How to Build Relationships With Investors

Key Takeaways

Lead with transparency: share the real picture, including what isn't working, to preserve board trust when it matters most.

Systematize your updates: consistent investor updates for startups prevent relationship drift and keep strategic capital close.

Build early: warm relationships opened 6–12 months before a raise reduce friction and compress your fundraising timeline.

Treat investors as operators: the more aligned they are with your execution reality, the more leverage you unlock from the relationship.

That judgment doesn't stop at the close. It compounds over every interaction that follows.

The Shift from Transactional Pitching to Strategic Partnership

Founders who understand how to build relationships with investors (not just close them) consistently outperform those who treat fundraising as a one-time event.

The term sheet is a beginning, not an endpoint. Once capital transfers, the real relationship starts: board seats are filled, follow-on decisions get made, and introductions to customers, partners, and future co-investors flow through the same people who wrote the first check. Investor data shows us that a significant majority of institutional investors rank management team quality as a critical factor in their investment decision — often ahead of the product itself. That judgment doesn't stop at the close. It compounds over every interaction that follows.

The founders who attract follow-on funding at the highest rates aren't necessarily those with the cleanest metrics at Series A. They're the ones whose investors feel genuinely informed, actively involved, and confident in the team's judgment. Relationship depth, built through consistent communication, honest reporting, and shared problem-solving, is what converts a passive capital provider into an advocate who leads your next round.

This requires a fundamental mindset shift: from convincing to collaborating. Pitching is a performance; partnership is an ongoing exchange. When founders approach investors as operator-partners (i.e., people with pattern recognition, network access, and domain experience that complements the founding team), the dynamic changes from transactional to strategic. Allied Venture Partners is built on exactly this model, connecting early-stage software founders with a diverse operator network that stays engaged well beyond the initial check. You can explore how that investment philosophy works before our first conversation.

That shift in dynamic, toward openness, shared stakes, and honest dialogue, is where the real alpha lives. And it starts with one non-negotiable principle: no surprises.

The 'No Surprises' Rule: Cultivating Extreme Transparency

Knowing how to manage startup investor relationships starts with one uncomfortable truth: investors can handle bad news far better than they can handle surprises.

Hiding problems doesn't protect your relationship; it destroys it. When founders obscure a missed milestone, delay sharing a key departure, or soften a burn rate concern, they're not buying time. They're eroding the credibility that took months to build. Board members and syndicate investors alike operate on imperfect information; the moment they sense that information is being managed rather than shared, trust degrades fast.

The 'No Surprises' mandate is the bedrock of every high-functioning founder-investor relationship. It's a simple operating principle: communicate material developments (positive or negative) before your investor hears about them elsewhere. In practice, this means a difficult conversation today is almost always preferable to a damaged relationship next quarter.

"The best founder-investor relationships are built on a foundation of 'extreme transparency,' especially when things are going wrong." — Andreessen Horowitz (a16z)

a16z's perspective here isn't idealistic; it's analytical. During a pivot, founder integrity is stress-tested in real time. Investors who receive candid, early disclosure can mobilize their networks, adjust expectations internally, and become active problem-solvers. Founders who surface issues late, however, leave investors reactive and often defensive. The difference in outcome is significant, particularly when you consider that fewer than 15% of seed-funded startups reach Series A — a milestone that depends heavily on sustained investor confidence.

Transparency also expands what investors can actually do for you. A well-informed investor can make a warm introduction, flag a competitive risk, or redirect a hiring search. An investor managing information gaps can do none of those things effectively.

The structural mechanics of building that transparency consistently through regular, formatted updates is where the real leverage lies.

Operationalizing Trust with Monthly Update Frameworks

Transparency isn't a mindset shift alone; it requires a repeatable system that keeps investors informed without pulling founders away from building.

According to Visible.vc, founders who send regular monthly updates see measurably higher rates of follow-on funding and stronger investor NPS scores. The mechanism is straightforward: consistent communication signals operational discipline, and disciplined operators attract capital when they need it most. That's true whether you're managing current investors or thinking about how to approach investors for your next round.

The most reliable structure for a monthly update is the Highlights, Lowlights, and Asks framework. It's deliberately simple, which is exactly the point. Here's what each section should cover:

Highlights: Key wins since the last update — revenue milestones, product launches, new hires, or customer validation that moves the narrative forward

Lowlights: Honest reporting on what isn't working — an unexpected churn increase, a missed target, a hiring challenge. This is where trust compounds fastest

Asks: Specific, actionable requests your investors can actually fulfill — an intro to a potential enterprise customer, a referral to a CFO candidate, or a sanity check on a pricing decision

The "Asks" section is where passive investors become active partners. Most founders leave it blank or keep it vague. That's a missed opportunity. When you frame a request around someone's specific expertise or network, you make it easy for them to add value, and people who add value feel invested in your outcome.

