Down Round Dilution: Solving Common Founder Equity Problems

Key Takeaways

Down rounds are increasingly common. In Q1 2024, 23% of all new venture rounds were down rounds — the highest rate in more than five years — making this a critical issue for founders to understand and prepare for.

Dilution hits founders hardest. When a company raises capital at a lower valuation, more shares must be issued to secure the same amount of capital, shrinking founder ownership percentages faster and more severely than in a standard up round.

Anti-dilution provisions determine who absorbs the pain. Full ratchet provisions are the most damaging for founders, repricing all prior preferred shares to the lowest valuation. Broad-based weighted average provisions distribute the dilution impact more fairly and should always be the goal in negotiations.

SAFEs can create unexpected dilution surprises. When SAFEs with valuation caps and discounts convert during a down round, founders can end up giving away significantly more equity than anticipated. Understanding SAFE conversion mechanics before a down round hits is essential.

Liquidation preferences can wipe out founder economics at exit. Investors typically receive their capital back before founders see any proceeds. In a low-exit scenario, even a 1x liquidation preference can absorb all available proceeds, leaving founders with nothing.

Employee stock options are collateral damage. A falling share price renders existing options underwater and damages company morale at a critical time. Founders may need to issue refresh grants — at the cost of additional dilution — to retain and motivate key team members.

Board composition and control are at risk. New and existing investors often use a down round to negotiate additional board seats and governance rights, potentially shifting strategic control away from founders.

Proactive negotiation is a founder's strongest defense. Thoroughly preparing before term sheet discussions — knowing the company's financials, understanding market comparables, and identifying which clauses matter most — gives founders meaningful leverage even in a difficult fundraising environment.

Alternatives to equity financing deserve serious consideration. Venture debt, bridge financing, convertible notes, and revenue-based financing can provide necessary runway while minimizing or deferring equity dilution.

Transparency and communication are essential post-round. Openly addressing the down round with employees, existing investors, and new investors — and presenting a credible recovery plan — is critical for rebuilding confidence and maintaining momentum.

A down round is not the end. Securing capital, even at a lower valuation, preserves the company's ability to execute, grow, and ultimately create value. A smaller stake in a thriving company is almost always worth more than a larger stake in one that runs out of runway.

Down Round Dilution: Solving Common Founder Equity Problems

The entrepreneurial journey is often characterized by a relentless pursuit of growth, fueled by external capital. For founders, securing funding is a critical milestone, a validation of their vision, and a necessary catalyst for scaling. However, the landscape of startup financing is inherently dynamic, and market shifts can lead to challenging scenarios, none more daunting for a founder than a "down round." This occurs when a startup raises capital at a valuation lower than its previous funding round. While necessary for survival or continued growth, a down round can trigger a cascade of equity-related problems, disproportionately impacting founders' ownership stakes, control, and overall economic well-being.

Understanding and proactively addressing the complexities of down round dilution is not just about preserving equity; it's about safeguarding the founder's long-term vision and motivation. The very shares that represent their hard work and belief can become significantly diluted, potentially diminishing their incentive and altering the power dynamics within the company.

This comprehensive guide aims to demystify the mechanics of down round dilution and, more importantly, equip founders with practical strategies and solutions to navigate these challenges, protect their equity, and emerge stronger. We will explore the core issues, dissect the critical protective mechanisms, and delve into specific problems founders often encounter, offering actionable advice for proactive negotiation and strategic recalibration.

What is a Down Round and Why Does it Matter to Founders?

