Mental Models for Founders to Master Fundraising Success

Key Takeaways

Only 0.7% of founders who pitch to venture capitalists secure funding — a statistic that signals pitch decks alone aren't enough. What separates funded founders is how they think, not just what they present.

Investors at the Seed and Series A stage are betting on trajectory, not current position. Being a "Slope" person (someone with a steep, compounding rate of growth) consistently outweighs having a strong starting point.

First Principles thinking means rebuilding your core assumptions from verifiable truths rather than industry benchmarks or category analogies. Investors pressure-test borrowed reasoning quickly; atomic clarity is what holds up under diligence.

Inversion: mapping every reason an investor would pass on your deal before they do transforms your biggest vulnerabilities into proof of intellectual honesty, one of the most valuable trust signals in early-stage fundraising.

The Circle of Competence applies to investor targeting as much as domain expertise. Pitching generalist investors on a specialized thesis wastes your scarcest resource: time. Prioritize partners whose sector knowledge, check-size history, and portfolio patterns genuinely overlap with your business.

Second-order thinking reveals the downstream consequences of every term you accept today. An aggressive seed valuation, a party round without a lead, or a fast close with minimal diligence each carries second-order effects that shape your Series A options before you've even started that raise.

Venture math is built around the Power Law. Investors aren't evaluating whether your business is good; they're evaluating whether it could be the outlier that returns the fund. Founders who understand this frame their pitch accordingly.

Fundraising is as much a psychological endurance test as a business exercise. Systematic detachment from rejection and separation of personal identity from company valuation are as important as any financial framework for sustaining performance across a 60-plus-meeting process.

The right investor network matters beyond the term sheet. Partners with genuine operator experience don't just provide capital; they steepen your growth slope through hiring referrals, customer introductions, and strategic guidance grounded in real execution experience.

The 0.7% Reality: Why Cognitive Frameworks Outperform Pitch Decks

Only 0.7% of founders who pitch to venture capitalists successfully secure funding — a number that makes the lottery look generous. That statistic, cited across Fundable and Harvard Business Review research, isn't just a caution sign. It's a signal that pitch decks alone don't separate funded founders from the rest.

What does separate them is how they think. Investors at the Seed and Series A stage aren't simply evaluating current revenue. They're evaluating trajectory — what Sam Altman describes as being a "Slope" person rather than a "Y-intercept" person. A high Y-intercept means a strong starting position today; a steep slope means a compounding rate of change over time. Investors consistently bet on slope, because slope predicts where a company will be, not just where it stands.

This is where mental models become the actual operating system of a successful raise. A mental model is a structured way of reasoning about complex, high-uncertainty situations — the kind of environment every early-stage fundraise creates. The approach, popularized through the work of Charlie Munger (often referenced as mental models by Munger), argues that smarter decision-making comes from building a latticework of frameworks rather than relying on intuition alone.

For founders navigating investor conversations, the practical implication is clear: before refining your deck, you need to rebuild how you reason about your business. That's exactly where first principles thinking begins.

First Principles: Stripping Your Business to Its Atomic Truths

First Principles thinking is one of the mental models found repeatedly useful precisely because it dismantles the comfortable shortcuts that get founders rejected.

As The Rainmaker Group highlights, First Principles thinking involves stripping business challenges to their core to avoid the bias of industry norms. For founders navigating due diligence, that bias is often lethal.

The Analogy vs. The Atom

The analogy trap often sounds like: "We're the Uber for X" or "Think Salesforce, but for Y." Analogies are cognitive shortcuts — useful for cocktail conversations, dangerous in a term sheet discussion. When a syndicate lead stress-tests your valuation, they're not looking for a familiar shape. They're looking for evidence that you understand why your business works at the unit level.

The atomic approach starts from verifiable truths: your actual cost to acquire a customer, the real retention curve driving lifetime value, and the structural reason a competitor can't replicate your distribution. Each assumption must be defensible on its own, not borrowed from a category narrative.

Applying this to unit economics means rebuilding your LTV:CAC ratio from first principles rather than benchmarking against industry averages. For instance, if your churn assumptions are anchored to what SaaS "typically" looks like, you're reasoning by analogy, and a sharp investor will surface that gap immediately. Understanding how hidden cost structures affect your valuation is part of the same discipline.

