Essential Legal Checklist for Your Series A Funding Round

Key Takeaways

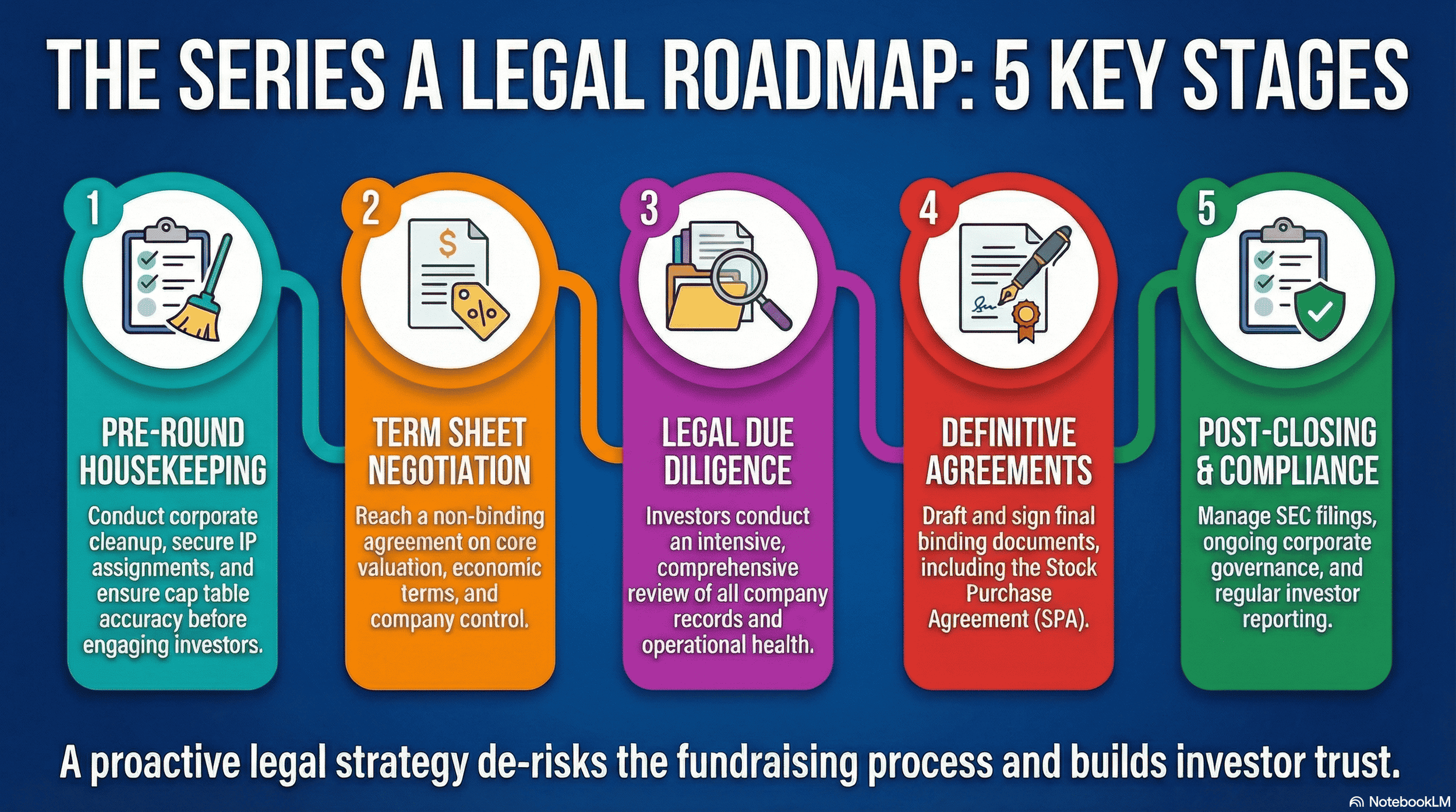

Series A funding requires extensive legal preparation across five critical stages: pre-round housekeeping, term sheet negotiation, legal due diligence, definitive agreements, and post-closing compliance—each demanding meticulous attention to protect founder interests and ensure smooth transactions.

Corporate governance and IP protection are foundational: Startups must maintain accurate cap tables, complete board meeting minutes, proper shareholder agreements, and comprehensive IP assignments from all founders, employees, and contractors before engaging with investors.

The Term Sheet is your first major legal negotiation: Understanding key provisions like liquidation preferences, board composition, protective provisions, and founder vesting is crucial—these terms profoundly impact future returns and control, making experienced legal counsel essential.

Due diligence demands comprehensive documentation: Investors will scrutinize your entire legal foundation through a virtual data room containing corporate records, IP documentation, material contracts, employment agreements, regulatory compliance proof, and financial statements—incomplete documentation is a major red flag.

