The Definitive Guide to the Role and Responsibilities of Lead Investors in Syndicates

Key Takeaways

Lead Investors are the linchpin of investment syndicates, serving as architect, negotiator, and steward throughout the entire investment lifecycle—from sourcing deals to post-investment support.

Syndicates democratize startup investing by allowing accredited angel investors to pool capital and access high-quality deals curated by experienced Lead Investors, often with minimum investments as low as $1,000.

The SPV structure streamlines investments by creating a Special Purpose Vehicle (LLC) for each deal, giving startups one clean cap table entry while providing liability protection and centralized management for all syndicate members.

Lead Investors earn 20% carried interest on profits after syndicate members recover their principal, directly aligning their financial success with the syndicate's performance while requiring significant personal investment as "skin in the game."

Pre-investment work is the most critical phase, involving masterful deal sourcing through deep networks, exhaustive due diligence across team, market, product, financials, and legal dimensions, and expert term sheet negotiation to secure favorable terms.

Rigorous selection is essential: at Allied VC, we review 1,500+ deals annually and invest in only the top 0.5%. Our diligence process includes a 100-point checklist.

Post-investment value creation separates great leads from good ones, including active mentorship, strategic guidance, network introductions, regular syndicate reporting, and crisis management support for portfolio companies.

Lead Investors manage ongoing relationships by coordinating pro-rata rights for follow-on funding rounds, helping founders prepare for future fundraising, and serving as the primary communication conduit between the company and syndicate members.

Success requires both science and art: technical expertise in deal mechanics, financial analysis, and legal structures must be combined with soft skills like relationship building, strategic judgment, reputation cultivation, and managing diverse stakeholder expectations.

The role demands significant commitment with asymmetric rewards—Lead Investors invest substantial time, effort, and expertise in exchange for the potential of outsized returns through carried interest on successful exits.