This kind of atomic clarity also reveals non-obvious market opportunities: the opportunities competitors missed because they were anchored to existing category assumptions. That's exactly the thinking that inversion builds on, which we'll explore next.

Inversion: Thinking Backwards to De-Risk the Deal

Inversion is one of the most underused mental models first principles thinkers reach for, and it's the one that can quietly make or break your fundraising round. Charlie Munger framed it simply: "Tell me where I'm going to die so I don't go there." For founders, that means running the pitch process in reverse before a single slide is opened.

The idea is to identify every reason a syndicate lead would pass on your deal and address those reasons first.

Here's a practical inversion checklist to work through before you approach investors:

Cap table red flags. Are there early investors with terms that complicate downstream rounds? Messy cap tables are a top-three deal-killer. Walk in knowing this, or walk out empty-handed.

Business model fragility. Where does your revenue model break under stress? Single-customer concentration, thin margins, and unproven retention are signals investors are trained to find.

Founder-market fit gaps. Can you credibly defend why you are the right team for this specific problem? Weak answers here stall more deals than weak financials.

The psychology underneath this approach matters. When founders surface their own risks proactively, syndicate leads experience a trust signal that's almost impossible to manufacture otherwise. It signals intellectual honesty (the trait that operator-led networks value most in early-stage software founders). As you build toward milestone-based commitments, that trust becomes the foundation every subsequent conversation rests on.

Knowing what you're walking into is powerful. Knowing who you're walking into it with is equally critical — which is exactly where your circle of competence comes in.

The Circle of Competence: Targeting the Right Syndicate

Pitching the wrong investor isn't just discouraging, it's a structural waste of one of your scarcest resources: time. Among the most practical mental models for startup founders, the Circle of Competence cuts through the noise immediately. According to DocSend's Founder Network, founders spend an average of 12.5 weeks closing a seed round across roughly 40 to 60 investor meetings. When a meaningful slice of those meetings lands with generalist VCs whose mandate stops well short of deep-tech SaaS, those weeks evaporate without moving your round forward.

The model, popularized by Charlie Munger and Warren Buffett, draws a clean boundary between what you genuinely understand and what you only think you understand. Applied to fundraising, it works in both directions. You need to know your own domain deeply enough to defend every assumption under pressure. But you also need to map each investor's circle (i.e., their sector knowledge, check size history, and portfolio pattern) before you book the meeting.

Align with operator-led syndicates whose circle overlaps yours. When your cap table includes investors who've actually built or scaled software businesses in your category, you gain more than capital. You gain pattern recognition that compounds. For example, Allied Venture Partners' operator network is structured precisely around this idea of connecting founders with domain-aligned backers who can stress-test a roadmap, not just a pitch deck.

Knowing where the boundaries of your competence sit also shapes how you answer hard questions. Founders who build towards an intentional cap table of complementary partners tend to attract investors who already understand the space, which shortens the education cycle and tightens the close. That kind of targeting discipline sets the foundation for the next decision layer: considering the downstream consequences of every term you accept.

