individual investors making isolated decisions.

Operational Questions

How does an SPV affect deal flow and future fundraising rounds?

SPVs positively impact deal flow and future fundraising in several ways. The clean cap table they create makes your startup more attractive to institutional investors in later rounds, as VCs prefer companies with manageable shareholder structures. This can accelerate Series A and beyond by reducing due diligence complexity. Additionally, a well-connected Syndicate Lead can improve your deal flow by making introductions to downstream investors—we've seen cases where a $1,000 angel investor in an Allied SPV introduced a company to a VC that led their Series A with a $400,000 investment.

Can SPVs be used across different sectors beyond technology startups?

Absolutely. While our guide focuses on tech startups, SPVs are versatile structures used throughout the private equity landscape and beyond. They're common in real estate syndication, structured finance transactions, healthcare ventures, and even creative industries. In 2025, technology, healthcare, fintech, and AI attracted 68% of angel investments, but SPVs can effectively aggregate capital for any sector where multiple investors want exposure to a specific opportunity. The fundamental mechanics—pooling capital, simplifying administration, and providing limited liability—apply universally across investment contexts.

What ongoing governance rules and compliance requirements apply to SPVs?

SPVs must adhere to securities regulations, including accredited investor verification requirements and proper investor solicitation practices. The Syndicate Lead handles ongoing governance rules such as regular investor reporting, annual K-1 tax form distribution, and maintaining corporate formalities. Responding to regulatory changes is particularly important—it's noted as a major challenge for private markets professionals running SPVs, especially in Europe. The SPV must also comply with any investor rights provisions in the Operating Agreement, maintain proper books and records, and ensure all communications with Limited Partners meet regulatory standards for private placements.

Disclaimer: This article is provided for general informational and educational purposes only and does not constitute legal, financial, investment, tax, or professional advice of any kind. Allied Venture Partners LLC makes no representations or warranties regarding the accuracy, completeness, or currentness of this information, which is subject to change without notice. To the fullest extent permitted by law, Allied Venture Partners LLC, its affiliates, officers, directors, employees, and agents expressly disclaim all liability for any direct, indirect, incidental, consequential, special, or punitive damages arising from your use of or reliance on this content, including but not limited to any securities offerings, capital raises, regulatory compliance issues, enforcement actions, financial losses, or business damages. Securities laws are complex, fact-specific, and vary by jurisdiction. You are solely responsible for ensuring compliance with all applicable federal and state securities laws and should consult with qualified legal counsel, financial advisors, and tax professionals licensed in your jurisdiction before making any decisions or taking any actions based on this information. By accessing or using this article, you acknowledge that you have read and understood this disclaimer, assume all risks associated with your use of this information, and agree to indemnify and hold harmless Allied Venture Partners LLC from any claims arising from your use of this content.