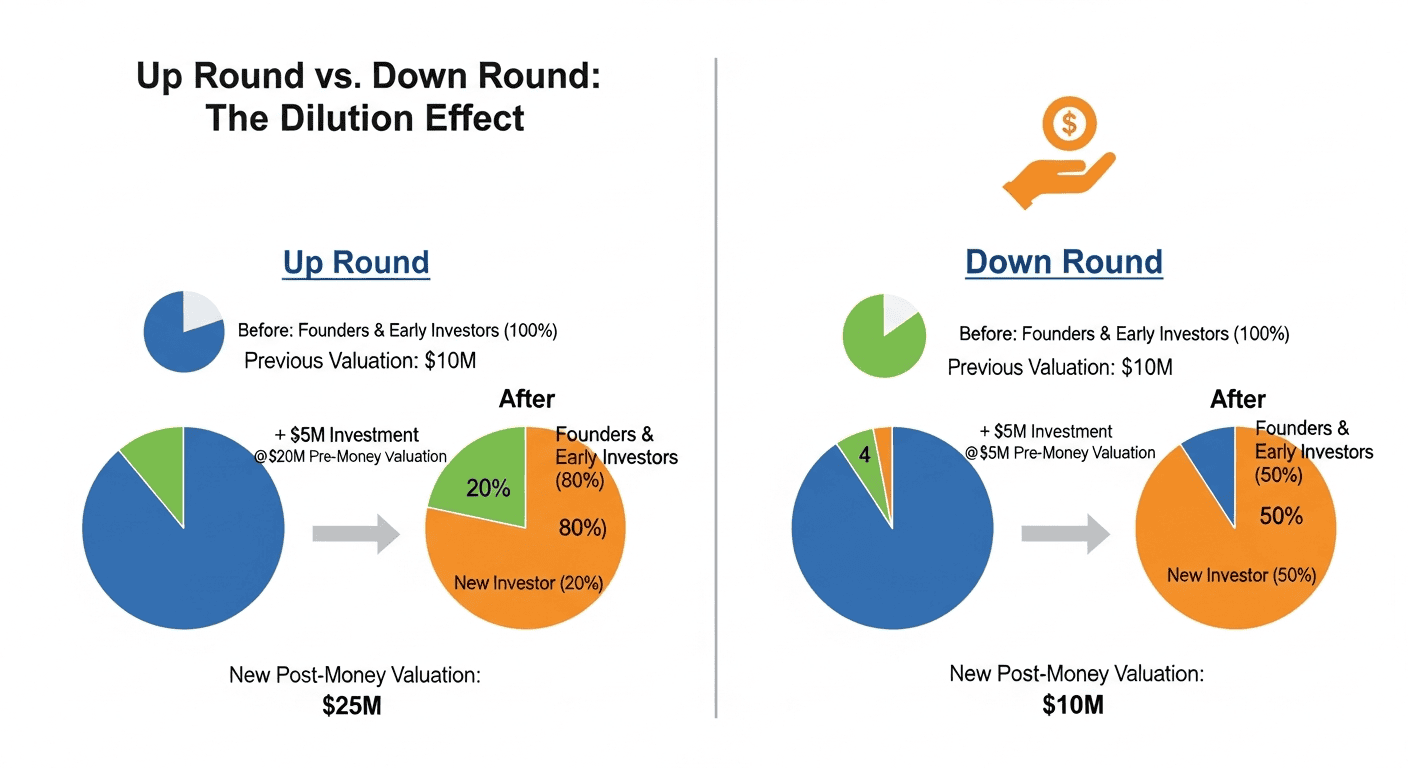

A down round significantly increases dilution. In this example, the same $5 million investment results in 2.5 times more dilution for founders and early investors in a down round compared to an up round.

A down round signifies a critical inflection point in a startup's life. Unlike previous funding rounds where the company's valuation typically increased, a down round involves raising new capital at a lower pre-money valuation than the one set during the preceding round. This isn't merely a technical accounting adjustment; it’s a market signal that can influence investor confidence, employee morale, and critically, the founders' ownership percentage.

The current market environment underscores the relevance of this issue; in Q1 2024, an alarming 23% of all new venture rounds were down rounds, marking the highest rate in more than five years (source: Carta, May 2024). This trend highlights a challenging fundraising climate where securing capital on favorable terms is increasingly difficult.

For founders, a down round is a stark reminder that the journey is rarely linear. The valuation achieved in earlier funding rounds sets an expectation for future growth and equity value. When this valuation is revisited downwards, the implications are immediate and profound. It can suggest that the company has not met its growth targets, is facing increased competition, or that broader market conditions have shifted unfavorably, impacting the perceived value of the startup. The consequence for founders is often a more pronounced loss of ownership than anticipated, a phenomenon driven by the mechanics of how new shares are issued and how existing agreements are structured.

The Core Problem: Founder Dilution and Ownership Erosion

At its heart, the primary concern for founders during a down round is dilution. Dilution refers to the reduction in an existing shareholder's proportionate ownership of a company. When a startup raises new capital by issuing more shares, the total number of outstanding shares increases. If the new issuance is priced at a lower valuation than previous rounds, the existing shareholders, particularly founders who typically hold a significant portion of common equity, see their ownership percentage shrink more dramatically than if the new round were at an increased valuation.

Consider the typical founder's journey: After raising a seed round, the median founding team collectively owns 56.2% of their startup's equity. By Series A, this typically falls to 36.1%, and by Series B, it's around 23% (source: Carta, January 2025). These benchmarks already illustrate substantial dilution across early funding rounds. A down round exacerbates this erosion. It's not just about owning fewer shares; it's about owning a smaller piece of the overall pie, potentially affecting control, decision-making power, and the ultimate economic payout.

In a challenging market, late-stage pre-money valuations dropped significantly in 2023, with venture growth pre-money valuations experiencing a nearly 50% year-over-year decline (source: Valuation Research, June 2024). This drastic reduction in perceived company value directly translates to founders and early employees giving up more equity for the same amount of capital.

