AI Fundraising: How to Stand Out When 80% of VC Dollars Go to AI-Native Startups

AI funding has never been more abundant, or more unevenly distributed. In Q1 2026 alone, AI startups captured an astonishing 80% of all global venture funding, totaling over $242 billion, according to PitchBook. Those numbers feel like a green light for every founder with an AI pitch deck. But the reality is far more complicated.

Callout: Record-breaking total funding means very little if the vast majority flows to a handful of players.

The mega-deal phenomenon is reshaping the entire landscape. The top 4 companies in the AI sector now capture 63% of all venture investment. That concentration leaves the remaining 37% split across thousands of startups competing for what amounts to the scraps of an otherwise historic market.

Reality Check

Total AI VC deployed (Q1 2026): $242B+

Share reaching top 4 firms: ~63%

Capital left for everyone else: Less than half — divided among thousands of companies

For founders approaching Series A fundraising, this creates a paradox: the market has never looked more promising on paper, yet standing out has never been harder. Investors aren't short on deal flow; they're drowning in it. Strong AI capabilities once opened doors; today, they're simply the price of admission.

What actually separates funded from unfunded in this environment? The answer starts with understanding where most founders stumble before they ever reach a term sheet, and it begins even earlier than you might expect.

Is Pre-Seed Still Realistic for First-Time Founders?

Pre-seed fundraising hasn't disappeared, but the terms of entry have fundamentally changed. The question isn't whether early-stage capital exists; it's whether first-time founders can access it without proof that their core thesis already works.

The data tells a stark story. According to Carta, AI-native seed startups now command a 42% valuation premium over non-AI peers. In practice, that translates to a meaningful gap at the median:

AI seed startups: $17.9M median pre-money valuation

Non-AI seed startups: $12.6M median pre-money valuation

Premium gap: $5.3M, before a single dollar of revenue is earned

Premium valuations cut both ways. Higher entry points attract more capital, but they also raise investor expectations around traction, team pedigree, and defensibility before the round even closes.

What's shifted most is investor philosophy. Discovery funding (i.e., capital deployed to test whether an idea has merit) has largely dried up in favor of validation funding, where investors expect founders to arrive with early signals already in place. As Rajul Kadakia of Ayana put it, "Capital should scale what's already working, not be used to discover whether it works."

Understanding how milestones shape funding decisions has never been more critical for founders approaching their first institutional check. And increasingly, what investors are validating isn't just the model, it's the underlying asset the model depends on.

The Death of Model Sophistication as a Differentiator

Building a better model is no longer a fundable thesis. Investors now bet on who controls the data that makes any model valuable.

Foundational models have become a commodity. As capable base models grow increasingly accessible, the technical gap between startups has narrowed to near zero. Any well-resourced team can fine-tune a capable LLM in weeks. What they can't replicate overnight is a proprietary dataset built over years of real-world interactions, industry partnerships, or exclusive integrations.

This shift has fundamentally changed how investors evaluate AI companies, including where seed funding for startups gets allocated. According to Dealmaker and Harvard Business Review, proprietary data moats have replaced model sophistication as the primary competitive advantage in venture evaluations.

"The question investors are really asking is: who owns the data the model needs to be useful — and can anyone else get it?"

Data moat refers to a durable, defensible asset: labeled datasets, behavioral logs, proprietary integrations, or exclusive domain access that competitors simply cannot purchase or reproduce. A startup processing claims for a major insurer accumulates structured feedback loops that no open-source alternative can match.

The narrative shift is decisive. "We built a better LLM" no longer moves the needle in a pitch room. "We own the data pipeline no competitor can access" does. When you structure your pitch deck around this framing, defensibility becomes your lead story, which naturally sets the stage for demonstrating the operational efficiency that backs it up.

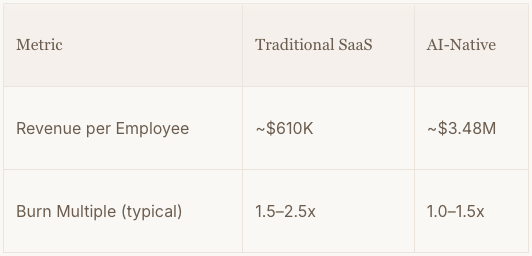

The New Efficiency Benchmark: 5x Revenue Per Employee

AI-native startups have redefined what "lean" means, and investors are now using efficiency ratios, not just growth rates, to separate fundable teams from the rest.

The benchmark is stark: according to Thunderbit, AI-native startups average $1.48 million in revenue per employee, compared to roughly $310,000 for traditional SaaS companies. That's a 5x gap that signals something structural, not incidental.

Why this matters to investors: Founders who know how to find investors for startup capital at the Series A level will increasingly encounter partners who open due diligence with an efficiency audit rather than a product demo. The question they're asking is: Does this team use AI internally the same way they're selling it externally?

