The New Era of Venture Alpha: Decoding the 2026 Midas List

Key Takeaways

Exit value: A minimum of $200 million in realized or unrealized exits over the trailing five years.

Portfolio appreciation: Alternatively, a $200 million increase in portfolio value across the same window.

Secondary market activity: Private secondary sales now factor into valuations, reflecting how liquidity actually moves in today's market.

Recency weighting: More recent exits carry heavier scores, rewarding timely, high-conviction bets over legacy wins.

The 2026 Midas List arrives as more than an annual ranking; it's a definitive stress test for an entire investment era.

The Forbes Midas List is venture capital's most closely watched performance record, tracking the investors whose bets produced the largest, most measurable returns across the global tech landscape. Every year, it separates disciplined conviction from fortunate timing. In 2026, that distinction matters more than ever.

As TechCrunch noted, "The 2026 list serves as a crucial evaluation of the 'ZIRP' (Zero Interest Rate Policy) era investments." For most of the 2010s and into the early 2020s, near-zero interest rates inflated valuations across asset classes, making it easier for passive capital deployment to look like sharp thesis-driven investing. That environment is gone. What's left is a cleaner signal: which investors actually generated alpha, and how.

The answer, increasingly, is operators: investors who bring domain expertise, founder networks, and hands-on support rather than just capital.

The shift from passive growth to AI-driven value creation is reshaping what top-tier venture performance looks like. Companies backed by investors with direct operator experience are outperforming peers not just on exits, but on the speed and quality of company building. The 2026 list directly reflects that structural change.

Analyzing the list reveals that investors who consistently integrate operator expertise, data-driven insights, and a strategic approach to scaling startups are the ones thriving in today's market. A recent 2026 report from Gartner supports this, noting that 67% of high-performing venture firms prioritize operational support alongside financial investment.

What is the Midas List? Understanding the $200M Threshold

The Forbes Midas List is venture capital's most rigorous public benchmark; a data-driven ranking built on verifiable financial outcomes, not reputation or deal volume.

Produced through a research partnership between Forbes and TrueBridge Capital Partners, the list draws on one of the most comprehensive private-market databases in North America. TrueBridge applies a quantitative screen before a single name is considered:

Exit value: A minimum of $200 million in realized or unrealized exits over the trailing five years

Portfolio appreciation: Alternatively, a $200 million increase in portfolio value across the same window

Secondary market activity: Private secondary sales now factor into valuations, reflecting how liquidity actually moves in today's market

Recency weighting: More recent exits carry heavier scores, rewarding timely, high-conviction bets over legacy wins

The $200M floor is the list's defining filter. It separates investors who generate genuine venture-scale returns from those who simply deployed capital into a favorable cycle.

One practical implication for founders: understanding how investors evaluate market potential directly shapes who reaches this threshold. Midas honorees consistently backed companies operating in large, defensible markets before that thesis was consensus.

Including secondary sales marks a significant methodological shift. As traditional IPO and M&A exits remain compressed, secondary transactions now provide credible mark-to-market data — and the ranking reflects that reality. This is supported by research from Stanford University, which highlights how secondary market participation increased by 35% from 2024 to 2026, signaling its growing importance in venture capital.

The AI Takeover: How Infrastructure Bets Dominate the Top 10

AI-focused investors dominate the top 10 positions on the 2026 Midas List: a concentration driven almost entirely by foundational bets on OpenAI, Anthropic, and Mistral.

According to Forbes and TrueBridge Capital Partners, AI mega-startups have fundamentally rewired how venture returns are generated. The investors who backed large language model infrastructure (not applications sitting on top of it) are capturing the lion's share of paper and realized gains. This isn't a coincidence; it reflects a structural shift in where value is accruing across the technology stack.

AI infrastructure has become the current Midas engine precisely because it compounds across every vertical simultaneously. A single foundational model investment touches healthcare, legal tech, fintech, and defense at once. That cross-sector leverage is something conventional SaaS plays simply can't replicate, which is why the returns profiles look so asymmetric right now.