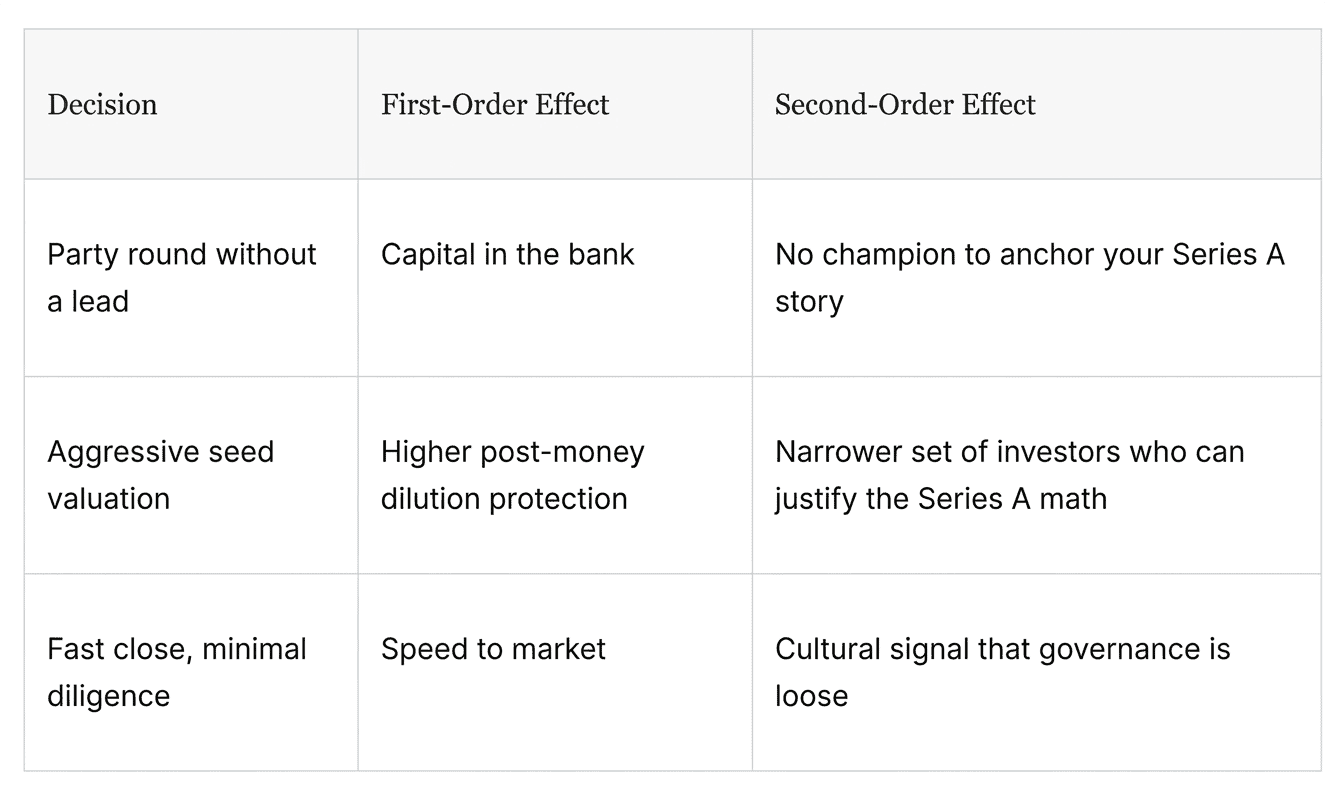

Second-Order Thinking: Beyond the Initial Check

Most fundraising mental models focus on closing the current round, but second-order thinking asks what that round sets in motion. The decisions you make today don't just fund your runway; they shape the terms, leverage, and optionality you carry into every conversation that follows.

As Jayme Hoffman notes on Medium, second-order thinking involves anticipating future consequences of current decisions, including how early dilution affects later-stage control. A seed valuation that feels like a win can quietly become a trap: if your Series A multiple doesn't clear the implied hurdle rate, institutional investors will pass regardless of your traction.

Capital also changes your company in ways that aren't on any term sheet. Headcount grows, decision cycles slow, and the scrappy culture that made your early product sharp can erode faster than your burn rate. Understanding how new capital affects team dynamics is as important as negotiating the valuation itself. The check is a catalyst, and catalysts don't just accelerate growth; they accelerate everything. That compounding effect is exactly why investors think in terms of power law returns, which we'll unpack next.

The Power Law: Understanding the Investor's Perspective

Venture capital math is brutally simple: a small number of investments must return the entire fund, which means every check a VC writes is a bet on an outlier. As Peter van Sabben notes, the Power Law dictates that the majority of returns come from a tiny fraction of portfolio companies, and that single insight explains nearly every investor behavior that founders find confusing.

The practical implication: VCs aren't evaluating whether your business is good. They're evaluating whether it could be the one that returns 100x.

This creates a meaningful distinction between a good business and a venture-scale business. A profitable, steady-growth SaaS company generating $3M ARR can be an excellent business, yet still be the wrong fit for a syndicate portfolio. If the realistic upside caps out below what a VC needs to justify the portfolio math, the answer will be no, regardless of your traction. Understanding how follow-on capital compounds these dynamics helps founders grasp why investors often reserve as much capital as they deploy initially.

The "outlier narrative" is therefore not hype; it's a structural requirement. When you pitch, you're not just describing what your company is today; you're constructing a credible path to a market outcome large enough to anchor a fund's returns. Frame the addressable market, the defensibility of your position, and the compounding nature of your growth in terms that let an investor genuinely model the 100x scenario. If that scenario isn't visible in your pitch, the math never works in your favor, no matter how solid your product is.

