Annual Investor Letter 2023

Friday, December 22, 2023

To the Founders, Investors, and Partners of Allied VC,

Thank you for another great year of support and enthusiasm as we continued scaling Allied Venture Partners during the most challenging venture market of the past decade.

Allied is an amalgamation of the best practices I have learned as an angel and scout over the past ten years, so seeing it come to life and receiving such a positive response from founders and investors is inspiring.

I know you're quite busy, so I'll do my best to keep this brief. In line with my format from previous letters, there are three key topics I'd like to cover in this update:

Syndicate Metrics, Outlook & Portfolio Construction

The Current State of Markets (Public & Private)

Looking Forward: Phase Two, Phase Three

1) Syndicate Metrics, Outlook & Portfolio Construction

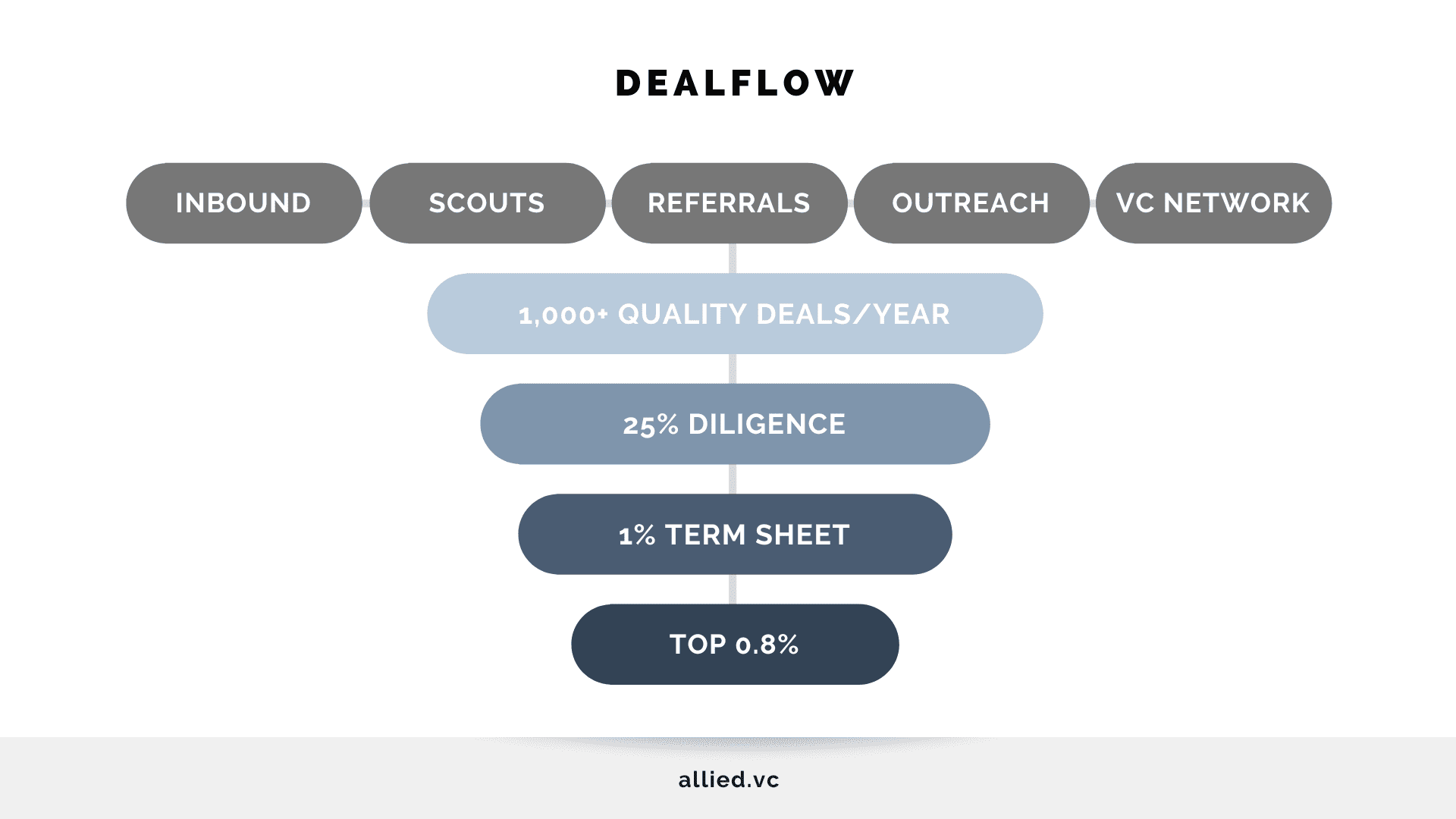

Allied Venture Partners boasts a whopping 1,700+ members, with investors from over two dozen countries. Since 2020, we’ve deployed more than $5M into 16 companies across Canada, the United States and Australia. Our Scout and Advisory programs have proven to be an unparalleled success, establishing a dealflow flywheel that is robust and diversified.