What investors typically look for in AI-native efficiency:

Small headcount relative to ARR: teams of 10–20 generating $5M+ in revenue raise flags in the right direction

Automation-first operations: support, onboarding, and QA running on internal tooling

Low burn multiples: spending less per dollar of new ARR than comparable SaaS peers

When structuring your pitch, understanding how advisors frame these metrics for institutional audiences can sharpen how your efficiency story lands, especially as you approach the more demanding proof thresholds of a Series A round.

Transitioning from Seed to Institutional Series A

The leap from Seed to Series A is where most AI startups stall, because investors stop funding potential and start funding proof.

Understanding how to get startup funding at the institutional level means recognizing that the rules change completely between rounds. What worked at seed (e.g., a compelling narrative, a sharp team, early signals) won't close a Series A. The evolution follows a clear three-stage logic:

Team (Seed focus): Investors bet on the founders' ability to figure it out. Domain expertise and execution credibility carry disproportionate weight.

Traction (Bridge to Series A): Repeatable revenue, retention curves, and pipeline quality replace promises. Metrics must tell a story without the founder in the room.

Tech defensibility (Series A threshold): Institutional investors want to see why the model, data moat, or workflow integration can't be replicated cheaply by a better-funded competitor.

Series A rounds focus on scaling a proven business model, not finishing the product. Institutional investors typically acquire 15–25% equity in exchange for capital designed to extend runway for 18–24 months of aggressive growth. According to Carta, the structural expectations at this stage are materially different from early checks.

Review your legal readiness before the round – institutional due diligence moves fast and rewards founders who are prepared.

Knowing what investors expect is only half the equation. The other half is finding the right investors to have that conversation with, and that requires a different kind of strategy entirely.

How to Find and Vet the Right AI Investors

Not all capital is equal, and in today's overheated market, choosing the wrong investor can be as damaging as choosing no investor at all. Startup fundraising success increasingly depends on identifying partners who understand AI infrastructure, not just AI headlines. As Matt Murphy of Menlo Ventures noted via Crunchbase, "the craziness of certain AI have and have-nots are pushing valuations to 2021 levels" - a warning sign that hype-chasers are flooding the space.

The distinction matters: Infrastructure-literate investors ask about fine-tuning costs, inference latency, and data moats. Hype-chasers ask what LLM you're using and whether you've "talked to OpenAI."

Investor relationships are also a year-round responsibility, not a three-week sprint before you need a check. Founders who track the right growth signals continuously have warmer pipelines when it's time to raise because investors have already watched the story develop.

Checklist for Vetting VCs:

Portfolio fit: Do they have existing AI infrastructure investments, or only application-layer bets?

Operational value: Can they provide go-to-market intros, recruiting support, or technical advisory?

Stage consistency: Have they led rounds at your stage before, or are they experimenting?

Conviction signals: Do they ask hard questions, or just enthusiastic ones?

Venture partners who bring structured support beyond the check can meaningfully compress the time between funding and traction. That kind of visibility, both to investors and to the market, becomes its own fundraising asset.

Promoting Your AI Startup: Visibility as Fundraising Fuel

Visibility isn't vanity, it's a fundraising strategy that converts passive VC interest into inbound deal flow before you ever send a startup pitch deck.

As Startup Grind notes, visibility fuels fundraising by signaling market leadership and reducing the "discovery" friction investors face when evaluating dozens of similar tools. If a VC already knows your name before your cold email arrives, your raise is halfway done.

Three promotional formats consistently move the needle for AI founders:

The Whitepaper. Publishing rigorous, data-backed research on a narrow technical problem positions you as the category expert, not just another vendor. It attracts investors who are specifically hunting for depth. Keep it focused; own one problem completely rather than gesturing at ten.

The Demo. A sharp, public-facing product demo, whether a live tool, a recorded walkthrough, or a compelling video format, shows rather than tells. In practice, demos that highlight a specific, painful workflow generate far more qualified inbound than broad capability showcases.

The Keynote. Speaking at industry conferences, podcasts, or niche community events signals that the market endorses your perspective. It's social proof at scale.

The throughline across all three: own your niche clearly and loudly. Ambiguity kills momentum. When investors can articulate what you do in one sentence (because you've made it unavoidable), the conversation shifts from discovery to conviction. That's the foundation on which the next section's key takeaways are built.

The Bottom Line: Key Takeaways for the AI Era

To raise funding in the AI era, founders must internalize four hard truths: the rules have changed, and yesterday's pitch logic no longer applies.

Efficiency is the new growth metric. Investors are no longer impressed by headcount. They want revenue per employee, and the new benchmark is $3M or higher. A lean team generating real output signals far more to a discerning VC than a bloated org chart with a flashy demo.

Data is your only defensible moat. Foundational models are increasingly commoditized, meaning your technology stack alone won't protect your position. Proprietary datasets, unique feedback loops, and first-party behavioral data are what actually compound in value over time. Own that, and you own something worth funding.

Capital is concentrating fast. The market is bifurcating into clear winners and everyone else. If your traction metrics don't place you in the top 10% of your niche, you're effectively competing for scraps. The middle ground is evaporating.