Of course, building a compelling outlier narrative requires more than strong slides. It also demands the psychological resilience to keep telling that story across dozens of meetings, which is exactly where many founders quietly struggle.

The Shrink's Perspective: Managing Founder Psychology

Fundraising is as much a psychological endurance test as it is a business exercise, and the founders who navigate it best treat their mental models as seriously as their financial ones.

Mental models from a psychological perspective help founders manage the emotional volatility that comes with scaling and raising capital. One of the most common traps is tying personal identity to company valuation. When a term sheet comes in below expectations, it can feel like a verdict on your worth as a founder. It isn't. Your company's current valuation is a data point, not a definition of you.

“Rejection isn't a judgment of your potential — it's a signal about fit, timing, and investor thesis alignment.”

Running 60+ investor meetings (a normal volume for a competitive Seed round) creates compounding rejection fatigue. The antidote isn't thicker skin; it's systematic detachment. Treat each "no" as product feedback, not personal failure.

“The investor who passes today may lead your Series A. How you handle rejection shapes the relationship more than the pitch deck does.”

The Map is Not the Territory model is equally critical when reality forces a pivot. Your business plan is a map — a useful approximation, not the terrain itself. When the market gives you new information, updating the map isn't a weakness; it's intellectual honesty.

“Founders who confuse their plan with reality resist pivots. Founders who hold the map lightly adapt faster.”

Understanding these psychological frameworks connects directly to the tactical mental models that make your pitch sharper. Which brings us to the four you need to master before your next investor meeting.

The Bottom Line: 4 Mental Models to Master Before Your Next Pitch

Fundraising success rarely comes down to a single pitch; it comes down to how clearly you think before you walk into the room. The four mental models covered in this article aren't abstract philosophy; they're practical frameworks that shape how investors read your conviction, your preparation, and your trajectory.

First Principles: Strip your business to its core truths. Investors push back hardest on assumptions you've borrowed from competitors. When you can defend your vision from the ground up (not by analogy), you signal the kind of independent thinking that survives market pivots.

Inversion: Before an investor asks why your startup might fail, you should have already answered it. Mapping your key risks, challenges, and failure modes (and building around them) transforms objections from threats into proof of rigor.

Circle of Competence: Pitching the wrong investor wastes everyone's time. Target those with genuine operator DNA in your market, i.e., people who understand your problem viscerally, not just financially. A curated deal flow network built around sector expertise matters for exactly this reason.

The Slope: As Sam Altman puts it, "The best way to build a large company is to be a 'Slope' person." Your rate of learning and traction tells investors more than your current metrics ever could. Show momentum, not just a snapshot.

Master these four models, and you're not just pitching a business, you're demonstrating the thinking process investors fund. The question isn't whether you know these frameworks. It's whether you're using them. The right network can help you apply them where it counts most.

Leveraging the Network: Why the Right Partner Matters

The mental models you carry into a fundraising process only create value when the partner across the table is equipped to recognize them. Fundraising isn't a transactional event; it's the beginning of a multi-year working relationship. The investor network you choose shapes not just your cap table, but the quality of guidance, operator connections, and follow-on support you can access at every inflection point.

This is where the slope versus y-intercept framework becomes directly actionable. A high y-intercept (i.e., strong initial metrics) gets you in the room. But the partners who accelerate your slope (i.e., your rate of compounding growth) are the ones with genuine operator experience and diverse networks to contribute after the term sheet is signed.

A no-cost pitching process removes the friction that often filters out high-potential founders before investors ever evaluate the actual business. Allied Venture Partners offers founders exactly that: access to one of Canada’s largest angel investor networks without upfront costs, connecting Seed and Series A software founders directly to a diverse network of operators across North America.

In practice, that operator access translates into faster hiring referrals, credible customer introductions, and strategic guidance grounded in real execution experience — all of which steepen your growth trajectory in measurable ways.

If the mental models in this article clarified how you think about traction, trajectory, and investor signals, the next step is straightforward. Submit your pitch through Allied Venture Partners' accessible 'Pitch Us' portal and put that thinking in front of investors who evaluate early-stage software companies with the same analytical rigor this article describes.

Key Mental Models Munger Takeaways

Cap table red flags. Are there early investors with terms that complicate downstream rounds? Messy cap tables are a top-three deal-killer. Walk in knowing this, or walk out empty-handed.