Proactive legal readiness significantly de-risks fundraising: With median Series A valuations reaching $49.3 million and 26-month gaps between seed and Series A rounds, maintaining continuous legal compliance, organized documentation, and robust governance demonstrates operational maturity and accelerates the funding process.

Post-closing legal obligations are ongoing and critical: After securing Series A funding, startups must maintain rigorous corporate governance through regular board meetings, continuous cap table management, evolving IP protection, regulatory compliance monitoring, and systematic preparation for future funding rounds like Series B.

Navigating Series A with Legal Confidence

Securing Series A funding is a pivotal moment for any startup. It signifies validation, unlocks significant growth potential, and elevates the company's trajectory. However, this critical funding round also introduces a new level of scrutiny and complexity, particularly on the legal front. Investors, especially institutional ones, will meticulously examine your company's legal health, from its foundational structure to its operational compliance. A thorough understanding of the legal requirements and potential pitfalls is not just beneficial; it's essential for a smooth transaction, founder protection, and long-term success.

This guide provides an essential legal checklist, meticulously designed to help founders navigate the Series A funding round with confidence. We'll cover the foundational legal housekeeping necessary before engaging with investors, the critical terms within the Term Sheet, the rigorous process of legal due diligence, the definitive agreements that close the deal, and the ongoing legal compliance vital for sustained growth.

By proactively addressing these legal facets, you can significantly de-risk the fundraising process, build investor trust, and ensure your company is positioned for continued expansion and a strong future valuation.

The Stakes of Series A: Beyond the Investment Capital

The Series A funding round represents a significant inflection point for startups. It's more than just injecting capital; it's a strategic endorsement that propels a company from its nascent stages toward scalable growth. While the investment funds critical initiatives such as product development, market expansion, and team scaling, the associated legal due diligence and negotiation processes carry substantial weight.

At this stage, investors are looking for more than just a promising idea and early traction. They seek a well-structured, legally sound company capable of navigating complex regulatory landscapes, protecting its intellectual property, and adhering to robust corporate governance. The median pre-money Series A valuation reached $49.3 million in Q3 2025, the highest on record, according to Carta. This level of investment underscores the expectation of a mature and legally defensible business. The median time lapse between funding rounds from Seed to Series A was 26 months in 2025, the longest span since 2012, according to SaaStr. This extended timeline means startups must maintain legal preparedness for a longer duration.

Why a Proactive Legal Approach is Your Best Investment

Approaching Series A legal requirements proactively is not merely about avoiding problems; it's a strategic investment that yields tangible benefits. A clean legal foundation demonstrates a company's professionalism, operational rigor, and long-term vision to potential investors. It signals that the founders have built a robust entity, not just a product. This preparedness can significantly expedite the fundraising process, reduce the likelihood of costly delays or deal renegotiations, and build invaluable trust with investors. Furthermore, a strong legal posture directly influences the company's valuation, as it mitigates perceived risk.

The Goal: A Smooth Legal Transaction and Founder Protection

The ultimate objective of meticulously managing the legal aspects of your Series A funding round is twofold: to facilitate a smooth, efficient transaction that secures the necessary investment, and to ensure the founders' interests and vision are protected. This involves understanding and negotiating terms that align with the company's growth strategy while safeguarding against future conflicts or misaligned incentives. A well-structured legal framework protects the founders' equity, ensures clear decision-making processes, and establishes a solid foundation for future fundraising and exit opportunities.

The Series A funding process involves several distinct legal phases, from initial preparation and due diligence to the final closing agreements and ongoing compliance.

Section 1: Laying the Legal Foundation (Pre-Funding Housekeeping)

Before you even begin discussions with potential investors, a significant amount of foundational legal work should be completed. This pre-funding housekeeping is critical for demonstrating a mature, well-governed company and for streamlining the subsequent stages of the funding round. Ignoring these elements can lead to significant "red flags" during due diligence, potentially jeopardizing the investment or forcing unfavorable renegotiations.

Corporate Governance and Company Structure

The bedrock of any company lies in its corporate structure and governance. This includes ensuring your company is properly incorporated in the correct jurisdiction, with all necessary documentation in place. Key aspects to review and rectify include:

Formation Documents: Verify your Certificate of Incorporation (or equivalent) is accurate and filed correctly. Ensure your company bylaws are up-to-date and reflect current operational practices.

Board of Directors: Confirm the composition of your board is appropriate for a company seeking institutional investment. This often involves establishing independent board seats or preparing for investor-appointed directors. Document all board minutes and resolutions meticulously, as these are scrutinized during due diligence.

Shareholder Agreements: If you have existing shareholders beyond the founders, ensure a clear and comprehensive shareholder agreement is in place. This document governs rights, obligations, and decision-making processes among shareholders. Around 65% of startups fail due to founders' conflicts, underscoring the critical need for clear founder agreements and robust corporate governance structures from the outset to prevent legal disputes that can lead to company failure, as noted by Legal Nodes.