Monthly updates are the standard for Seed and Series A companies. Quarterly updates work for later-stage investors managing larger portfolios, but at early stages, how your cap table evolves and your key metrics evolve so fast that monthly context keeps everyone aligned. Longer gaps create information vacuums, and investors fill vacuums with assumptions.

Building this habit now also shapes how future investors perceive your company before you ever send a pitch deck.

How to Approach Investors Before You Need the Capital

Strong investor relationships are often built well before a term sheet is on the table. Effective investor relationship management for founders isn't a fundraising activity; it's a continuous practice that begins long before you open a round.

The 'advice-first' outreach is one of the most underused levers at a founder's disposal. Instead of leading with a pitch, you open with a question: "We're solving X problem in Y market — would you be open to sharing your perspective on how you see this space evolving?" This framing removes the transactional pressure from the conversation and lets the investor engage as an expert, not an evaluator. A genuine exchange of ideas is far more memorable than a cold deck.

Building your target list requires more precision than filtering by check size alone. According to Harvard Business Review, a majority of venture capital firms identify deal sourcing and selection as critical stages of the investment process, which means investors are actively looking for founders who fit their thesis. Research each firm's portfolio, stated sector focus, and the stage at which they've historically led rounds. Understanding whether you fit within milestone-based funding criteria before your first conversation signals the kind of rigor investors want to see.

Warm introductions remain the dominant currency in early-stage venture. A LinkedIn analysis of startup fundraising dynamics consistently finds that operator networks (i.e., advisors, fellow founders, portfolio company executives) are the most reliable path to a credible introduction. Cold outreach can work, but it carries a much higher friction cost.

Structured platforms like 'Pitch Us' portals offer a third path that's often overlooked. Submitting through a formal intake process at a network like Allied Venture Partners creates a documented record of your company's trajectory, even if the timing isn't right for an immediate investment. It positions you for re-engagement when your metrics align with what investors are looking for.

Understanding how you'll eventually return value to your investors is the natural counterpart to everything discussed above — a topic the next section addresses directly.

The Exit Strategy: How Investors Are Paid Back

Venture capital is fundamentally an equity game: investors don't collect monthly interest payments; they realize returns when shares are sold during a liquidity event. Understanding that mechanic isn't optional for founders who want to build genuinely aligned relationships with their cap table.

"Paying back" investors means growing equity value, not retiring a debt.

As the Allied Venture Partners Educational Series notes, equity-based capital means returns flow from liquidity events, not from the business writing a check back to investors on a schedule.

The two primary paths to liquidity are M&A (a strategic or financial buyer acquires the company) and an IPO (in which shares are listed on a public exchange). M&A events are far more common at the early stage; IPOs remain the exception, typically reserved for companies with the scale and revenue profile to withstand public-market scrutiny. In practice, most Seed and Series A investors are underwriting to a trade sale outcome.

Secondary markets add a third dimension, particularly at Series B and beyond. Secondary transactions allow early investors or employees to sell shares to new investors before a formal liquidity event, providing partial liquidity without requiring the company to exit. For founders, understanding this dynamic matters: secondary activity can shift cap table composition and influence governance dynamics heading into later rounds.

The mechanics most founders underestimate are liquidation preferences and participation rights. A 1x non-participating preference means an investor recoups their investment before common shareholders receive anything in an exit. Participating preferred structures go further, allowing investors to "double-dip" (i.e., recover their preference and share in the remaining proceeds). If you're structuring a round, reviewing how these terms layer across your cap table before signing is essential.

It's a useful reminder that the founder-investor relationship isn't about minimizing losses; it's about building toward the outcome that justifies the risk for everyone on the cap table.

With that financial context established, it's worth examining what can go wrong when the relationship itself breaks down, because misaligned incentives and poor communication don't just slow momentum, they can actively destroy value.