Business model fragility. Where does your revenue model break under stress? Single-customer concentration, thin margins, and unproven retention are signals investors are trained to find.

Founder-market fit gaps. Can you credibly defend why you are the right team for this specific problem? Weak answers here stall more deals than weak financials.

Only 0.7% of founders who pitch to venture capitalists successfully secure funding

Each assumption must be defensible on its own, not borrowed from a category narrative.

Inversion helps founders think about why a deal will fail, allowing them to proactively address gaps before approaching a syndicate.

Frequently Asked Questions

What are the most important mental models for startup founders navigating a fundraise?

The four fundraising mental models covered in this article are First Principles, Inversion, Circle of Competence, and the Slope vs. Y-Intercept framework. Each one addresses a different layer of the fundraising process — from how you reason about your unit economics, to how you target the right investors, to how you demonstrate trajectory rather than just current traction. Founders who internalize these frameworks don't just pitch better; they think differently in the room, which is ultimately what investors are evaluating.

What does "slope vs. y-intercept" mean in the context of venture fundraising?

The slope vs. y-intercept distinction, popularized by Sam Altman, describes two types of founders: those with a strong starting position today (high y-intercept) and those with a steep, compounding rate of growth over time (high slope). Venture investors consistently bet on slope, because it predicts where a company will be — not just where it stands at the moment of the pitch. Strong current metrics get you in the room, but demonstrable momentum is what closes the deal.

Why is First Principles thinking one of the mental models I find repeatedly useful as a founder?

Because most founders reason by analogy without realizing it. Framing your business as "the Uber for X" or benchmarking your churn assumptions against generic SaaS averages are both forms of borrowed reasoning — and experienced investors will surface those gaps quickly. First Principles thinking forces you to rebuild every core assumption from verifiable truths: your actual CAC, your real retention curve, your structural defensibility. That kind of atomic clarity is what separates a fundable pitch from a familiar-sounding one.

How does inversion help during the fundraising process?

Inversion asks you to map every reason an investor would pass on your deal — before they do. That means auditing your cap table for downstream complications, identifying where your revenue model breaks under stress, and honestly assessing whether you can defend your founder-market fit. When founders surface these risks proactively, it creates a trust signal that's difficult to manufacture any other way. Syndicate leads interpret that intellectual honesty as a green flag, not a red one.

What is the Circle of Competence, and how should founders apply it to investor targeting?

The Circle of Competence, developed by Charlie Munger and Warren Buffett, draws a boundary between what you genuinely understand and what you only think you understand. Applied to fundraising, it works in two directions: you need deep domain knowledge to defend your assumptions under diligence, and you need to map each investor's circle — their sector focus, check size history, and portfolio pattern — before booking a meeting. Pitching a generalist VC on a deep-tech SaaS thesis isn't just inefficient; it actively consumes the time and relationship capital you need to close the right partner.

What is second-order thinking, and why does it matter for early-stage founders?

Second-order thinking means looking past the immediate outcome of a decision to understand what it sets in motion. In fundraising, that means recognizing that an aggressive seed valuation might feel like a win today while quietly narrowing the field of investors who can justify your Series A math tomorrow. A fast close with minimal diligence signals loose governance culture to future institutional investors. Every term you accept today shapes the leverage and optionality you carry into every conversation that follows.

How does understanding the Power Law change how founders should pitch?

Venture funds are structured around the expectation that a small number of investments will return the entire fund. That means investors aren't evaluating whether your business is good — they're evaluating whether it could be the outlier that returns 100x. A profitable, steadily growing company can still be the wrong fit for a syndicate portfolio if the realistic upside doesn't clear the fund math. Founders who understand this frame their addressable market, defensibility, and growth compounding in terms that let an investor genuinely model that outlier scenario.

How should founders manage the psychological toll of a fundraising process?

Running 60 or more investor meetings — a normal volume for a competitive Seed round — creates compounding rejection fatigue. The most effective antidote isn't resilience for its own sake; it's systematic detachment. Treat each no as signal about fit, timing, or thesis alignment rather than a verdict on your potential. Separating personal identity from company valuation is equally critical: a term sheet below expectations is a data point, not a definition of you. The investor who passes today may well lead your Series A, and how you handle the rejection shapes that future relationship more than the pitch deck ever will.