The difference with non-AI SaaS is stark. The exit market for traditional SaaS businesses remains largely frozen. IPO windows are narrow, strategic acquirers are cautious, and multiples have compressed significantly from their 2021 peaks. Founders building in that space are navigating a more demanding fundraising environment, where the fundamentals of scaling a startup matter more than narrative alone.

Understanding where Midas-level returns are clustering today helps explain a broader geographic narrative – one that extends well beyond Silicon Valley's traditional deal flow corridors.

Beyond the Bay Area: The Decentralization of Deal Flow

Geographic concentration has long defined venture capital's power structure, and the numbers make it hard to argue. Over 60% of 2024 Midas List Forbes investors were based in the Bay Area, according to Forbes and NVCA data, creating a gatekeeper effect that systematically disadvantaged founders building outside Silicon Valley.

The result was that geography, rather than fundamentals, filtered too much deal flow.

That model is being challenged. Digital-first syndicates and operator networks are enabling capital to move across borders without requiring a Caltrain commute. Where the "Old Guard" model demanded warm introductions through Sand Hill Road relationships, the emerging "New Network" model routes deal flow through distributed communities of domain experts, former operators, and sector-specific angels spread across North America.

For early-stage software founders in Toronto, Vancouver, Calgary, or Austin, this shift is material. A fee-free pitching process, like the model Allied Venture Partners operates, removes the friction that once made geography destiny. Founders can access a diverse operator network without relocating or cold-emailing partners who never respond. If you're evaluating your options, it's worth understanding how early-stage capital actually works before choosing which networks to prioritize.

Endeavor's 2024 analysis noted the Midas List was becoming its most global edition yet — a signal that decentralization isn't theoretical. It's already happening at the growth stage. The more interesting question is where it's happening earliest, and that points directly toward seed-stage investing.

The Rise of the Midas Seed List: Where Future Giants Are Found

Early identification separates generational investors from everyone else, and the Forbes Midas Seed List exists precisely to spotlight who's doing it best.

The real alpha in venture isn't catching the next OpenAI at Series C, it's being the first check in before the narrative solidifies. For early-stage founders, the Midas Seed List functions as a credibility signal: these are the investors who have a documented track record of finding companies in the $10M–$100M valuation range and helping them become breakout names. That window represents disproportionate upside for both founders and investors willing to move before consensus forms.

What distinguishes the investors on this list isn't just capital, it's pattern recognition at an early, ambiguous stage when most data is incomplete. As Brad Feld of Foundry has noted, "The next generation of Midas investors will be those who provide more than just a check; they are the operators who can help a company scale." That distinction matters enormously at Seed, where a single strategic introduction or go-to-market insight can compress an 18-month growth timeline.

Operator-led networks are increasingly the deciding factor in the Seed to Series A transition. Founders who navigate that gap successfully tend to have investors who bring direct functional expertise in product, distribution, or enterprise sales, not just governance. If you're evaluating funding options beyond traditional accelerators, the composition of your investor's operator network deserves as much scrutiny as the check size itself.

That structural advantage (i.e., who's in your corner, not just how much they wrote), increasingly determines which Seed investments survive to define the next Midas list. And as we'll explore next, who gets access to those networks reflects a deeper tension that the list hasn't fully resolved.

The Diversity Gap: Why the Midas List Still Has a Representation Problem

Venture capital's returns data increasingly points in one direction: diverse investment committees outperform, yet the Midas List still doesn't reflect that reality.

Women represented only 11% of the Midas List in recent cycles, according to Forbes and Deloitte Venture View research, despite evidence that gender-diverse decision-making teams generate stronger risk-adjusted returns. That gap isn't a pipeline problem; it's a structural one baked into how legacy firms hire, promote, and allocate carry.

The business case for diverse investment committees is straightforward when you follow the data. Homogeneous networks surface homogeneous deal flow. When every partner shares the same background, geography, and professional history, the firm systematically misses categories of founders and, therefore, categories of returns. Diverse operators evaluate risk differently, pattern-match across broader markets, and tend to catch blind spots that consensus-driven committees overlook.