Cap Table Management: Maintain an accurate and up-to-date capitalization table (cap table). This document details all equity holders, their respective ownership percentages, and the terms of their holdings. A clean cap table is paramount for Series A investors who will use it to understand ownership structures and potential dilution.

Intellectual Property (IP) Protection

Your intellectual property—patents, trademarks, copyrights, and trade secrets—is often the core asset of your startup. Protecting it rigorously is non-negotiable for a Series A funding round.

IP Assignments: Ensure all IP created by founders, employees, contractors, and advisors has been formally assigned to the company. This is crucial; if IP vests with individuals, the company doesn't truly own its most valuable assets. Standard employment and contractor agreements should include robust IP assignment clauses.

Patent and Trademark Filings: Review the status of any patent or trademark applications. Investors will assess the strength and defensibility of your IP portfolio. Understand your strategy for protecting your product's unique features and brand identity.

Trade Secrets: Implement measures to protect your trade secrets, such as non-disclosure agreements (NDAs) and internal security protocols.

Employee, Contractor, and Advisor Documentation

The legal standing of your team, including employees, independent contractors, and advisors, is a significant area of focus for investors.

Employment Agreements: Ensure all employees have clear employment agreements outlining their roles, responsibilities, compensation, and any equity grants.

Independent Contractor Agreements: For any work performed by contractors, verify that proper independent contractor agreements are in place. These should clearly define the scope of work, payment terms, and critically, ensure that the contractor is not misclassified as an employee, which carries significant legal and financial liabilities.

Non-Disclosure Agreements (NDAs): All individuals who have access to sensitive company information, including early employees, advisors, and key partners, should have signed NDAs.

Equity Vesting: For founders and early employees, ensure stock vesting schedules are clearly documented and consistently applied. This aligns incentives and protects the company if key individuals depart unexpectedly.

Data Privacy and Regulatory Compliance

In today's regulatory environment, demonstrating a commitment to data privacy and compliance with relevant laws is essential, particularly if your company handles customer data or operates in a regulated industry.

Privacy Policies: Ensure your company has a clear, accessible, and compliant privacy policy on your website and within your product.

Data Handling Procedures: Understand how your company collects, stores, processes, and protects user data. Compliance with regulations like GDPR (General Data Protection Regulation) and CCPA (California Consumer Privacy Act) is often expected.

Industry-Specific Regulations: Depending on your industry (e.g., FinTech, HealthTech), identify and comply with all relevant regulatory requirements. The global compliance software market is projected to reach $80 billion by 2027, driven by regulatory expansion, according to The Tech Buzz, illustrating the growing importance of this area.

Review of Existing Material Contracts and Agreements

Investors will want to review significant contracts that impact your company's operations, revenue, and liabilities.

Customer Agreements: Ensure your standard customer agreements are well-drafted and protect the company's interests. Review significant customer contracts for key terms, obligations, and potential risks.

Vendor and Partner Agreements: Examine agreements with key suppliers, vendors, and strategic partners.

Lease Agreements: Review any real estate leases or significant asset agreements.

Licensing Agreements: If you license technology from or to third parties, ensure these agreements are in order.

Thoroughly organizing and reviewing these foundational legal documents before engaging with investors can significantly de-risk the process and demonstrate a well-managed company.

Section 2: Navigating the Term Sheet: Your First Legal Negotiation

The Term Sheet marks the initial formal offer from investors and outlines the principal terms of the proposed investment. While often non-binding in its entirety, it serves as the blueprint for the definitive agreements and represents the first significant legal negotiation in the Series A process. Understanding its components and implications is crucial.

Understanding the Term Sheet's Purpose and Legal Standing

A Term Sheet is a preliminary, non-binding agreement (with a few exceptions, typically confidentiality and exclusivity clauses) that details the core economic and control terms of an investment. Its purpose is to establish a mutual understanding between the startup and the investors, allowing both parties to assess the viability and desirability of the deal before incurring the significant costs associated with drafting definitive agreements. It lays the groundwork for the legally binding documents that will follow.

Key Economic and Control Provisions to Scrutinize

The Term Sheet is packed with clauses that profoundly impact the company's future and the founders' equity. Key provisions to scrutinize include:

Valuation and Investment Amount: This defines the company's pre-money valuation and the amount of capital to be raised, directly impacting ownership percentages.

Pro tip: For further reading on pre-money versus post-money valuation, see Pre-Money and Post-Money Valuation Formulas.

Liquidation Preferences: This dictates how investors are repaid in the event of a sale or liquidation. Common types include non-participating, participating, and uncapped participating preferred. Investors typically seek preferences that ensure they recoup their investment (and often a multiple of it) before common stockholders receive anything.

Pro tip: For further reading on liquidation preferences, see Founders Essential Guide: Negotiating Liquidation Preferences for Optimal Outcomes, Modelling Liquidation Preferences in Cap Tables, and Liquidation Preferences: Investor vs. Founder Interests.