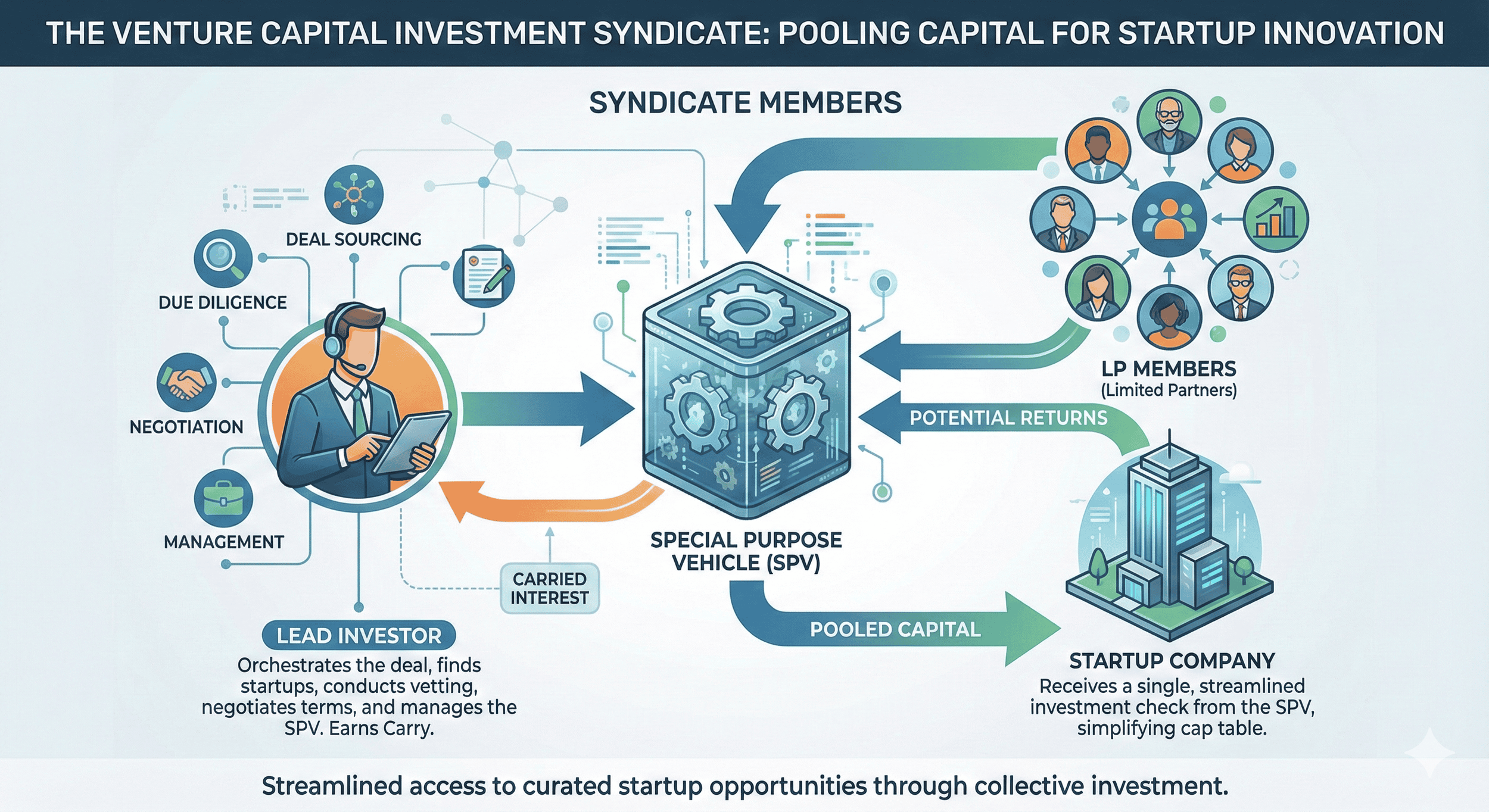

The Linchpin of Startup Syndicates

In the dynamic landscape of early-stage venture capital, investment syndicates have emerged as a powerful force, democratizing access to high-potential startups for a broader range of investors. At the heart of this collaborative funding model stands a pivotal figure: the Lead Investor. This individual is far more than a mere facilitator; they are the architect, conductor, and steward of the entire investment process. From unearthing promising companies to negotiating terms and guiding post-investment growth, the Lead Investor's expertise and commitment are the linchpin that holds a successful syndicate together.

What is an Investment Syndicate?

The Lead Investor orchestrates the syndicate, pooling capital from members into an SPV to make a single, streamlined investment into a startup.

An investment syndicate is a group of individual investors, often angel investors, who pool their capital to invest in a single funding round for a startup. Instead of each investor negotiating separately with the founders, they co-invest under the terms negotiated by a single, experienced Lead Investor. This structure allows startups to raise significant capital from multiple sources while streamlining their cap table and managing only one primary relationship. For syndicate members, it provides access to vetted investment opportunities they might not find on their own, often with smaller check sizes.

Real-world Example: Allied Venture Partners Angel Syndicate Overview

Allied Venture Partners is organized as an angel investor syndicate made up of high-net-worth individuals and family offices. Investors can join the syndicate at no cost and gain access to Allied's deal flow. The syndicate lead and Managing Director, Matthew Wilson, sources and negotiates each investment based on specific criteria. Syndicate members can then invest on a deal-by-deal basis, with a minimum of $1,000 USD. Funds are pooled into an SPV and invested in the target company as a single cap table entry. Matthew Wilson manages the ongoing relationship between the founder and syndicate, and shares company updates with individual investors.

The Crucial Role of the Lead Investor

The Lead Investor is the syndicate's designated expert and representative. They are responsible for sourcing the investment opportunity, conducting comprehensive due diligence, negotiating the investment terms, and managing the syndicate's relationship with the company post-investment. This role demands a unique combination of financial acumen, industry expertise, strong networks, and leadership skills. They are the trusted agent for the syndicate members, who rely on the lead's judgment and diligence when committing their funds.

Why This Guide Matters: Navigating the Complexities

Stepping into the role of a Lead Investor is a significant undertaking with asymmetric rewards and substantial responsibilities. Success requires a deep understanding of the mechanics of deal-making, the nuances of legal structures like the Special Purpose Vehicle (SPV), and the art of managing diverse stakeholder expectations. This definitive guide will dissect every facet of the Lead Investor's role, providing a comprehensive playbook for aspiring leads, a clear framework for founders seeking syndicate funding, and valuable insights for investors considering joining syndicates.

Understanding the Foundation: What Defines a Lead Investor in a Syndicate?