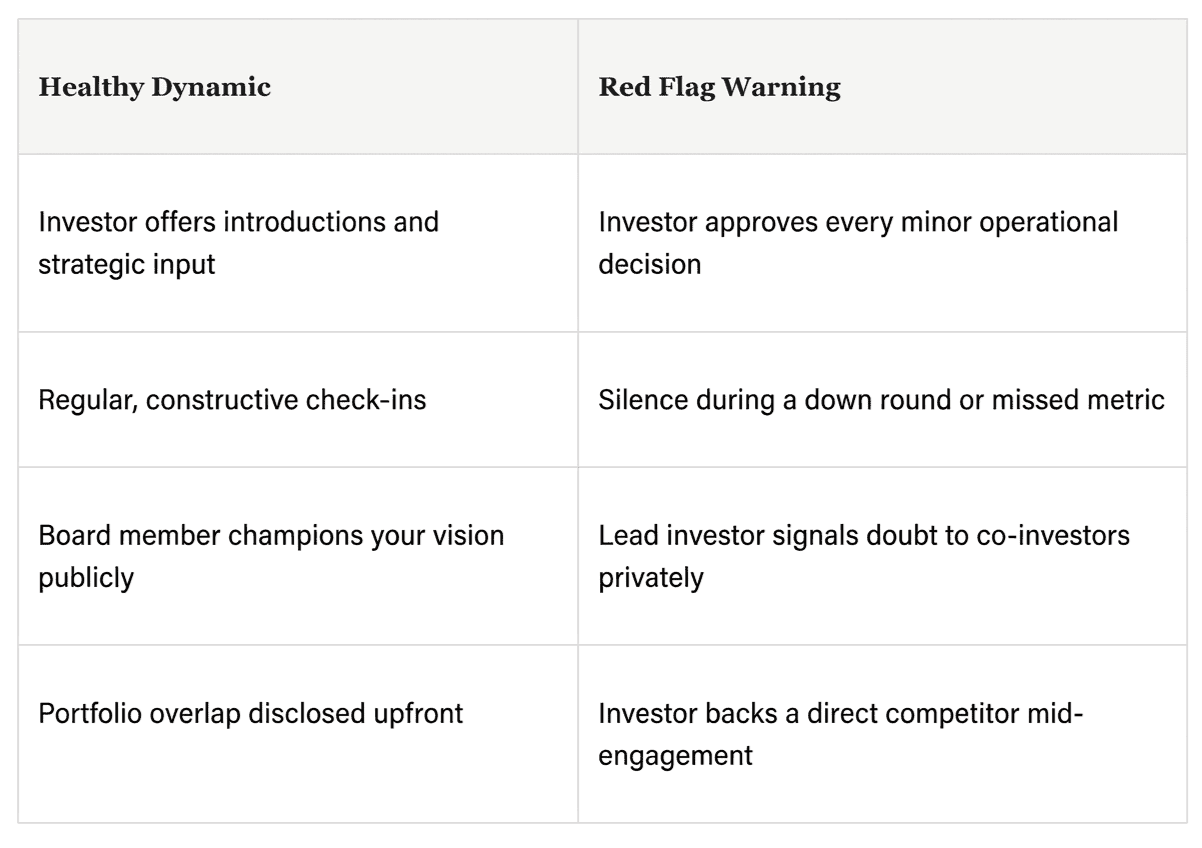

Red Flags: When the Founder-Investor Dynamic Turns Toxic

Relationship decay rarely announces itself. It shows up quietly in delayed reply times, shifted board dynamics, and conversations that feel more like audits than strategy sessions. Understanding how to spot misalignment early is just as important as understanding how investors are paid back, because a deteriorating relationship can derail your next round long before a down round forces the issue.

A toxic cap table can block future funding entirely. New investors at Series A will run due diligence on your board relationships, and perceived misalignment between founders and existing backers is a known deal-killer in venture capital. What starts as a "difficult" dynamic can harden into a structural problem that no pitch deck can fix.

Micromanagement tends to surface when an investor loses confidence but hasn't yet said so directly. The inverse: the silent investor who goes dark during a down round, is equally damaging, because you lose both their operational support and their signal to the broader market. If a lead investor is backing a direct competitor, that conflict of interest needs to be addressed head-on through your counsel, not managed around.

When a lead investor loses faith in your vision, the most productive move is a structured, documented conversation that either realigns expectations or begins the process of transitioning their role on the board. Founders who address this proactively, rather than letting friction compound, protect their cap table integrity and their standing with incoming investors. The patterns you establish now, in how you handle conflict and communicate under pressure, set the foundation for the kind of partnership covered in the next section.

The Bottom Line: Building a Partnership That Scales

Founder-investor alpha isn't won at the term sheet; it's accumulated through every interaction that precedes and follows it.

The through-line across everything covered in this article is simple: transparency isn't a soft skill, it's a structural advantage. Boards that receive honest, consistent communication make faster decisions, extend more goodwill during hard quarters, and unlock strategic introductions at the right moments. Those who don't spend their energy managing information gaps instead of building the company.

Investor updates for startups are the most underutilized lever in that equation. A well-structured monthly update (one that leads with metrics, flags risks early, and closes with a specific ask) keeps your investors activated between board meetings. It signals operational discipline. It also means that when you need to make a strategic ask, you're not re-establishing context from scratch. According to Entrepreneur Magazine, the strongest relationships are those where the investor feels like an extension of the executive team, and that dynamic is built through cadence, not just chemistry.

Timing matters here, too. Relationship-building before a raise works best when it starts 6–12 months before you need the capital. Investors who've watched your trajectory, who've seen you hit the growth benchmarks that matter at each stage, are far more likely to move quickly when a round opens. Cold outreach at the moment of fundraising forces investors into a trust-building sprint that rarely ends well for either side.