Board Seats and Control: The Term Sheet will specify the composition of the board of directors, often granting investors one or more board seats. It will also outline protective provisions, which require investor consent for certain major corporate actions (e.g., selling the company, raising subsequent rounds, incurring significant debt).

Pro tip: For further reading on startup board seats, see Startup Governance: How Board Seat Allocation Shapes Your Company's Future.

Dividends: While less common at Series A, some Term Sheets may include provisions for dividends, which can accrue to preferred stockholders. Overtly investor-friendly terms like cumulative dividends declined from 8.2% to 3.3% in financing rounds since 2020, according to Mayer Brown, indicating a trend towards more balanced agreements.

Conversion Rights: Details on how preferred stock converts into common stock upon certain events, such as an IPO.

Drag-Along and Tag-Along Rights: These clauses govern the sale of the company. Drag-along rights allow majority shareholders (typically investors) to force minority shareholders to sell their shares in a sale, while tag-along rights allow minority shareholders to join a sale initiated by majority shareholders.

Pro tip: For further reading on drag-along and tag-along rights, see Ultimate Guide to Drag-Along and Tag-Along Rights.

Founder-Specific Clauses for Protection

Beyond the standard investor terms, it's crucial to ensure founder interests are adequately protected.

Founder Vesting: If founder shares are not already fully vested, the Term Sheet or subsequent agreements may require continued vesting, often tied to continued service. Ensure this is clearly defined and reasonable.

Founder Employment Agreements: Outline the terms of employment for founders, including salary, role, and severance packages, to provide stability and clarity.

Non-Competes: Be aware of any clauses that may restrict founders' future entrepreneurial activities. Negotiate these terms carefully.

The Critical Role of Legal Advice

Navigating the complexities of a Term Sheet without experienced legal counsel is highly inadvisable. Specialized startup lawyers understand market norms, can identify potentially unfavorable terms, and can negotiate on your behalf to achieve a balanced agreement. They ensure that the Term Sheet accurately reflects your understanding and protects your company's long-term interests.

Spotting Red Flags in Term Sheet Negotiations

Certain terms or negotiation tactics can serve as red flags indicating potential issues:

Unreasonable Valuation: A valuation that significantly deviates from market norms for your stage and industry can be a warning sign.

Excessively Investor-Friendly Economics: Terms like high liquidation multiples, broad participation rights, or automatic preferred stock resets can severely dilute founders' and employees' potential returns.

Overly Restrictive Control Provisions: Protective provisions that give investors veto power over nearly every significant business decision can stifle innovation and operational agility.

Unusual or Opaque Terms: If you or your counsel don't fully understand a term, it warrants further investigation and clarification.

Pressure Tactics: Investors who rush negotiations or refuse to allow for proper legal review may be attempting to push through unfavorable terms.

A well-negotiated Term Sheet sets a positive tone for the remainder of the funding process and establishes a fair partnership between the company and its new investors.

Section 3: Legal Due Diligence: Opening Your Books to Investors

Once a Term Sheet is agreed upon, the investors will commence their formal legal due diligence. This is an intensive review process where they meticulously examine every aspect of your company's legal and operational health to confirm the representations made during fundraising. Thorough preparation is key to a smooth and successful due diligence phase.

Preparing Your Data Room for Investor Scrutiny

A virtual data room (VDR) is a secure online repository where you will upload all requested documents. Investors’ legal teams will access this to conduct their review. The data room should be organized logically, making it easy for due diligence teams to find what they need.

Categorization: Organize documents into clear categories (e.g., Corporate Records, Intellectual Property, Contracts, Employment, Financials).

Completeness: Ensure all requested documents are provided accurately and in their entirety. Missing documents can be a significant red flag.

Accessibility: Provide appropriate access levels to the investor's team.

Professional Presentation: Documents should be clean, legible, and well-organized. Automated reporting can reduce the time to create financial reports from days to two hours, and cut data entry mistakes by 90%, significantly streamlining due diligence, according to Lucid.

The Comprehensive Legal Due Diligence Checklist (VC Due Diligence Checklist)

While specific requests vary by investor, a comprehensive legal due diligence checklist typically includes the following categories and documents:

Corporate Records:

Certificate of Incorporation/Formation and any amendments

Bylaws/Operating Agreement and any amendments

Minutes of Board of Directors and Shareholder meetings

Stock ledgers and cap table history

List of all current Shareholders and their contact information

Any shareholder agreements or voting agreements

Records of any past or pending litigation

Intellectual Property (IP):

List of all registered patents, trademarks, and copyrights, including application and registration numbers and dates

Copies of patent and trademark filings

Evidence of IP assignments from founders, employees, and contractors

Proprietary technology and trade secret documentation (subject to confidentiality)

Licenses granted to or by the company

Material Contracts:

Key customer agreements (e.g., SaaS agreements, master service agreements)

Key vendor and supplier agreements

Partnership and joint venture agreements

Loan and financing agreements

Lease agreements

Any other contract that is material to the company's business or financial condition

Employment and Compensation:

Standard form employment agreements

Independent contractor agreements

Consulting agreements

Employee handbook and policies

Stock option plans and grant agreements

Agreements with key executives and founders

Regulatory Compliance:

All necessary licenses and permits

Privacy policies and terms of service

Data security policies and certifications

Compliance documentation related to specific industry regulations (e.g., HIPAA, FINRA)

Financials:

Audited financial statements (if applicable)

Unaudited interim financial statements

Tax returns

Cap table showing all equity issuances and changes

Pro tip: For further reading on the VC due diligence process, see Due Diligence Process: What Founders Need to Know.

Addressing and Mitigating Potential Legal Red Flags

During due diligence, investors look for consistency, accuracy, and completeness. Potential red flags include:

Incomplete or Missing Documentation: This suggests a lack of diligence on the company's part.

Unclear IP Ownership: Gaps in IP assignment are a critical concern, as they undermine the company's core asset.

Misclassified Employees: Incorrectly classifying contractors as employees can lead to significant back taxes, penalties, and legal liabilities.

Breaches of Contract: Any significant breaches of material contracts can expose the company to lawsuits and financial damages.

Outstanding Litigation or Disputes: Existing legal battles can drain resources and create uncertainty.

Non-Compliance with Regulations: Failure to adhere to data privacy or industry-specific laws can result in fines and operational disruptions.

Proactively identifying and resolving these issues before due diligence begins can save significant time and prevent deal disruptions. For example, ensuring all IP assignments are finalized and employment agreements are correctly executed will preemptively address major concerns.

Legal Opinions: What Investors Expect

As part of the closing process, investors may request legal opinions from your company's counsel. These opinions are written statements from the lawyers confirming certain legal facts or conclusions about the company and the transaction. Common opinions include:

Enforceability Opinion: Confirming that the definitive agreements are legal, valid, and enforceable against the company.

Good Standing Opinion: Stating that the company is duly organized and in good standing in its jurisdiction of incorporation.

Authorization Opinion: Confirming that the company has the authority to enter into the transaction documents.

Your legal counsel will work with the investors' counsel to determine the scope and form of any required legal opinions.

Section 4: Definitive Agreements & Closing the Funding Round

The successful completion of due diligence transitions the Series A process from negotiation and examination to the execution of legally binding documents. This phase is where the Term Sheet's provisions are codified into formal agreements that finalize the investment.

Transitioning from Term Sheet to Binding Legal Contracts

The Term Sheet, having provided the framework, now guides the drafting of definitive agreements. These are complex legal documents that require careful review by both parties' legal counsel. Key agreements typically include:

Stock Purchase Agreement (SPA): This is the primary agreement detailing the terms under which investors will purchase shares. It includes representations and warranties made by the company and the investors, covenants (promises of future actions), and conditions precedent to closing.

Amended and Restated Certificate of Incorporation (or equivalent): This document incorporates the terms of the preferred stock being issued, including liquidation preferences, conversion rights, and voting rights, into the company's corporate charter.

Amended and Restated Bylaws: These bylaws are updated to reflect the new board structure and governance provisions.

Investors' Rights Agreement: This agreement outlines various rights granted to the investors, such as registration rights (for future public offerings), information rights, and rights of first refusal on future financings.

Voting Agreement: This agreement often details how directors will be elected and how certain major corporate decisions will be voted upon, reflecting the board composition agreed in the Term Sheet.

Right of First Refusal and Co-Sale Agreement: This governs the transfer of shares by existing shareholders, including founders, and is often amended or replaced by the new investor agreements.

These agreements collectively establish the legal framework for the company's relationship with its new investors.

Finalizing the Cap Table Management

With the investment closing, the company's capitalization structure will change. This is the critical point where the cap table must be updated accurately to reflect:

Issuance of New Preferred Shares: The shares purchased by the investors.

Potential Conversion of Existing Securities: If convertible notes or SAFEs were used in prior rounds, they will now convert into preferred stock as per their terms. In 2024, 62% of Series A financings included the conversion of convertible securities, indicating a higher incidence compared to prior years, according to Osler, Hoskin & Harcourt LLP.

Dilution of Existing Shareholders: The impact of the new issuance on the ownership percentages of founders, employees, and earlier investors.

An accurate and up-to-date cap table is essential for understanding ownership, managing future equity grants, and calculating potential returns during an exit.

Pro tip: To learn more about cap table impacts, see our guide How Cap Tables Change Across Funding Rounds.

The Legal Transaction Closing Mechanics

The closing is the formal event where all parties sign the definitive agreements, funds are transferred, and the investment is officially completed.

Signing Ceremony: All parties sign the executed copies of the definitive agreements.