This is precisely where alternative syndicates have a structural edge. Networks built around operator-investors, across industries, geographies, and demographics, evaluate founders through a wider lens. At Allied Venture Partners, that diversity of perspective is embedded in how we assess deal flow, connecting founders with a network that reflects the actual breadth of the North American software ecosystem.

The Midas List measures past performance. The diversity gap is where future alpha is hiding, and that creates real opportunity for syndicates willing to look where legacy firms haven't. The question of when that value gets realized, however, is increasingly tied to a market where the traditional exit window has all but frozen.

Secondary Markets and the New Path to Liquidity

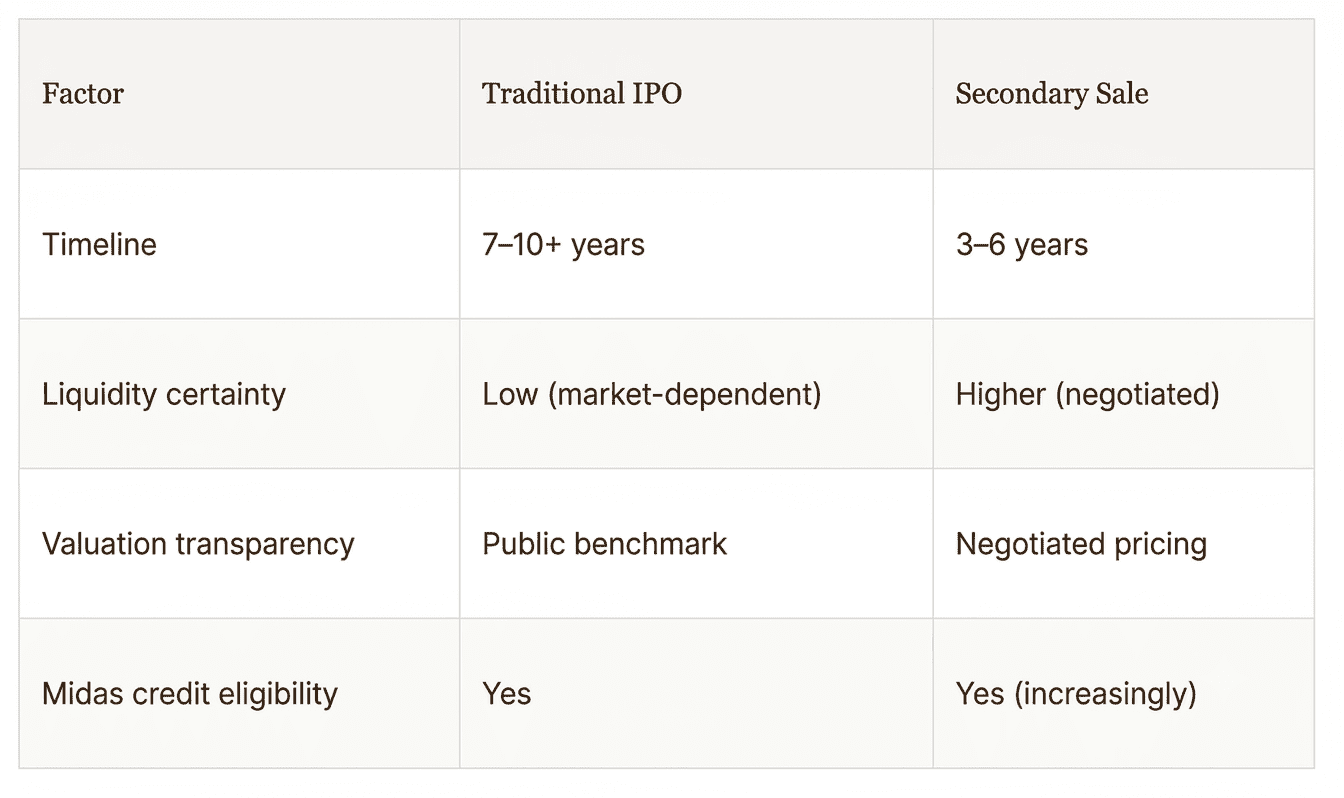

The exit market is frozen, and the Midas List methodology is quietly adapting to reflect that reality.