Before diving into the intricate responsibilities, it's essential to establish a clear understanding of the foundational concepts. The effectiveness of the entire syndicate model hinges on the capabilities and definition of the Lead Investor, who operates as the central node in this collaborative network.

Investment Syndicates: A Collaborative Funding Mechanism

At their core, investment syndicates are a solution to a market inefficiency. High-growth startups need capital and expertise, while many accredited angel investors have capital and expertise but lack the time or access to consistently find and vet the best deals. Syndicates bridge this gap. By pooling their funds, investors can participate in larger, often more competitive, funding rounds. The structure, typically managed through an online platform (like AngelList) or a legal entity, simplifies the investment process for everyone involved. The startup gains a single, organized entry on its cap table instead of dozens of individual investors, and syndicate members gain access to deals curated by a trusted expert.

Defining the Lead Investor: The Orchestrator and Anchor

The Lead Investor is typically an experienced angel investor, a former founder, or a domain expert with a proven track record of successful investments. They are not merely the first person to commit capital; they are the anchor of the deal. Their credibility, network, and willingness to perform the heavy lifting of due diligence are what attract other investors to the opportunity. The lead's personal investment in the deal—their "skin in the game"—serves as a powerful signal of conviction, aligning their interests directly with those of the syndicate members who follow them. They are the primary fiduciary, acting on behalf of the group and making critical decisions that will shape the investment's future.

The Pre-Investment Phase: Strategic Sourcing, Rigorous Vetting, and Deal Structuring

The bulk of a Lead Investor's most critical work occurs before a single dollar is transferred. This pre-investment phase is where opportunities are discovered, risks are mitigated, and the foundation for a successful investment is meticulously laid.

Masterful Deal Sourcing and Curation

Exceptional deal flow is the lifeblood of a successful Lead Investor. It's not about seeing every possible deal, but about cultivating access to high-quality, often proprietary, investment opportunities. This is achieved through several channels:

Deep Networks: Strong relationships with founders, venture capitalists, attorneys, and other angel investors are a primary source of referrals.

Industry Expertise: A reputation as a thought leader in a specific sector (e.g., FinTech, HealthTech) makes a lead a magnet for relevant startups seeking smart capital.

Proactive Outreach: Top leads don't just wait for deals to come to them. They actively research emerging trends and identify promising founders early in their journey.

Platform-Based Sourcing: Utilizing syndicate platforms can broaden access to a curated stream of potential deals beyond a personal network.

The Lead Investor acts as a curator, filtering through numerous startups to present only the most compelling opportunities to their syndicate network.

Real-world Example: Allied Venture Partners Deal Sourcing Process

At Allied VC, we have a five-part deal flow funnel:

Cold inbound pitch application

Referrals from portfolio company founders and syndicate members

Networking and outreach (e.g., industry conferences, podcasts, speaking engagements)

Connections through our extensive network of co-investors and VCs

In aggregate, we review more than 1,500 deals per year and invest in the top 0.5%.

The Lead Investor's Advanced Due Diligence Imperative

Once a promising company is identified, the Lead Investor embarks on an exhaustive due diligence process. This is the most labor-intensive part of the role and where the lead provides immense value to the syndicate members. While every deal is unique, a comprehensive diligence checklist typically covers:

The Team: Assessing the founders' experience, resilience, coachability, and vision. Is this the right team to navigate the challenges of building a massive company?

Market Opportunity: Validating the size of the target market (TAM, SAM, SOM), understanding the competitive landscape, and confirming a genuine customer pain point.

Product & Technology: Evaluating the product's defensibility, scalability, and traction. This may involve user interviews, product demos, and technical reviews.

Business Model & Financials: Scrutinizing the company's financial projections, unit economics, revenue model, and capital efficiency. The current selective investment environment, where funds from the 2022 vintage have deployed only 43% of their capital after 24 months, underscores the need for leads to be exceptionally diligent about financial sustainability.

Legal & Cap Table Review: Examining the company's corporate structure, intellectual property, and existing capitalization table to identify any red flags.

This rigorous vetting process is designed to build a strong investment thesis and uncover potential risks that could jeopardize the syndicate's capital. With the probability of achieving a 5x return on a venture investment being around 15%, meticulous diligence is non-negotiable.