Funding Wire: Investors wire the investment capital to the company's bank account.

Filing of Documents: Any necessary amendments to the company's corporate charter are filed with the state.

Issuance of Shares: The company formally issues the new shares to the investors.

Closing Certificates: Board and officer certificates are often exchanged, confirming the authority to act and the completion of necessary corporate actions.

This step culminates the Series A fundraising process, transforming the provisional agreement into a legally binding reality.

Section 5: Post-Closing Legal Essentials and Ongoing Compliance

The funding is secured, but the legal work is far from over. Establishing robust post-closing legal practices is crucial for a company's sustained growth, future fundraising success, and ongoing compliance. This phase focuses on maintaining the legal health and operational integrity demonstrated during the Series A round.

Maintaining Robust Corporate Governance

With new investors and potentially new board members, maintaining strong corporate governance is paramount.

Regular Board Meetings: Conduct board meetings in accordance with your bylaws and applicable laws, typically quarterly for Series A companies. Ensure clear agendas are set, and detailed minutes are recorded for all meetings and key decisions.

Shareholder Communications: Keep all shareholders informed about significant company developments, as stipulated in the Investors' Rights Agreement.

Compliance with Laws: Continuously monitor and comply with all federal, state, and local laws and regulations relevant to your business operations. This includes labor laws, industry-specific regulations, and tax obligations.

Continuous Cap Table Management

The cap table will continue to evolve. Ongoing management is essential to avoid future complications.

Tracking Equity Events: Accurately record all future equity issuances, such as employee stock option grants, exercises, and any new funding rounds.

Dilution Monitoring: Understand and communicate the impact of new issuances on existing shareholders.

Option Plan Administration: Properly administer your stock option plan, including vesting schedules and exercise procedures.

This ongoing vigilance ensures transparency and accuracy, which are vital for investor confidence and future financial planning.

Protecting Your Investment and Future Growth

Your legal foundation is not static; it must adapt as your company grows.

Ongoing IP Management: Continue to monitor and protect your intellectual property. File for new patents or trademarks as your product evolves, and take action against infringement.

Contract Renewals and Revisions: Proactively manage contract renewals and adapt existing agreements to reflect changes in your business model or market conditions.

Data Privacy and Security: Stay updated on evolving data privacy laws and ensure your practices remain compliant. Invest in robust cybersecurity measures to protect sensitive data.

Legal and Financial Health: Maintain a clean financial record and clear legal standing. This will be critical for subsequent funding rounds (Series B, C, etc.) and potential exit strategies.

What's Next? Preparing the Legal Foundation for Your Series A Funding Round

Successfully navigating your Series A funding round requires meticulous attention to legal details, from initial structural housekeeping to post-closing compliance. You've learned the critical legal foundations to lay, the nuances of term sheet negotiation, the demands of investor due diligence, the mechanics of closing, and the importance of ongoing legal stewardship.

By proactively addressing these legal aspects, you not only de-risk the fundraising process but also build a stronger, more attractive company, enhancing your valuation and investor confidence. A robust legal framework is a testament to your company’s maturity and its readiness for significant growth.

Your next steps should involve:

Engage Experienced Legal Counsel: If you haven't already, secure legal advisors specializing in venture capital financings. They are your most critical partners in this process.

Organize Your Data Room: Begin compiling and organizing all necessary legal and corporate documents as outlined in Section 3. This preparatory work will significantly accelerate due diligence.

Review and Understand Key Agreements: Familiarize yourself with standard Series A documents and terms, and be prepared to negotiate effectively with your legal team's guidance.

Prioritize Founder Protection: Ensure your own interests, and those of your founding team, are considered and protected throughout the negotiation and documentation phases.

Establish Post-Closing Processes: Implement systems for ongoing corporate governance, cap table management, and compliance to ensure your company remains legally sound as it scales.

By treating legal readiness as a strategic imperative, you will be well-equipped to close your Series A funding round smoothly and set your company on a path for sustained success.

Frequently Asked Questions (FAQ)

General Series A Preparation

What's the difference between raising funds at pre-seed/seed stages versus Series A?

Pre-seed/seed funding typically relies more on founder credibility and product potential, while Series A requires startups to demonstrate market validation, proven revenue growth rate, and sustainable unit economics. Series A investors, including venture capitalists, conduct far more rigorous legal diligence and expect startups to have comprehensive financial records, a well-organized data room, and clear evidence of market potential through validated KPIs and growth metrics.

How long should startups maintain legal preparedness between funding rounds?

The median time between Seed and Series A was 26 months in 2025—the longest since 2012. During this period, startups must continuously maintain their legal foundation, including up-to-date board meeting minutes, accurate cap table templates, organized financial records, and compliance with all regulatory requirements. This extended runway means sustained attention to legal diligence, not just last-minute preparation when raising funds.

What role does the management team play in Series A legal preparation?