In 2023, we saw more than 1,000 investment opportunities across North America and chose to invest in the top 0.8%. For your reference, I’ve included a breakdown of our five-part dealflow funnel:

I’m very grateful for those of you who continue sharing unique investment opportunities from across your networks. Without you, Allied would not exist.

Regarding our 2023 investment progress, Allied raised and deployed over $550k, making five investments into five companies (including three first-time Seed investments and two follow-ons at Series A). These investments were part of an overall $10M in total funds raised by our founders.

These companies include:

In June, Allied members also had the exclusive opportunity to participate in an ownership syndicate for an NHL hockey team. However, this was a unique one-time opportunity and not part of our normal investing activities.

Additionally, two investments were canceled due to the founder pivoting the business, thus placing fundraising on hold.

As you’ll recall from our investment mandate, I aim to add between four and six new companies to the Allied portfolio each year. Although we only added three new companies in 2023, I’m satisfied with a slower deployment, given the volatility we saw in markets over the past 12 months. Furthermore, I leveraged this downtime to visit our Founders in Toronto, Austin, Sydney, Miami, and Boston.

Regarding performance, our thesis of co-investing alongside high-profile investors continues to execute well. This year, we co-invested alongside notable firms such as MGV Capital, DraftKings, MCMA Ventures, Techstars, Harvard Business School Angels, Hilltop Ventures, Hustle Fund, AngelList, the US Department of Defence, and Academy Award-winning actor Kevin Costner. We were also very excited to see one of our companies receive an offer from Kevin O’Leary on Shark Tank, and another company raise capital from an owner of the New York Yankees.

Among our two follow-on investments, we were fortunate to participate in a significant markup of 3.2x after just 16 months from our initial investment.

To reiterate our mandate, my goal is to operate Allied with the diligence and discipline of a top-tier VC fund yet with the flexibility of a syndicate. As such, I feel that our disciplined, thesis-driven approach, adhering to our core investment values, has held up well against recent market volatility.

However, we are in the business of early-stage venture investing, so if we don’t experience some losses, I’m likely not doing my job correctly. In Q4, I shared the news that one of our founders made the difficult decision to close their company.

Without revealing too many details publicly, when we first invested, the company was experiencing tremendous growth of 3x QoQ and nearly $250k ARR. However, the unprecedented headwinds of 11 interest rate increases since March 2022 made it increasingly difficult for the company to sustain its growth trajectory while operating efficiently.

Despite adverse market conditions, the founder displayed unwavering dedication and made every possible effort to save the business.

For anyone who has ever built a company, you pour your heart and soul into something for years only to risk being devastated personally, professionally, and financially if it doesn’t work out. I commend every entrepreneur brave enough to take this leap and look forward to being the founder’s first phone call when they start their next company.

As for Allied, I shared a detailed postmortem with investors. In hindsight, I knew inflation and higher interest rates were coming, but I never would have guessed a 21x increase in 18 months.

Regardless, moving forward, I recognize the importance of assessing the broader macro environment and its potential impact on our portfolio companies. I will dedicate more time and resources to analyzing the macroeconomic factors that could significantly influence the industries in which our companies operate.

Once again, I want to express my sincere appreciation for your trust and partnership. I am dedicated to continuously improving our investment practices to maximize value for our limited partners.

In 2024, I remain focused on finding unique opportunities that others have overlooked and then doubling down as they break out. We currently have several exciting opportunities in the pipeline that I look forward to sharing with you in the coming weeks.

2) The Current State of Markets (Public & Private)

Just when we thought we had seen it all in 2022, along came the roller coaster that was 2023.

The FTX fallout in November’22 continued to roil digital asset prices well into the New Year. This was further exacerbated by the SVB collapse and subsequent regional banking crisis in Q1. Thankfully, the broader banking system avoided contagion through the Federal Reserve’s swift and decisive intervention.

Additionally, in the first half of 2023, we saw four more interest rate increases as the US Fed continued its ongoing battle with inflation. It was a strange inverse of conditions where markets cheered negative economic data as a sign of cooling inflation. Nevertheless, this rise in interest rates has helped remove excess liquidity that caused asset prices to bubble in 2021.

Amidst this volatility, public technology stocks rebounded strongly in the second half, closing the year up over 60% on a backdrop of two regional wars in Eastern Europe and the Middle East. It appears we’ve reached peak interest rates, and markets have responded favorably.

Looking forward, I would prefer not to see any rate cuts until at least Q4’24, thus avoiding a premature decrease. However, as history tells us, the US Fed doesn’t have the best timing. Coupled with the upcoming US Presidential Election, we could see pressure for a rate cut as early as Q2.

What I’m Seeing in Private Markets

Regarding private markets, growth and pre-IPO valuations continued their decline throughout the year. Higher interest rates and fallout from crossover funds like Tiger and Softbank imploded the IPO market and caused a valuation reset down the entire funding stack.

Some VCs have stated that valuations at pre/seed have yet to normalize. However, I disagree with this sentiment and have a theory as to why certain VCs are stuck playing in an overpriced market.