Validation, not discovery, earns the check. Investors today are not in the business of helping you find a market. Lead with proof that a market already responds to your solution, then ask for capital to dominate it, not explore it.

These takeaways aren't just tactical reminders; they reflect a structural shift in how AI ventures are evaluated, and understanding that shift is the first step toward building a company worth backing for the long term.

Beyond the Hype: Partnering for Long-Term Scale

The era of winning on AI narrative alone is over. 2026 rewards founders who pair ambitious technology with disciplined, defensible unit economics.

The shift from 2021-style fundraising to today's environment is stark. Hype secured checks; efficiency now secures them. Investors who once funded compelling demos are scrutinizing gross margins, GPU cost trajectories, and retention curves with the same rigor they once reserved for late-stage deals. That compression isn't a temporary correction; it's the new baseline every AI founder must plan around.

Founders who internalize the "New Economics" early hold a structural advantage. They enter pitch meetings with the right benchmarks already mapped, the right questions already answered, and the right story (i.e., one built on evidence rather than possibility). Before your next pitch, audit your metrics honestly: Does your gross margin hold up at scale? Is your net revenue retention above the threshold that signals genuine product-market fit? Can you articulate what makes your model defensible beyond today's API dependency?

Allied Venture Partners works alongside founders who are building with that level of clarity - not chasing rounds, but engineering sustainable growth.

Your next step is concrete:stress-test your narrative against the hardest investor questions before you're in the room, and sharpen your opening minutes so every second earns its place. The math has changed. Make sure your pitch reflects it.

Frequently Asked Questions

What does it mean that AI startups captured 80% of global VC funding in Q1 2026?

It means the overall funding environment for AI has never been larger — but size doesn't equal access. The top four AI companies alone absorbed roughly 63% of that capital. For most founders, the practical funding pool is far smaller than the headline number suggests, and competition for the remaining share is intense.

Is pre-seed funding still accessible for first-time AI founders?

Yes, but the bar has risen considerably. Investors have largely moved away from "discovery" funding — backing ideas to test whether they work — in favor of "validation" funding, where founders arrive with early proof already in hand. Higher median valuations for AI seed startups (around $17.9M pre-money, per Carta) also raise expectations around traction and team credentials before a round even closes.

Why isn't building a better AI model enough to raise funding anymore?

Because capable base models are now widely accessible and relatively inexpensive to fine-tune. The technical differentiation between AI startups has narrowed significantly. What investors are evaluating instead is whether a company controls proprietary data — labeled datasets, behavioral logs, exclusive integrations — that no competitor can easily replicate. Model sophistication is table stakes; data ownership is the actual moat.

What is a "data moat" and why do investors care about it?

A data moat is a durable, defensible data asset that accumulates value over time and cannot be easily purchased or reproduced by a competitor. Examples include structured feedback loops from industry partnerships, first-party behavioral data generated through real-world product usage, or exclusive domain integrations. Investors care because it's the primary answer to the question: why can't a better-funded competitor simply build what you've built?

What efficiency benchmarks are investors using to evaluate AI-native startups?

The key metric is revenue per employee. AI-native startups are averaging around $1.48M–$3.48M in revenue per employee, compared to roughly $310K–$610K for traditional SaaS companies. Investors increasingly open due diligence with an efficiency audit rather than a product demo, looking for small headcounts relative to ARR, automation-first operations, and low burn multiples.

What's the difference between what gets a seed round versus a Series A?

Seed investors are primarily betting on the founding team's ability to execute and figure things out. Series A investors want evidence that the problem has been solved. That means repeatable revenue, strong retention curves, and a clear answer to why the business model can't be cheaply replicated. The shift is from funding potential to funding proof — and it's where many AI startups stall.

How should founders approach finding the right investors?

Not all capital is equal. Investors who understand AI infrastructure will probe fine-tuning costs, inference economics, and data defensibility. Hype-driven investors will ask surface-level questions about which LLM you're using. Founders should vet VCs the same way VCs vet founders: by checking portfolio fit, stage consistency, and whether the partner can add operational value beyond the check. Building those relationships year-round — rather than during a three-week fundraising sprint — produces meaningfully warmer pipelines.

How does visibility factor into fundraising success?

Investor inbound is substantially easier when VCs already know who you are before a cold email arrives. Publishing rigorous technical whitepapers, sharing sharp product demos, and speaking at industry events all signal market authority and reduce the friction investors face when evaluating similar companies. The goal is to make your positioning so clear and consistent that a VC can articulate what you do in a single sentence before your first meeting.

What are the most important things an AI founder should validate before pitching?

Four things: your revenue per employee relative to the AI-native benchmark; whether your data assets are genuinely proprietary and defensible; whether your traction metrics place you in the top tier of your niche; and whether you can demonstrate that a market already responds to your product, rather than asking investors to fund the search for one. The pitch should lead with evidence, not possibility.