The management team, particularly the founder CEO, bears ultimate responsibility for ensuring legal readiness. This includes overseeing corporate governance, maintaining the data room, ensuring all diligence checklists are complete, protecting confidential information, and working with law firms to address compliance issues before venture capitalists begin their evaluation. The management team must demonstrate operational maturity alongside product-market fit.

Corporate Structure & Governance

Why do investors prefer Delaware C-Corps for VC-backed startups?

Delaware C-Corps are the standard structure for VC-backed startups because they offer well-established corporate law frameworks, flexible ownership structures, and governance provisions that venture capitalists understand. The governing law in Delaware is particularly favorable for venture and seed funding transactions, making it easier to execute standard investment documents and protecting both startups and investors through clear dispute resolution mechanisms.

What's included in a comprehensive shareholders' agreement for Series A?

A shareholders' agreement (or articles of association) governs the ownership and share structure, defining rights, obligations, and decision-making processes. It should address board composition, investor approval requirements for major decisions, transfer restrictions, drag-along and tag-along rights, dispute resolution procedures, and protection of confidential information. This agreement becomes increasingly important as the ownership structure grows more complex post-Series A.

How detailed should board meeting minutes be for investor scrutiny?

Board meeting minutes must document all significant decisions, discussions, and votes comprehensively. Venture capitalists reviewing your data room will scrutinize these records to assess governance quality, decision-making processes, and whether the management team has exercised proper fiduciary responsibility. Missing or incomplete board meeting minutes are major red flags that can derail Series A negotiations and affect investor approval.

Financial Documentation & Metrics

What financial metrics do venture capitalists prioritize when evaluating startups?

Key VC evaluation criteria include revenue growth rate, burn rate, runway (months of cash remaining), customer acquisition cost, LTV/CAC ratio, gross margins, unit economics, and overall financial health. Investors expect startups to demonstrate scalability through improving KPIs, efficient sales cycles, sustainable business models, and a clear financial plan showing the path to profitability. GAAP financials are often required for larger Series A rounds.

How should startups organize their financial model for Series A investors?

Your financial model should project at least 3-5 years forward, showing realistic revenue assumptions, detailed expense breakdowns including burn rate, customer acquisition cost trends, and the impact on runway. Include sensitivity analysis for key growth metrics, demonstrate understanding of unit economics and gross margins, and show how the Series A capital will extend your runway while accelerating market opportunity capture. Use professional valuation software if analyzing complex scenarios.

What financial records must be included in the data room?

The data room should contain audited financial statements (if available), unaudited interim statements, tax returns, detailed revenue reports, accounts receivables aging, expense records, the complete cap table template history, and your comprehensive financial plan. Additionally, include documentation of all financial transactions, loan agreements, and records demonstrating financial health and the absence of financial crime exposure.

Market & Business Model

How do startups demonstrate market validation to Series A investors?

Market validation requires proof beyond the product itself. Startups should provide market research reports, customer videos and testimonials, documented user numbers and growth, competitive market analysis showing your unique selling proposition, evidence of product-market fit through strong NPS scores and viral coefficient, and clear demonstration of market size and market potential within your sector thesis.

What business model elements are most scrutinized during Series A?

Investors carefully examine whether your business model is scalable, the sustainability of unit economics, pricing strategy and its impact on gross margins, customer acquisition cost relative to lifetime value (LTV/CAC ratio), revenue diversity and concentration risk, sales cycle length and efficiency, and the clarity of your path to market leadership. The business model must support the valuation and demonstrate clear market opportunity exploitation.

How important is competitive market landscape analysis in your pitch deck?

The market landscape section of your pitch deck is critical—venture capitalists need to understand your competitive positioning, differentiation, and defensibility. Include thorough market analysis showing market size, market potential, market opportunity, your unique selling proposition, competitive advantages, and barriers to entry. Angel investors and VCs want confidence that you understand both the market and your place within it.

Legal Due Diligence & Documentation

What should startups include in their legal diligence data room checklist?

Comprehensive diligence checklists should include: all formation documents and articles of association, complete ownership structures documentation, intellectual property assignments with evidence of moral rights waivers, employment and contractor agreements, material customer and vendor contracts, regulatory compliance documentation, privacy policies, board meeting minutes, shareholders' agreements, power of attorney documents where applicable, and any litigation or dispute resolution records. Organize these logically for easy navigation.

How can startups identify and address compliance issues before Series A due diligence?

Conduct an internal audit using standard evaluation checklists months before raising funds. Work with experienced law firms to review regulatory compliance, data privacy adherence, employment classification accuracy, IP ownership documentation, and industry-specific requirements. Address any compliance issues proactively, document remediation efforts, and ensure all regulatory licenses and permits are current. Prevention of compliance issues protects against both deal failure and reputational damage.

What IP protection measures do venture capitalists expect from startups?