Real-world Example: Allied Venture Partners Due Diligence Process

At Allied VC, we have developed a robust, proprietary 100-point diligence checklist; the result of investing in more than 100 startups since 2012, including multiple unicorns.

Expert Term Sheet Negotiation and Investment Structure

Armed with insights from due diligence, the Lead Investor negotiates the investment terms with the founders. Their goal is to secure a deal that is fair to the company while providing strong protections and upside potential for the syndicate investors. Key negotiation points include:

Valuation: Determining a pre-money valuation that reflects the company's progress, potential, and market comparables.

Investment Instrument: Deciding between equity (e.g., preferred stock) or a convertible instrument (e.g., SAFE or convertible note).

Investor Rights: Negotiating for crucial provisions such as pro-rata rights (the right to maintain ownership percentage in future funding rounds), information rights, and a potential board seat or observer rights.

Liquidation Preferences: Structuring how proceeds are distributed in an exit scenario to protect the syndicate's principal investment.

A skilled lead balances the need for favorable terms with the importance of building a positive, long-term relationship with the founders.

Real-world Example: Allied Venture Partners Investment Structure

At Allied VC, our average post-money valuation for initial seed-stage investments is $9.3 million, with a maximum post-money valuation of $25 million for initial Series A investments. We invest only in startups that are post-product and generating at least $5,000 in monthly revenue. Our investments are made through preferred stock, convertible notes, or SAFEs; we do not invest in common stock. We require pro rata rights with all initial investments, as well as regular updates from the founder (either monthly or quarterly). We do not take board seats, but may assume a board observer role once a formal board of directors is established, typically at the Series A stage.

The Investment Execution Phase: Assembling and Managing the Syndicate

With a term sheet agreed upon, the Lead Investor shifts from analyst and negotiator to manager and administrator. This phase involves assembling the capital, formalizing the legal structure, and executing the investment.

Building and Aligning the Syndicate

The lead's next task is to present the investment opportunity to their network of potential syndicate members. This involves creating a concise and compelling deal memo that summarizes the investment thesis, due diligence findings, and key deal terms. Transparency is paramount. The lead must clearly articulate both the potential rewards and the inherent risks. They answer questions from prospective co-investors, vet their accreditation status, and secure capital commitments. A strong lead often curates a syndicate that includes members who can add strategic value to the startup beyond just their capital.

Legal and Structural Setup: Mastering the Special Purpose Vehicle (SPV)

To manage the pooled funds and streamline the company's cap table, syndicates almost universally use a Special Purpose Vehicle (SPV). The SPV is a new legal entity, typically a Limited Liability Company (LLC), created for the sole purpose of making that one investment. The Lead Investor acts as the Managing Member of the SPV. All syndicate members become investors in the SPV, and the SPV, in turn, makes a single investment into the startup. This structure is highly efficient:

For Founders: They receive one line item on their cap table (e.g., "Syndicate Name SPV, LLC") instead of dozens of individuals.

For Investors: It provides liability protection and centralizes management and communication through the Lead Investor.

For the Lead: It formalizes their administrative role and is the vehicle through which they receive carried interest.

Setting up an SPV involves legal and administrative costs, which are typically passed on to the syndicate members.

Real-world Example: Allied Venture Partners Syndicate Legal Structure

Allied VC utilizes the AngelList platform to streamline the formation and management of Special Purpose Vehicles (SPVs). For each SPV, a one-time setup fee is allocated pro rata among participating investors. This fee covers both the initial establishment and ongoing management of the SPV, including the preparation of annual tax documents and the distribution of funds, for the entire lifespan of the SPV.

Capital Call and Closing Process

Once the target funding amount for the syndicate is committed, the Lead Investor initiates a "capital call," instructing syndicate members to wire their funds to the SPV's bank account. The lead works with legal counsel to finalize all closing documents, including the SPV's operating agreement and the subscription agreement with the startup. After all funds are collected and documents are signed, the SPV wires the total investment amount to the company, officially closing the funding round. The lead ensures all administrative details are handled correctly, providing a seamless experience for both the investors and the founders.

The Post-Investment Phase: Value Creation, Governance, and Ongoing Stewardship

The Lead Investor's work is far from over once the deal closes. In many ways, the most important phase is just beginning. A great lead transitions from dealmaker to active partner, dedicated to helping the company succeed and maximizing the return for the syndicate.