Purpose of This Guide: Practical Solutions for Protecting Your Equity

This guide is designed to move beyond a mere explanation of the problem and offer tangible solutions for founders facing the prospect or reality of a down round. We aim to provide a strategic framework for understanding, negotiating, and mitigating the adverse effects of dilution on founder equity. By delving into the specific mechanisms that trigger severe dilution, exploring the critical protective clauses within investment agreements, and addressing common pain points, founders can approach these challenging funding rounds with greater preparedness and strategic foresight. Our objective is to empower you with the knowledge to protect your stake, maintain your motivation, and ensure your startup can continue its journey towards success, even when navigating difficult market conditions.

Understanding the Mechanics of Down Round Dilution

The impact of a down round on founder equity is not arbitrary; it's a direct consequence of financial mechanics governed by valuation, share price, and the structure of investment agreements. Understanding these mechanics is the first step towards effective mitigation.

How Valuation Shifts Impact Founder Ownership

The valuation of a startup is the cornerstone upon which all funding rounds are built. It dictates the price per share at which new capital is exchanged for equity. When a startup raises capital at a pre-money valuation of $10 million and issues 1 million new shares, the price per share is $10. If the next funding round occurs at a pre-money valuation of $5 million, and the company needs to raise the same amount of capital ($10 million), it will need to issue 2 million new shares at $5 per share.

This means that existing shareholders, including the founders, will see their ownership percentage significantly reduced. For every share they previously owned, they now represent a smaller fraction of a larger total share count, and crucially, the new investors are acquiring shares at a substantially lower price, potentially triggering protective clauses for those investors.

The Cap Table's Story: Visualizing Dilution Patterns

The cap table (capitalization table) is the definitive ledger of a company's equity structure. It meticulously tracks every shareholder, the number of shares they own, the type of shares (common, preferred), and the valuation at which those shares were issued.

In the context of a down round, the cap table becomes an essential tool for visualizing the impact of dilution. It clearly shows how the ownership percentage of founders and early employees diminishes with each new funding round, especially when that round is at a lower valuation. Analyzing the cap table before and after a down round can starkly reveal the extent of equity erosion and the immediate effect of protective clauses designed to shield investors. Understanding these shifts is paramount for founders to grasp the true economic consequences of the down round on their personal stake.

The Role of Share Price in Equity Dilution

The share price is the direct mechanism through which valuation changes translate into dilution. In any funding round, the pre-money valuation is divided by the number of shares outstanding before the new investment to determine the price per share. A lower pre-money valuation in a down round directly results in a lower share price. This lower price means that more new shares must be issued to raise the desired amount of capital.

For example, if a startup previously raised capital at $10 per share, and now raises capital at $4 per share in a down round, existing shareholders have their equity effectively repriced downwards. This is where anti-dilution provisions come into play, often protecting the investors who bought at the higher price by allowing them to convert their shares into more shares at the lower price, further increasing the dilution for founders and other common shareholders.

Beyond Ownership Percentage: The Broader Impact on Control and Motivation

While the reduction in ownership percentage is the most tangible aspect of dilution, a down round can have broader, more insidious impacts on founders. A significant drop in equity can diminish a founder's motivation, as their perceived reward for future success is lessened. If a founder's ownership percentage falls below critical thresholds, it can also erode their control over the company's direction. Board seats, voting rights, and the ability to influence strategic decisions can be jeopardized.

In some cases, founders might find themselves owning a small piece of a company that is struggling to regain its footing, a situation far less appealing than owning a larger stake in a thriving business. While this can feel discouraging, it's crucial to remember the adage that "a small piece of a big pie is usually more valuable than a big piece of a small pie."

The challenge in a down round is to ensure that the new capital allows the company to grow into a significantly larger and more valuable entity, ultimately making the founder's reduced percentage more valuable than their prior larger percentage in a struggling company. However, the impact on motivation and control cannot be overlooked.

The Primary Defense: Anti-Dilution Provisions

Anti-dilution provisions are a critical component of preferred stock terms designed to protect investors from the negative effects of dilution that occur between funding rounds. While primarily investor protections, understanding them is crucial for founders as they directly influence how dilution is distributed.

What is Anti-Dilution Protection and Why is it Crucial?

Anti-dilution protection is a contractual clause that adjusts the conversion price of preferred shares downwards if the company later issues new shares at a lower price. This ensures that investors who purchased preferred equity at a higher valuation are not unfairly disadvantaged by subsequent, lower funding rounds. For founders, this is crucial because these provisions often dictate who bears the brunt of the dilution. Without adequate understanding and negotiation, founders can find themselves absorbing the majority of the dilution impact, even when the company needs the new capital to survive.

Full Ratchet vs. Weighted Average: A Critical Distinction for Founders

There are two primary types of anti-dilution protection: Full Ratchet and Weighted Average. The distinction between them is paramount for founders.