Firstly, I’ve noticed that this type of commentary has come predominantly from larger firms with nine-figure funds––typically, high-profile VCs with global brand names. As a result of their brand status, they naturally end up in more competitive ecosystems with higher valuations—for example, YC at $25M post-money versus Techstars at $10M post.

One could argue that companies from these ecosystems have a higher probability of generating venture-scale outcomes. However, since venture is a power law business, it’s wildly difficult to predict where the next unicorn will originate, especially in today's world of distributed teams and remote work.

Second, startups are becoming more capital efficient, requiring fewer funds to launch an MVP, acquire customers, and achieve scale. Early-stage rounds are becoming smaller, with the average seed round now between $750k and $1.5M.

As a result, it’s near impossible to effectively deploy a nine-figure seed fund raised during the peak market in 2019 to 2022, with fund math predicated on $2M to $3M seed checks.

Over the past 18 months, the game on the field has changed dramatically. Gone are the days of outbidding a competing fund by offering founders a larger check with a higher valuation. However, there remains a significant number of funds that were raised based on this deployment strategy––now unable to move downstream since the growth stage market is still in limbo, yet unable to effectively deploy upstream at pre/seed because their fund math doesn’t support it. These funds are essentially stuck paying higher valuations under the old playbook to remain in business.

Furthermore, although the year began with a heavy influence from LPs citing the denominator effect, this is no longer true as public markets retest all-time highs. While I’ve heard of several VCs paring back fund sizes and returning capital to LPs, I feel the majority are still sitting on the sidelines, blaming high valuations while they figure out how to respond.

Unfortunately, it’s the fund LPs who feel the negative effect as the IRR clock continues to tick, as well as the many founders who are struggling to raise.

Now more than ever, fund size is the strategy. As a result, the edge/alpha has shifted to smaller and earlier checks as companies require less capital to achieve product-market fit and scale.

As an LP in several funds, I’m focused on managers with smaller fund sizes (i.e., sub-$25M), writing pre/seed checks up to $1M over a 3-4 year deployment period. As history shows, emerging managers with smaller fund sizes (and mindful of vintage diversification) are the top-performing VC funds on a net DPI basis.

At Allied, I’m seeing an increasing flow of high-quality deals from talented teams solving venture-scale problems (as outlined in my recent LinkedIn post). I’m excited for the year ahead and will continue to source quality, off-the-beaten-path opportunities at reasonable valuations.

3) Looking Forward: Phase Two, Phase Three

I created Allied to boost the availability of capital for startups in Western Canada. At the same time, I wanted to give local investors more access to high-growth opportunities from established VC markets.

Throughout 2021, Phase One required building a global investor network by syndicating attractive venture-scale opportunities from across North America. In 2022 and 2023, I began executing Phase Two by introducing more Canadian opportunities to the Allied portfolio.

Since our geographical focus includes Canada and the US, it’s only natural that most of our dealflow comes from a US market ten times larger than Canada. However, I remain committed to adding 1-2 Canadian companies to the portfolio each year and have several in the pipeline that I’m excited to share.

Regarding Phase Three, I am still considering an early-stage fund. The fund would provide early checks between $50k to $75k into talented teams where we have high conviction; and be supported by larger follow-on investments from the syndicate as they progress through Seed and Series A.

As I continue to assess the venture landscape and broader fundraising environment, I’m pleased to share that I graduated from the VC Lab Accelerator Program for Emerging Managers earlier this year.

VC Lab is a grueling 16-week program with a 70% failure rate aimed at helping top emerging managers launch new VC funds.

Throughout the program, I worked with other top emerging managers from around the world, and am very grateful for the opportunity to have built our playbook under the guidance of Silicon Valley heavyweights.

What’s Next?

Having gone through the process, I realize how time-consuming raising and launching a new VC fund is. For instance, while the average founder can close a round in 3-5 months, VC funds take 18-24 months (on average).

As a result, I’m at a difficult crossroads. Since current market conditions are so attractive, I don’t want to pause our syndicate activities and miss the current vintage. Meanwhile, raising a new VC fund is a full-time job, and I simply can’t do both while upholding our investment standards.

Ultimately, supporting founders and generating attractive returns for LPs is my top priority, so I’ve chosen to continue deploying capital via the syndicate as I contemplate bringing in another GP to help divide and conquer.

Long-term, I’m committed to my vision of a co-investment model (i.e., fund + syndicate), whereby we work with founders to build meaningful ownership positions over time, ultimately reaching 10%+ ownership within our best-performing companies.

As we move into 2024, please stay tuned for more updates regarding the prospect of Allied Fund I.

************

Thank you once again, Founders, Investors, and Partners, for placing your continued trust and support in Allied throughout the volatility of 2023. I firmly believe the worst is behind us and that market conditions will continue to improve throughout 2024.

Please feel free to connect with me on LinkedIn, Twitter, or by email. I am always happy to chat about startups, fundraising, and anything else that comes to mind.

Sincerely,

--

Matt Wilson, MBA

Founder & Managing Director | Allied Venture Partners