Active Portfolio Management and Mentorship

Unlike passive investors, a dedicated Lead Investor actively supports their portfolio companies. This can take many forms:

Strategic Guidance: Offering advice on product strategy, go-to-market plans, and key hiring decisions.

Network Access: Making valuable introductions to potential customers, partners, and future investors.

Mentorship: Serving as a trusted sounding board for the founders, helping them navigate the inevitable challenges of startup life.

This hands-on support can be a critical factor in a startup's success, providing value far beyond the initial capital invested.

Syndicate Reporting and Ongoing Communication

The Lead Investor is the primary conduit of information between the company and the syndicate members. They are responsible for establishing a regular reporting cadence to keep investors informed about the company's progress. This typically includes quarterly updates summarizing key performance indicators (KPIs), product milestones, financial performance, and any significant challenges or opportunities. Proactive and transparent communication builds trust and manages expectations within the syndicate, especially during difficult periods.

Pro tip: when working with an investment syndicate, founders should always aim to maximize the syndicate network's value by sharing regular updates and including strategic asks.

Guiding Future Fundraising Rounds and Managing Pro Rata Rights

As the company grows, it will likely need to raise additional capital. The Lead Investor plays a crucial role in this process. They help the founders prepare for subsequent funding rounds, make introductions to venture capital funds, and advise on strategy. A key responsibility is managing the syndicate's pro-rata rights. The lead will assess whether exercising these rights to invest in a follow-on round is in the syndicate's best interest, and if so, they may form a new SPV to gather the necessary capital from existing or new syndicate members.

Strategic Problem-Solving and Crisis Management

Startups are inherently volatile. When a portfolio company faces a crisis—whether it's a co-founder dispute, a product failure, or a market downturn—the Lead Investor is often the first call. They act as a steady hand, helping the team diagnose the problem, brainstorm solutions, and make tough decisions. Their experience and objective perspective are invaluable in navigating these critical moments and helping the company get back on track.

The Financials and Incentives Driving a Lead Investor

The Lead Investor role requires a massive commitment of time, effort, and expertise. To compensate for this work, a specific incentive structure has become standard in the industry, aligning the lead's financial success with that of their syndicate members.

Carried Interest (Carry): The Primary Incentive Structure

The primary financial incentive for a Lead Investor is "carried interest," or "carry." This is a share of the syndicate's profits from an investment. A typical carry structure is 20%. This means that after all syndicate members have received their original investment back upon a successful exit (e.g., an acquisition or IPO), the Lead Investor receives 20% of the remaining profits, with the other 80% distributed to the syndicate members pro-rata. This model directly rewards the lead for sourcing, managing, and supporting a successful investment. According to analysis from AngelSchool.vc, syndicate leads can earn significantly higher carry than VC fund GPs on a per-deal basis, highlighting the powerful upside of this model.

Personal Investment: Skin in the Game as an Anchor Investor

To ensure alignment, it is standard practice for the Lead Investor to make a significant personal investment in the deal. This "skin in the game" demonstrates their conviction to other syndicate members and ensures their financial interests are directly tied to the outcome. The lead's personal check is often one of the largest in the syndicate, cementing their status as the anchor investor and reinforcing their commitment to the startup's success.

Understanding Investment Costs and Liabilities

While the upside is significant, leads also manage certain costs and liabilities. The legal and administrative expenses associated with setting up the SPV and closing the deal are typically paid by the syndicate investors, often deducted from their initial investment or paid as a one-time administrative fee. The Lead Investor, as the manager of the SPV, has a fiduciary responsibility to act in the best interests of the syndicate members. This requires a high degree of ethical conduct, transparency, and careful management of potential conflicts of interest.

The "Art" of Lead Investing: Beyond Mechanics and Towards Strategic Leadership

Executing the technical responsibilities of a Lead Investor is the science of the role. However, what separates good leads from great ones is the "art"—the collection of soft skills, strategic judgment, and relationship-building prowess that drives exceptional outcomes.

Cultivating a Powerful Personal Brand and Reputation

A Lead Investor's reputation is their most valuable asset. A strong track record of successful investments, ethical conduct, and providing genuine value to founders builds a powerful personal brand. This brand attracts higher-quality deal flow, as the best founders want to work with respected investors. It also makes it easier to assemble syndicates, as other investors are more willing to trust and follow a lead with a history of success and integrity.