Full Ratchet is the most aggressive form of anti-dilution protection. Under a Full Ratchet clause, if a company issues new shares at a price below the investor's original purchase price, the investor's shares are converted into new shares at this new, lower price. This effectively means that all prior preferred shares are repriced to the lowest price paid in any subsequent funding round. Full ratchet anti-dilution provisions can severely harm founder equity during down rounds, as they reset the price of all previous shares to the lowest valuation, resulting in significant dilution. This can lead to catastrophic dilution for founders and early employees.

Weighted Average is a more common and generally more founder-friendly form of anti-dilution. Instead of repricing all prior shares, it calculates a new, adjusted price based on a weighted average of the original price and the new, lower price, considering the number of shares issued at each price. This approach spreads the dilution impact more evenly between new investors and existing shareholders, including founders.

The Founder's Ally: Broad-Based Weighted Average Anti-Dilution

Within the Weighted Average category, there are further distinctions: narrow-based and broad-based. A narrow-based weighted average typically considers only the price of the new shares and the price of the previous round's preferred shares when calculating the adjustment. A broad-based weighted average, however, includes all outstanding shares (common shares, options, warrants, and all classes of preferred shares) in its calculation.

For founders, broad-based weighted average anti-dilution is significantly more advantageous. By including common shares and other potentially dilutive instruments in the calculation, it spreads the dilution effect across a wider base, thereby reducing the impact on any single group, including the founders. When negotiating term sheets, advocating for broad-based weighted average protection is a critical strategy for founders to safeguard their equity.

Understanding Investor Perspective on Anti-Dilution Clauses

While founders aim to protect their equity, investors seek to protect their capital and returns. Anti-dilution clauses are primarily designed to ensure that investors don't lose value disproportionately if the startup subsequently raises money at a lower valuation. They view these provisions as essential risk mitigation tools.

In our experience at Allied Venture Partners, anti-dilution provisions in term sheets mean founders absorb more impact than preferred shareholders in down rounds. This highlights the inherent tension. Founders must understand that investors will likely push for the strongest protections for themselves. Therefore, negotiation around these clauses is a delicate balance between securing necessary funding and preserving founder ownership and incentives.

The increasing prevalence of protective terms, such as liquidation preferences of 1x or higher, which appeared in 8% of all new funding rounds on Carta in Q1 2024, marking the highest percentage this decade, indicates a cautious market where investors are prioritizing downside protection (source: Carta, June 2024).

Navigating the Term Sheet: Proactive Negotiation Strategies

The term sheet is the foundational document outlining the proposed terms of an investment. For founders, negotiating the term sheet for a down round is a critical juncture that can significantly shape the future of their equity and control.

Preparing for the Down Round Term Sheet Negotiation

Thorough preparation is key. Before entering negotiations, founders should have a clear understanding of their company's current financial health, burn rate, achievable growth milestones, and realistic market valuation. They must also understand the specific terms being proposed, paying close attention to anti-dilution provisions, liquidation preferences, and voting rights.

Knowing the competitive landscape is also beneficial. For instance, while total cash raised on Carta increased in 2024, the number of new investments declined, suggesting a trend towards larger, more concentrated deals, potentially making it harder for some startups to secure funding without accepting less favorable terms (source: Carta, February 2025). This market context can inform negotiation strategy.

Key Anti-Dilution Provisions to Focus On

When reviewing term sheets for a down round, founders must prioritize specific anti-dilution clauses:

Type of Anti-Dilution: As discussed, always push for Weighted Average over Full Ratchet.

Breadth of Weighted Average: Advocate for Broad-Based Weighted Average to distribute dilution more widely.

Carve-outs: Negotiate for exceptions where the issuance of new shares would not trigger anti-dilution. Common carve-outs include shares issued under employee stock option plans (ESOPs), shares issued in connection with acquisitions, and bona fide equity incentive plans. These carve-outs can significantly mitigate the dilution impact on founders and employees.

Definition of "Price": Ensure clarity on how the "price" of new shares is defined, particularly concerning discounts or warrants.

Leveraging Negotiation Strategy to Protect Your Equity Stake

Founders should approach down round negotiations with a clear objective: to secure the necessary capital while minimizing destructive dilution. This involves:

Understanding the "Why": If the down round is due to a temporary market downturn rather than fundamental business issues, founders have more leverage. If it's due to missed milestones, the negotiation will be tougher.

Prioritizing and Trading: Recognize that not every favorable term can be won. Understand which clauses (e.g., anti-dilution, liquidation preferences) are most critical to preserving founder equity and control. Be prepared to make concessions on less critical points to secure gains on the most important ones.

Framing the Narrative: Emphasize the long-term vision and the potential for future growth with the new capital. Highlight how preserving founder motivation and equity is crucial for achieving this future success.