According to Forbes, the 2024 Midas List featured a record-low 12 newcomers, a direct signal that IPO windows have narrowed dramatically. With public markets volatile and traditional exit timelines stretching well beyond the historical seven-to-ten-year range, investors can no longer rely on IPOs as their primary liquidity event.

The shift is structural: secondary transactions are now a recognized path to Midas-tier credit, not just a workaround.

What does that mean in practice? A sale of secondary shares, either to another institutional investor or through a dedicated secondary platform, can generate the kind of realized returns that the Midas methodology rewards. The table below illustrates how these two paths compare:

For founders and investors navigating today's low-liquidity environment, understanding how pre-IPO secondary markets work is no longer optional; it's a core part of portfolio strategy. Networks that provide early access to secondary transactions are becoming as valuable as the initial check.

What this means for your specific position as a founder or investor comes down to one question: how does the $200M benchmark and AI dominance on the Midas List translate into actionable decisions?

The Bottom Line: What the 2026 Midas List Means for You

The 2026 Midas List sends a clear signal: AI is no longer a category bet, it's the baseline infrastructure of venture-scale returns.

Here are the four takeaways every founder and investor should carry forward:

AI is the default, not the differentiator. According to Forbes and TrueBridge, AI mega-startups have fundamentally rewired how Midas-tier returns are generated. Backing AI-native software companies is no longer an edge; it's the minimum entry point for competitive deal flow.

Operator expertise is the primary moat. In a low-liquidity environment where traditional IPO exits remain unpredictable, the investors who win are the ones with hands-on operational insight. Secondary market transactions are increasingly counting toward Midas credit precisely because operators know how to manufacture liquidity where none exists.

Geography matters less than network access. Digital-first syndication has decoupled deal quality from zip code. What previously required a Sand Hill Road address now requires the right operator network and a disciplined evaluation process.

$200M is the benchmark. The Forbes Midas methodology uses a $200M exit value threshold to define top-tier performance; a number that frames what "success" looks like at the portfolio level.

The investors and founders who internalize these four shifts now are best positioned to define the 2027 list, not just admire it. For anyone ready to act on that, the next question is which network gets you closest to that outcome.

Finding Your Midas Partner: Why Allied Venture Partners Is the Next Step

The trends shaping the 2026 Midas List (AI infrastructure bets, operator-led networks, and early entry at Seed) are exactly where Allied Venture Partners operates.

The data is consistent: Midas-tier returns trace back to investors who entered early, backed software with durable infrastructure value, and leveraged operator networks to support portfolio companies through each growth stage. For early-stage founders and accredited angel investors in North America, the question isn't whether these dynamics matter; it's how to access them.

Allied Venture Partners is built around that access problem. As one of Canada's largest angel investor networks, the firm connects Seed and Series A software founders with a diverse network of operators and investors who can evaluate, support, and fund companies with genuine growth potential. Founders can pitch through a fee-free 'Pitch Us' portal (no application costs, no gatekeepers, just a direct path to a network that understands early-stage software).

For investors, Allied offers something increasingly rare: curated deal flow without traditional membership fees. Through our venture capital syndication platform, accredited angel investors can build a venture-scale portfolio of high-quality software opportunities, co-invest alongside tier-1 Midas List investors, and be supported by operator insight rather than brand-driven selection bias.

The 2026 Midas List confirms the shift toward specialized, network-driven capital in the venture model, and that shift creates real opportunity for those who move early. Whether you're a founder ready to raise your Seed round or an investor seeking structured exposure to North America's software ecosystem, Allied Venture Partners offers a concrete next step.

Submit your pitch or explore our investor platform at allied.vc to connect with a network built for early-stage software success.