Nurturing the Founder-Lead Relationship

The relationship between the founders and the Lead Investor is a long-term partnership. Great leads invest time in building trust, rapport, and open lines of communication. They act as a supportive mentor, not a micromanager. They understand that their role is to empower the founders, providing guidance and resources without stifling their autonomy. This strong, collaborative relationship is essential for navigating the ups and downs of the startup journey.

Navigating and Harmonizing Syndicate Dynamics

Managing a group of diverse investors, each with their own expectations and communication styles, requires skill. A successful lead sets clear expectations from the outset, communicates proactively, and is adept at managing different personalities within the syndicate. They must be able to deliver both good and bad news with transparency and maintain the confidence of the group, ensuring that all syndicate members feel informed and respected throughout the investment lifecycle.

Strategic Acumen and Decisive Judgment

Ultimately, a Lead Investor is a decision-maker. They must possess the strategic acumen to identify true market shifts and the decisive judgment to act on them. They need to be able to see beyond the hype of trending sectors like AI, which attracted 28% of all venture dollars in Q3 2024, and focus on a company's fundamental business viability. This involves pattern recognition honed over years of experience, the courage to pass on a seemingly popular deal that doesn't meet their criteria, and the conviction to back visionary founders in overlooked markets.

Summary: The Role of Lead Investors in Syndicates

The role of the Lead Investor is a demanding, multifaceted discipline that sits at the intersection of finance, strategy, and human relationships. They are the engine of the modern investment syndicate, shouldering the immense responsibility of sourcing deals, conducting rigorous due diligence, negotiating terms, and providing invaluable post-investment support. This comprehensive effort not only opens doors for syndicate members to participate in curated, high-potential investment opportunities but also provides founders with streamlined access to capital and a dedicated, expert partner.

For those aspiring to take on this role, the path requires building a strong network, developing deep industry expertise, and cultivating an unwavering commitment to integrity and transparency. For founders, understanding the Lead Investor's function is key to unlocking the power of syndicate funding. As the venture landscape continues to evolve, the skill, judgment, and leadership of the Lead Investor will remain the indispensable element that transforms a group of individual investors into a cohesive, value-adding force for the next generation of groundbreaking startups.

Frequently Asked Questions (FAQ)

General Questions About Investment Syndicates

What is an investor syndicate and how does it differ from traditional venture funds?

An investor syndicate is a group of accredited investors who pool their capital to invest in startups on a deal-by-deal basis, with a Lead Investor coordinating the process. Unlike traditional venture funds that raise a large pool of capital upfront and deploy it across multiple investments, angel syndicates operate on a deal-centric model where each limited partner chooses which syndicated investments to participate in. Venture funds typically have a Limited Partnership Agreement covering multiple investments, while investor syndicates create a new investment vehicle (SPV) for each deal. This makes angel syndicates more flexible for both Limited Partners (LPs) and Leads who want to maintain control over their investment strategy and investment goals.

How do platforms like AngelList facilitate syndicate investments?

AngelList has revolutionized angel investing by providing infrastructure for forming and managing angel syndicates. The platform streamlines the creation of SPVs (Special Purpose Vehicles) as the primary investment vehicle, handles legal formalities, provides automated cap tables, and manages ongoing administration, including tax documents. AngelList connects accredited investors with experienced Lead Investors, allowing limited partners to access curated deal flow they might not find independently. The platform also simplifies the process of reviewing pitch decks, conducting due diligence, and closing syndicated investments, making startup investing more accessible while maintaining necessary legal and tax support.

Who can participate in angel syndicates, and what are the requirements?

Participation in angel syndicates is generally limited to accredited investors as defined by the Securities and Exchange Commission. Accredited investors must meet certain income thresholds (typically $200,000+ annually for individuals) or net worth requirements ($1 million+ excluding primary residence). These requirements fall under Regulation D exemptions that allow private securities offerings. Many angel syndicates have minimum investment amounts ranging from $1,000 to $25,000 per deal, making startup funding more accessible than traditional venture capital while still complying with securities regulations. Co-investors in syndicates benefit from the Lead's expertise and network while maintaining the flexibility to choose deals aligned with their risk appetite.