Seeking Alternatives: Explore if alternative funding structures are possible, such as debt financing or bridge loans, which might carry different dilution implications.

The Indispensable Role of Legal Counsel and Financial Advisors

Navigating the complexities of down round term sheets, especially concerning equity and dilution, is an area where expert advice is non-negotiable. Engaging experienced legal counsel specializing in venture capital and startup finance is paramount. They can identify pitfalls in term sheets, advise on standard market terms, and help structure negotiations to protect founder interests.

Similarly, a skilled CFO or financial advisor can help model the financial implications of different term sheet provisions, providing objective analysis on the impact of dilution on the cap table and founder economics. This professional guidance ensures that founders make informed decisions during a high-stakes negotiation.

Solving Specific Founder Equity Problems in a Down Round Scenario

Down rounds present a unique set of challenges that go beyond simple percentage ownership reduction. Founders must grapple with specific contractual and operational issues that can further complicate their equity situation.

Problem 1: The SAFE Conversion Surprise and Accelerated Dilution

SAFE (Simple Agreement for Future Equity) agreements, popular for early-stage funding, can introduce unexpected complexities in a down round. While designed to defer valuation discussions, their conversion terms can lead to accelerated dilution for founders. A SAFE typically includes a valuation cap and/or a discount. In a down round, if the new valuation is lower than the SAFE's valuation cap, the SAFE holders will convert their investment into shares at the lower price, but potentially using the valuation cap, effectively getting more shares than if they converted at the actual new round valuation without a cap. This is compounded if the SAFE also has a discount.

To mitigate this, founders should strive to negotiate favorable terms in their initial SAFE agreements, such as a higher valuation cap or a limited discount that is not additive to other down-round protections. If a down round occurs, founders should carefully review the conversion mechanics and consider if there's room to negotiate with the SAFE holders, perhaps offering them a smaller percentage of the new round in exchange for a more favorable conversion. Understanding the interplay between the SAFE cap, discount, and the new round's valuation is crucial for projecting and managing the resulting dilution.

Problem 2: Impact on Employee Stock Options and Company Morale

A down round can significantly impact employee stock options (ESOPs). When the company's valuation drops, the share price decreases. This can make existing options with higher strike prices (exercise prices) significantly less attractive, potentially rendering them "underwater" – where the strike price exceeds the current market value of the shares. This reduces the incentive for employees to exercise their options and can negatively affect morale.

To address this, founders may need to consider offering "refresh grants" of new options at a lower strike price to employees. This requires careful consideration of the ESOP pool size and the overall dilution. Furthermore, transparent communication with employees about the down round, its necessity, and the efforts being made to protect their equity is vital. Explaining how the company plans to recover and grow can help mitigate the negative impact on morale. Founders must also ensure that any ESOP refresh grants are properly accounted for in the cap table and that anti-dilution provisions in new investments do not disproportionately penalize these employee incentives.

Problem 3: Liquidation Preferences and Founder Economics Post-Down Round

Liquidation preferences are a critical investor protection that can significantly alter a founder's economic outcome, especially in a down round. A liquidation preference dictates that investors receive their initial investment back (often with a multiple, like 1x, or even more) before any proceeds are distributed to common shareholders (which typically include founders). In a down round, the company's overall valuation is lower. If the company is later acquired or has an exit event, the total proceeds might only be enough to satisfy the liquidation preferences of the investors, leaving little or nothing for the founders.

For instance, if investors have a 1x non-participating liquidation preference, they get their money back first. In a scenario where the company is sold for an amount less than what would yield a significant return to common shareholders after investor payouts, founders could see their economic upside disappear. While 97% of non-participating preferred shares utilized a 1x multiple in 2024, indicating a trend toward more founder-friendly terms compared to higher multiples, it's still a critical factor (source: Phoenix Strategy Group, September 2025). Founders must negotiate these liquidation preferences carefully, ideally aiming for 1x non-participating preferences if possible, and understanding the implications for their own economic future in various exit scenarios.

Pro tip: To learn more about liquidation preferences for founders versus investors, see our guide Liquidation Preferences: Investor vs. Founder Interests.

Problem 4: Maintaining Board Composition and Governance

Down rounds can also affect board composition and governance. When a company raises new capital, especially from new investors, these investors often gain rights to appoint board members. In a down round, existing investors might also seek to strengthen their representation on the board to oversee the company's recovery and ensure their investment is protected. This can lead to a shift in the balance of power, potentially reducing the founder's direct control over strategic decisions.

Founders need to anticipate this and negotiate for board seats and voting rights that allow them to maintain significant influence. This might involve agreeing to a smaller board size initially, or ensuring that certain key decisions still require founder consensus. Understanding the voting agreements and shareholder rights associated with different classes of shares is crucial.