Four principles to carry forward:

Lead with transparency: share the real picture, including what isn't working, to preserve board trust when it matters most.

Systematize your updates: consistent investor updates for startups prevent relationship drift and keep strategic capital close.

Build early: warm relationships opened 6–12 months before a raise reduce friction and compress your fundraising timeline.

Treat investors as operators: the more aligned they are with your execution reality, the more leverage you unlock from the relationship.

Choosing the right network to build those relationships through is the logical next step, and it's worth thinking carefully about what that network can actually offer you.

Leveraging the Allied Venture Partners Network

Transparency earns trust, but the right network determines how far that trust can take your company. Everything covered in this article (proactive disclosure, structured communication cadences, navigating conflict, and avoiding red flags that erode partnerships) ultimately depends on being connected with investors who operate on the same principles.

Allied Venture Partners is built for founders who are ready to apply these practices at the Seed and Series A stages. Our fee-free pitching process eliminates a barrier that often causes early-stage founders to delay or limit their outreach. There's no cost to submit your pitch through the Pitch Us portal, which means founders can pursue early investor visibility without compromising runway or waiting until terms are already on the table.

What separates the Allied Venture Partners syndicate model from a traditional fund isn't just structure; it's the operator network behind it. Investors in the network aren't passive capital providers. They're operators with domain expertise who can contribute strategic context alongside their investment, which is precisely what makes transparency a productive exercise rather than a one-way reporting obligation. When your investors understand your industry from the inside, your honest updates lead to sharper guidance.

The syndicate model is also practical for Seed and Series A growth. Founders gain access to diversified capital without managing multiple disconnected relationships, while accredited angel investors can build curated, high-growth venture portfolios without membership fees. Both sides benefit from a structure designed around alignment. You can explore how this plays out across funding stages in the many startup and investor guides Allied publishes for the ecosystem.

If you're building a software company in North America and ready to raise capital with transparency, submit your pitch to Allied Venture Partners (at no cost) and connect with a network that treats operator insight as a core part of the investment.

Frequently Asked Questions

What is the most important principle in how to build relationships with investors after a round closes?

Extreme transparency is the foundation. The "No Surprises" rule means communicating material developments — positive or negative — before your investor hears about them elsewhere. Investors can handle bad news; what they can't recover from is feeling like information was managed or withheld. Every honest update you send compounds trust over time, which directly influences follow-on funding decisions and the quality of strategic support you receive.

How to manage startup investor relationships on an ongoing basis without losing focus on building the company?

The most effective approach is a repeatable monthly update framework built around three sections: Highlights, Lowlights, and Asks. The structure is intentionally simple so it doesn't pull founders away from operations. The "Asks" section is particularly high-leverage — specific, actionable requests convert passive investors into active partners who feel invested in your outcome. Consistency matters more than polish here. Investors filling information vacuums with assumptions is one of the most common and avoidable sources of relationship drift.

What's the best way to approach investors before you're actively fundraising?

Lead with an advice-first framing rather than a pitch. Opening with a genuine question about how an investor sees your market removes the transactional pressure from the conversation and lets them engage as an expert rather than an evaluator. Effective investor relationship management for founders means starting this process 6–12 months before you intend to open a round. Investors who've watched your trajectory over time move significantly faster when a round opens than those receiving a cold deck at the moment of fundraising.

How are investors paid back in a venture-backed startup?

Venture investors don't receive scheduled payments like a loan. They hold equity, which means returns are realized at a liquidity event — typically either an M&A transaction (the most common outcome for Seed and Series A companies) or an IPO. Secondary transactions at later stages can provide partial liquidity before a formal exit. Founders should also understand how liquidation preferences and participation rights affect payout order at exit, since these terms determine how proceeds are distributed across the cap table before common shareholders receive anything.

What are the warning signs that a founder-investor relationship is deteriorating?

The early signals are usually behavioral rather than explicit: delayed reply times, board check-ins that feel like audits, or an investor going silent during a missed metric instead of engaging constructively. More serious red flags include micromanagement (often a sign of lost confidence that hasn't been stated directly) and a lead investor backing a direct competitor. When friction surfaces, addressing it through a structured, documented conversation is almost always better than letting it compound. A toxic board dynamic is a known deal-killer in Series A due diligence, and it rarely resolves itself without a deliberate intervention.

Why do investors prioritize management team quality so heavily?

Because the team is the most durable asset at the early stage. Product roadmaps change, markets shift, and initial assumptions get invalidated — but a founder's judgment, communication style, and integrity under pressure persist across all of those pivots. Institutional investors consistently rank team quality as a critical factor ahead of the product itself, which means your credibility as an operator is being evaluated continuously, not just during a pitch. Every investor update you send, every difficult conversation you handle proactively, is part of that ongoing evaluation.