Lead Investor Roles and Responsibilities

What distinguishes a Lead Investor from other co-investors in syndicated investments?

The syndicate Lead serves as the primary decision-maker and manager of the investor syndicate, taking on significantly more responsibility than other co-investors. They source deals, conduct comprehensive due diligence (including reviewing the startup's financials, pitch decks, and ESOP structure), negotiate terms, and manage the post-investment relationship. Leads create investment memos to present opportunities to syndicate members and act as the Managing Member of the SPV. Their compensation typically includes 20% carried interest on profits, reflecting the substantial work involved. Other co-investors, as limited partners, rely on the Lead's expertise and judgment while choosing which deals to support based on their own investment goals.

How do Lead Investors provide ongoing value after making an investment?

Post-investment, Lead Investors transition from dealmakers to active partners, providing mentorship and strategic guidance to founders. They facilitate introductions to potential customers, follow-on investors, and venture capital firms for the next round of funding. Leads manage syndicate communication through regular reporting on company progress and coordinate the exercise of pro-rata rights in follow-on rounds (including bridge rounds or Series B). They also help navigate crises and strategic decisions, leveraging their experience across multiple startup investments. This ongoing support distinguishes angel syndicates from passive investment funds and can significantly impact a startup's trajectory, particularly for early-stage companies from series seed through later stages.

What is the difference between lead-centric and deal-centric syndication models?

In a lead-centric model, LPs primarily follow a specific syndicate Lead based on their track record, expertise, and reputation, committing to invest in most or all deals the lead presents. In a deal-centric model, investors evaluate each opportunity independently, choosing to participate based on the specific startup's merits rather than automatically following the lead. Most modern angel syndicates operate on a deal-centric basis, allowing accredited investors flexibility to align investments with their personal investment strategy. However, Lead Investors with strong reputations in specific sectors (like SaaS or FinTech) often develop syndication relationships with familiar syndicate partners who regularly participate, creating a hybrid model that combines elements of both approaches.

Practical Investment Considerations

How do angel syndicates compare to venture capital in terms of investment size and stage focus?

Angel syndicates typically invest smaller amounts ($50k-$500k) at earlier stages (pre-seed through Series A) compared to venture funds, which often invest $2M-$50M+ in later stages. This makes angel investing ideal for founders seeking startup funding before they're ready for lead-type VC firms. Syndicates can move faster than institutional venture capital, often closing deals in weeks rather than months. However, the deal-by-deal nature means angel syndicates don't guarantee follow-on capital like some venture funds. Many startups use syndicates for initial rounds, then transition to venture capital for growth stages like Series B. Some founders attend events like SaaStr to connect with both angel syndicates and venture funds simultaneously.

What due diligence do Lead Investors conduct before presenting deals to their syndicate?

Lead Investors conduct exhaustive due diligence covering multiple dimensions. They assess the founding team's capabilities, validate the market opportunity and competitive landscape, and analyze the business model (particularly important for SaaS companies with recurring revenue). Financial analysis includes scrutinizing the startup's financials, unit economics, and capital efficiency. Legal reviews cover corporate structure, intellectual property, cap table issues, and any venture debt financing. Technical evaluation examines product defensibility and scalability. Lead Investors also reference-check with familiar partners, co-investors, customers, and other market participants to understand the market landscape. This rigorous process, often documented in detailed investment memos, helps protect syndicate members from avoidable risks and ensures only high-quality opportunities reach accredited investors.

How are private syndicates structured legally, and what protections exist for investors?

Private syndicates typically use a Special Purpose Vehicle (SPV), usually a Limited Liability Company (LLC), as the investment vehicle for each deal. The Lead Investor serves as Managing Member, while syndicate members become limited partners in the SPV. This structure provides liability protection and centralizes management. Each SPV has an operating agreement outlining rights, responsibilities, and profit distribution. The SPV makes a single investment into the startup, simplifying the company's cap table.

Legal professionals typically handle the formation, ensuring compliance with securities regulations and Regulation D exemptions. The structure includes provisions for information rights, pro-rata rights for follow-on rounds, and liquidation preferences. While this provides important protections, accredited investors should understand that startup investing carries inherent risks, and the SPV structure doesn't eliminate investment risk—it primarily provides organizational efficiency and legal clarity for all parties involved in syndicated investments.