Strategic Re-evaluation and Resilience Post-Down Round

Surviving a down round is not just about getting through the immediate fundraising process; it requires a strategic recalibration of the company's trajectory and a focus on building long-term resilience.

Recalibrating Your Capitalization Table for the New Reality

After a down round, the cap table reflects a new reality of equity distribution. Founders must meticulously update their cap table to accurately reflect the new shares issued, the adjusted share prices, and the impact of any anti-dilution adjustments. This updated cap table serves as the foundation for all future financial planning and fundraising efforts. It's essential to use sophisticated cap table management software or consult with experts to ensure accuracy, as errors can lead to significant legal and financial complications down the line. Understanding the precise ownership percentage of each shareholder is critical for future negotiations and potential exit scenarios.

Communicating with Shareholders and Stakeholders

Transparency and clear communication are paramount following a down round. Founders must proactively communicate with all shareholders, including employees, existing investors, and any new investors, about the reasons for the down round, the terms of the new funding, and the company's revised strategic plan.

Employees: Be honest about the impact on their ESOPs and explain the plan for recovery and future growth. Reassure them of the company's vision.

Existing Investors: Explain how their equity has been impacted and demonstrate confidence in the path forward.

New Investors: Clearly articulate the revised strategy and milestones that will drive future valuation increases.

Open dialogue builds trust and can help mitigate negative sentiment, fostering a united front for recovery. In 2024, 63% of startups identified fundraising as a top three challenge, highlighting the difficult environment that can force down rounds (source: Slush Startup Struggle survey, October 2024). This difficult landscape makes clear communication even more vital.

Adjusting Your Long-Term Fundraising Strategy

A down round necessitates a re-evaluation of the long-term fundraising strategy. The valuation achieved in the down round sets a new baseline. Future funding rounds will need to demonstrate significant growth and progress to achieve a higher valuation and regain investor confidence. This means:

Setting Realistic Milestones: Focus on achievable, measurable milestones that clearly signal progress and growth.

Demonstrating Capital Efficiency: Show investors that the new capital is being used wisely to drive sustainable growth, with a managed burn rate.

Building a Strong Narrative: Craft a compelling story about the company's resilience, its updated strategy, and its path to future success. This narrative should be supported by strong operational performance.

The market dynamics, with total cash raised increasing by over 18% in 2024 despite fewer investments, suggest a more selective investor base focused on quality and potential for significant returns (source: Carta, February 2025). Founders must align their strategy with investor expectations.

Maintaining Founder Motivation and Vision

Perhaps the most crucial aspect of navigating a down round is maintaining founder motivation and vision. The personal and professional toll can be immense. However, it's vital to remember that a down round is often a sign of market realities or temporary setbacks, not an indictment of the founder's ability or the company's ultimate potential. In our experience at Allied Venture Partners, no startup has ever died from excess dilution, but the same cannot be said for lack of funds. This pragmatic view underscores the importance of securing capital even if it comes at a higher dilution cost.

Founders should:

Re-center on the Mission: Remind themselves and their team of the original vision and the problem the company is solving.

Focus on Execution: Channel energy into operational execution, hitting milestones, and demonstrating tangible progress.

Seek Support: Lean on mentors, advisors, and peer networks who have navigated similar challenges.

Celebrate Small Wins: Acknowledge and celebrate achievements along the path to recovery to maintain team morale.

Summary: Down Round Dilution Implications

A down round represents one of the most significant challenges a founder can face, threatening not only the startup's financial trajectory but also the founder's personal equity and motivation. The mechanics of dilution, driven by shifting valuations and complex term sheet provisions, can lead to substantial erosion of ownership percentage. However, this challenge is not insurmountable. By understanding the intricate interplay between valuation, share price, and anti-dilution clauses, particularly the critical distinction between Full Ratchet and Weighted Average provisions, founders can approach negotiations with greater strategic insight.

The journey through a down round demands meticulous preparation, assertive negotiation, and unwavering transparency. Addressing specific issues like SAFE conversions, the impact on employee stock options, the implications of liquidation preferences, and potential shifts in board governance is crucial for protecting founder economics and control. Post-round, recalibrating the cap table, communicating effectively with all shareholders, and adjusting long-term fundraising strategies are essential steps toward recovery and future growth.

Ultimately, maintaining founder motivation and vision, grounded in a clear understanding of the path forward and a commitment to execution, is the bedrock upon which a startup can rebuild and thrive after a down round. Armed with knowledge and a proactive strategy, founders can navigate these turbulent waters, protect their equity, and emerge stronger, more resilient, and better positioned for long-term success.

Frequently Asked Questions: Down Round Dilution

What exactly is founder dilution, and why does it matter more in a down round than in a normal financing round?