Investors expect comprehensive IP assignments from all founders, employees, contractors, and advisors, with explicit waivers of moral rights where applicable. Startups should have filed relevant patents and trademarks, implemented NDAs protecting confidential information, documented trade secrets with appropriate security protocols, and demonstrated ongoing IP management processes. IP protection is fundamental to the product's defensibility and the company's market potential.

Investor Relations & Negotiations

How should startups approach investor fit assessment beyond just securing capital?

A: Evaluate investor fit by researching their sector thesis alignment with your market, their track record with similar startups, the value-add beyond capital (e.g., network, expertise), their approach to governance and founder CEO autonomy, their typical involvement level and operational considerations, and their portfolio companies' experiences. The right investor fit can accelerate growth and facilitate future fundraising, including Series B rounds.

What resources can help startups prepare their Series A pitch deck and materials?

Leverage resources from accelerators like Y Combinator and Founder Institute, which provide pitch deck templates and VC fundraising guidance. Organize supporting materials in Google Drive or professional data room platforms. Include customer videos, market reports, detailed financial models, growth metrics dashboards, product demonstrations, and clear articulation of your unique selling proposition and market opportunity. Professional presentation reflects operational maturity.

What distinguishes angel investors' approach from venture capitalists' VC evaluation criteria?

Angel investors at earlier stages (pre-seed/seed) often rely more on founder relationships and product vision, while venture capitalists conducting Series A evaluation apply rigorous VC evaluation criteria focused on proven market validation, scalable business models, verifiable revenue and growth metrics, comprehensive financial health indicators, strong management teams, and clear paths to market leadership. VC-backed startups face higher bars for documentation, governance, and legal compliance than companies with only angel investors.

Post-Closing & Ongoing Management

What ongoing legal and governance obligations follow Series A closing?

Post-closing, startups must conduct regular board meetings with detailed minutes, maintain accurate cap table templates reflecting all equity events, provide investor reporting per the Investors' Rights Agreement, ensure continuous regulatory compliance, protect IP proactively, manage contract renewals, monitor financial health including burn rate and runway, and prepare systematically for future fundraising rounds like Series B by maintaining an organized data room and current diligence checklists.

How does Series A affect the responsibility and decision-making authority of the founder CEO?

Series A typically introduces investor board seats and protective provisions requiring investor approval for major decisions. While the founder CEO often retains operational control and day-to-day responsibility, significant actions like raising additional capital, selling the company, or incurring major debt require board consent. Understanding these governance changes and managing stakeholder communication becomes a critical founder CEO responsibility in VC-backed startups.

What systems should startups implement to track KPIs and growth metrics post-Series A?

Implement robust financial and operational tracking systems capturing revenue growth rate, burn rate, runway, customer acquisition cost, LTV/CAC ratio, user numbers, NPS score, viral coefficient, gross margins, sales cycle metrics, and product usage KPIs. Use professional valuation software and analytics platforms to monitor these growth metrics in real-time, enabling data-driven decisions and transparent investor reporting that builds confidence for future fundraising rounds.

Important Legal Notice

This article is provided for informational and educational purposes only and does not constitute legal advice. The information contained herein is general in nature and may not reflect the most current legal developments or apply to your specific circumstances. Laws and regulations governing venture capital financing, corporate governance, intellectual property, employment, data privacy, and securities vary by jurisdiction and are subject to change.

No Attorney-Client Relationship: Reading this article or using any information provided does not create an attorney-client relationship between you, your company, and Allied Venture Partners, LLC, its authors, employees, or affiliates. This guide should not be relied upon as a substitute for professional legal counsel tailored to your specific situation.

Seek Qualified Legal Counsel: Series A funding rounds involve complex legal agreements, significant financial commitments, and terms that can profoundly impact your company's future and your personal interests as a founder. We strongly recommend that you engage experienced legal counsel specializing in venture capital transactions and startup law before:

Entering into any negotiations with potential investors

Signing term sheets or letters of intent

Conducting or responding to due diligence requests

Executing any definitive investment agreements

Making material changes to your corporate structure or governance

Qualified law firms with expertise in venture capital financing can provide advice specific to your company's stage, industry, jurisdiction, and unique circumstances. They can identify risks, negotiate favorable terms, protect your interests, and ensure compliance with all applicable laws and regulations.

No Guarantees: While Allied Venture Partners, LLC strives to provide accurate and current information, we make no representations or warranties regarding the completeness, accuracy, reliability, or suitability of the information contained in this article. The use of this information is at your own risk.

Limitation of Liability: Allied Venture Partners, LLC, its officers, employees, affiliates, and content contributors shall not be liable for any damages, losses, or consequences arising from your use of or reliance on the information in this article.

For specific legal guidance on your Series A funding round, corporate governance, intellectual property protection, employment matters, regulatory compliance, or any other legal issues affecting your startup, please consult with qualified legal professionals in your jurisdiction.