Founder dilution occurs whenever new shares are issued and a founder's ownership percentage decreases as a result. In ordinary VC rounds — where valuations are rising — this equity dilution is offset by the increasing value of each remaining share; founders own less of a bigger pie. In a down round, however, the pie actually shrinks in perceived value at the same time as the ownership stake is reduced, creating a compounding effect. Because the share price is lower, more shares must be issued to raise the same amount of capital, amplifying the dilution far beyond what founders typically experience in up-round financing rounds. This is why down rounds can feel disproportionately punishing and why careful preparation matters so much.

How do SAFEs contribute to unexpected equity dilution during a down round?

SAFEs (Simple Agreements for Future Equity) are a popular early-stage startup funding tool partly because they defer the question of valuation. However, that deferred valuation question can become very expensive in a down round. When a down round is triggered, SAFEs convert into equity — but under terms set at signing, not at the new, lower valuation.

If a SAFE carries a valuation cap that is higher than the new round's pre-money valuation, the SAFE holder still converts using the cap, effectively receiving more shares than they would at the current round price. Layered on top of a discount rate, SAFE notes can produce surprisingly aggressive equity dilution for founders. Platforms like AngelList, which popularized SAFEs for early-stage deals, recommend that founders fully model SAFE conversion scenarios — including down-round cases — before signing. Running cap table modeling prior to any capital raise is the best way to avoid conversion surprises.

What is the difference between full ratchet provisions and weighted average provisions, and which is better for founders?

Both full ratchet provisions and weighted average provisions are forms of anti-dilution rights built into preferred stock to protect investors when a down round occurs, but they work very differently and have dramatically different consequences for founders. Full ratchet provisions are the more aggressive of the two: they reprice every previously issued preferred share all the way down to the lowest price paid in any subsequent round, regardless of how many shares were issued at that lower price. This can be catastrophic for founders because it artificially inflates the share count held by investors, causing severe equity dilution for common stockholders.

Weighted average provisions, by contrast, calculate a blended conversion price that takes into account both the old and new share prices, weighted by the volume of shares issued at each price. Broad-based weighted average provisions are the most founder-friendly because they factor in all outstanding shares — including common stock, options, and warrants — which softens the adjustment further. When reviewing financing documents and term sheets, founders should push firmly for broad-based weighted average provisions and resist full ratchet provisions wherever possible.

How do option pools and employee stock options get affected by a down round?

Option pools are a reserve of shares set aside for employee equity compensation, and a down round can make them a source of significant tension. When a company's valuation drops, the strike prices on existing employee stock options — set at the fair market value when they were granted — may now exceed the current share price, rendering those options "underwater" and essentially worthless unless the company recovers. This directly damages company morale and can accelerate employee departures at exactly the moment the company most needs stability.

To address this, founders sometimes issue refresh grants from the option pools at a new, lower strike price. However, this increases the total share count and adds another layer of equity dilution. Additionally, investors frequently require an expansion of the option pools as a condition of a down round, and this expansion is typically carved out of the pre-money valuation — meaning it dilutes founders before new money even enters. Understanding how option pool sizing interacts with the post-money valuation is critical for founders negotiating down round terms.

What role do liquidation preferences play in founder economics after a down round, and what does waterfall modeling show?

Liquidation preferences determine who gets paid first — and how much — when a company is sold or undergoes another exit event. In a down round, investors often negotiate for stronger liquidation preferences as compensation for the additional risk they are taking on. A 1x non-participating liquidation preference means investors recover their invested capital before any proceeds flow to common shareholders, including founders.

Participating preferred stock is more aggressive: investors take their preference first and then also share in any remaining proceeds alongside common shareholders. Waterfall modeling — a financial analysis that maps out how exit proceeds flow through different share classes in various liquidation scenarios — is essential for founders to understand the real economic impact of these terms. In a low-exit scenario, even a 1x liquidation preference can absorb the entirety of proceeds, leaving founders with nothing despite years of work. Founders should always run waterfall models across a range of exit values before agreeing to any liquidation preference structure in a down round term sheet.

Are there alternatives to a down round that can reduce dilution risks for founders?

Yes, and exploring them thoroughly before accepting a down round is always advisable. Several non-equity funding and debt-based options can provide capital without immediately triggering equity dilution:

Venture debt is one common option — loans from specialized lenders that are repaid with interest, often with warrant coverage rather than direct equity issuance, which limits dilution.

Bridge financing can provide short-term runway while a company works toward better valuation metrics for a future equity raise.

Revenue-based financing allows companies to repay investors as a percentage of ongoing revenue, preserving ownership structure entirely.

Convertible debt, like SAFEs but structured as a loan, can also defer dilution until a later round.

Tranche financing — structured equity investments released in stages tied to milestones — can reduce the upfront dilution of a large capital raise.

Each of these alternatives has trade-offs in cost base and flexibility, and founders should work with financial advisors to model which path minimizes long-term dilution while meeting immediate capital needs.

How should founders think about cap tables and capitalization tables when preparing for a down round?

Cap tables — and the broader capitalization tables that reflect the full ownership structure of a company — are the single most important analytical tool in a down round. Before entering any negotiation, founders should have a completely up-to-date cap table that accurately reflects all issued shares, outstanding options from option pools, SAFEs, convertible notes, warrants, and pro-rata rights. This gives founders a precise picture of current ownership percentages and allows them to model the impact of proposed new terms before committing.

After a down round closes, the cap table must be immediately updated to reflect new share issuances, anti-dilution adjustments, and any SAFE or convertible note conversions. Using dedicated equity management software — such as Carta or Pulley — significantly reduces the risk of errors that can cause legal complications in future VC rounds. Founders who treat cap table modeling as an ongoing discipline, rather than an occasional exercise, are far better positioned to negotiate effectively and protect their equity.

How can a down round affect Board of Directors composition and founder voting power?

Down rounds frequently come with governance changes attached. New investors — and sometimes existing investors using the down round as leverage — will often negotiate for additional board appointment rights as a condition of their participation. This can shift the balance of the Board of Directors away from founders and toward investor-controlled seats, reducing the founder's ability to direct strategy, block decisions, or shape the company's future.

In more severe cases, founders may find that voting power on key issues is effectively transferred to the investor bloc, particularly if the shareholders agreement grants preferred stockholders consent rights over major decisions. Founders should also be aware of their fiduciary duties as board members, which require them to act in the interests of all shareholders — not just themselves — even during a down round negotiation. D&O insurance becomes especially important in these scenarios, as governance disputes arising from down rounds can lead to litigation. Founders should negotiate governance terms carefully, seeking to maintain meaningful voting power and limiting board appointment rights granted to new investors.

What signals does a down round send to the market, and how can founders manage market perception?

In private markets, information travels quickly, and a down round can affect market confidence in ways that go beyond the cap table. Potential employees, future investors, customers, and partners may interpret a down round as a sign that the company missed targets, faces existential challenges, or that management capabilities have been called into question. This is especially true in high-visibility sectors like AI startups, where valuations are closely tracked and covered by the press.

Founders must proactively manage market perception by crafting a clear, honest narrative that explains the context — whether it reflects broader market timing issues, a market peak correction, or a deliberate strategic pivot — rather than allowing others to define the story. Transparency with the existing investor base, supported by strong market research and market analysis, helps rebuild market confidence. A compelling pitch deck for future financing rounds should directly address the down round, frame the reset valuation as a new foundation for growth, and demonstrate with data how the company's growth potential remains intact despite the valuation curve having temporarily declined.

What steps should founders take immediately after closing a down round to protect their equity going forward?

The period immediately following a down round is critical for stabilizing and repositioning the company:

First, founders should update their capitalization tables and run fresh cap table modeling to fully understand the new ownership percentages and plan for future dilution scenarios, including potential secondary offerings or recapitalizations.

Second, founders should review all financing documents — including the corporate charter, shareholders agreement, and any amended governance terms — to confirm that all changes have been properly reflected in legal records.

Third, founders should communicate transparently with employees about the impact on option pools and outline a clear plan for ESOP refresh grants where appropriate, to protect company morale and retain key talent.

Fourth, founders should revisit their long-term fundraising strategy with updated valuation metrics, realistic milestone timelines, and a revised narrative that frames the down round as a recalibration rather than a failure.

Finally, a recap of the company's financial position — including a review of burn rate, cash runway, and exit planning scenarios — will help ensure that the new capital is deployed efficiently toward rebuilding the valuation curve needed to make future venture capital funding possible on better terms.

Legal Disclaimer

The information contained in this article is provided for general informational and educational purposes only and does not constitute legal, financial, investment, or professional advice of any kind. The content reflects the views and analysis of the authors based on publicly available information and general market observations, and should not be relied upon as a substitute for professional guidance tailored to your specific circumstances.

Equity structures, investment terms, and applicable laws vary significantly depending on jurisdiction, company structure, and individual situation. Down rounds, dilution, anti-dilution provisions, liquidation preferences, and related matters involve complex legal and financial considerations that can have material consequences for your business and personal finances.

Before making any decisions related to fundraising, equity, or corporate governance, you should always consult with a qualified attorney experienced in venture capital and startup law, as well as a licensed financial advisor or certified public accountant. Nothing in this article creates an attorney-client relationship, a financial advisory relationship, or any other professional relationship between the authors, Allied Venture Partners, and the reader.

Past market data and statistics referenced in this article are sourced from third parties and are believed to be accurate at the time of publication but are not guaranteed. Market conditions change rapidly, and this article may not reflect the most current legal, regulatory, or financial developments.

Allied Venture Partners is not a law firm and does not provide legal advice.