The Power Law of Angel Investing: How to Spot the Top 2%

Key Takeaways

Customer calls: Speak directly with two to five current or churned customers. Their candor about the product's real value (and its gaps) surfaces signal that no pitch deck will reveal.

Technical audits: For software companies, a lightweight code review or architecture assessment flags scalability concerns and hidden technical debt before they become your problem.

Cap table hygiene: Messy ownership structures, missing SAFEs, or poorly documented equity create downstream problems at Series A and beyond.

Do the diligence: Minimum 20 hours per deal. Evaluate the market, the model, the competitive dynamics, and most critically, the team's capacity to learn and adapt under pressure.

Build for the Power Law: A portfolio of at least 25 companies isn't over-diversification; it's the statistical minimum required to give your winners room to compensate for the inevitable losses.

The Statistical Reality of Early-Stage Software Investing

Venture capital returns don't follow a bell curve; they follow a power law, and that distinction changes everything about how angel investing works.

Most asset classes reward diversification across average performers. Early-stage software investing does not. According to a study by Correlation Ventures, approximately 50% of all venture capital returns are generated by the top 2% of companies. The rest of the portfolio (i.e., every modest exit, every slow-growth outcome) contributes relatively little to total returns.

A 2x return feels like a win. In an angel portfolio, it's often a failure. When you factor in illiquidity, the time value of capital over a five-to-ten-year holding period, and the opportunity cost of a check that could have gone into a breakout company, a 2x outcome barely keeps pace. The math only works if a small number of investments return 50x, 100x, or more — not if the entire portfolio trends toward safe mediocrity.

This is where the "spray and pray" approach of writing small checks into many startups with minimal diligence breaks down. Volume without selection discipline doesn't capture the power law; it dilutes it. What separates consistently successful angels from those who quietly exit the asset class is the ability to identify the rare companies with genuine outlier potential before the broader market prices them correctly.

Understanding this asymmetry is foundational. How you structure your investment vehicle, whether as a solo angel, traditional fund, or venture syndicate model, shapes whether you can even access that 2%.

Angel Investing vs. Venture Capital: Choosing Your Vehicle

The structural gap between angel investing vs venture capital is wider than most new investors expect, and choosing the wrong vehicle quietly kills returns before a single check clears.

The core difference comes down to whose money is at work. Venture capitalists manage pooled capital from institutional limited partners and carry formal fiduciary duties to those LPs. Angels deploy their own personal capital, which means faster decisions but also full personal exposure to every loss.

That independence sounds appealing. In practice, it creates a real adverse selection problem. Solo angels rarely see the same deal flow as institutional funds. What typically happens is that the strongest Seed rounds get anchored by established networks first, and unaffiliated angels inherit whatever's left: the rounds that institutional investors already passed on. Research from Rock Health and Stanford Graduate School of Business confirms that sourcing deals through a curated network or syndicate measurably increases deal quality compared to unsolicited cold outreach.

"The syndicate model gives individual angels institutional-grade access — without requiring institutional-scale capital commitments."

That's the structural advantage of the venture syndicate model: pooled due diligence, shared access to operator networks, and co-investment alongside experienced lead investors who've already vetted the round. Allied Venture Partners extends this further by removing the traditional barrier of membership fees, making curated deal flow genuinely accessible to accredited angels.

Understanding how the vehicle works sets the foundation for the next critical question: who's actually worth backing once you're inside a high-quality deal?

The Learning Machine: Evaluating the Modern Founder

Founder quality is the single most predictive variable in early-stage investing, and angel investing start to finish begins and ends with getting this evaluation right.

The "brilliant jerk" archetype is a persistent myth. A high-IQ founder with low coachability is actually a liability at the Seed stage, where the product thesis shifts constantly, and the ability to absorb feedback determines survival. The more reliable signal is adaptability: founders who hold their vision tightly but update their tactics rapidly.

Naval Ravikant captured this precisely: "The best founders are 'learning machines' who possess a unique combination of stubbornness on the vision and flexibility on the details." That tension between conviction and openness is what separates founders who scale from those who stall.

Team structure matters just as much as founder psychology. According to the Startup Genome Report, startups with two or more founders raise 30% more investment and grow their customer base nearly 3x faster than solo founders. A solo founder isn't an automatic disqualifier, but it's a statistical red flag that demands a stronger explanation — usually in the form of an exceptionally deep operator network or domain moat.

When evaluating whether a team can scale from Seed to Series A, look at how they've already responded to adversity. Have they pivoted product scope without losing the core insight? Have they recruited people stronger than themselves? These aren't abstract qualities; they're observable patterns you can screen for through structured reference checks and customer conversations.

That last point is worth sitting with. Most evaluation failures aren't failures of access; they're failures of process. Which is exactly why the depth of diligence you bring to a deal shapes your outcomes more than almost any other factor.

The 20-Hour Rule: Why Diligence is the Only Alpha

Gut feel is not a strategy. Angels who spend at least 20 hours on diligence per deal generate returns 5.9x higher than those who spend less, according to research from Willamette University and the Angel Resource Institute. That single data point should reframe how every investor thinks about what angel investors look for before writing a check.

The myth of the instinctive angel investor persists because a handful of high-profile angels built their reputations on early pattern recognition. In practice, those same investors conducted rigorous, if informal, due diligence (they just made it look effortless). Skipping the work doesn't sharpen your instincts; it exposes your portfolio to entirely avoidable risk.

Professional-grade diligence has three components:

Customer calls: Speak directly with two to five current or churned customers. Their candor about the product's real value (and its gaps) surfaces signal that no pitch deck will reveal.

Technical audits: For software companies, a lightweight code review or architecture assessment flags scalability concerns and hidden technical debt before they become your problem.

Cap table hygiene: Messy ownership structures, missing SAFEs, or poorly documented equity create downstream problems at Series A and beyond.

The primary constraint is time. Most individual angels can't sustain 20-hour deep dives across a diversified portfolio, which is precisely why syndicates matter. A well-structured lead investor distributes the diligence workload across a network, so each member benefits from collective analysis without carrying the full burden alone.

Of course, a rigorous process is still no guarantee against a different kind of failure: the psychological one. Even the most methodical investors can be derailed by social pressure and fear of missing out, which is exactly what the next section addresses.

Avoiding the FOMO Trap: Psychological Biases in 2026

Cognitive bias is one of the most underestimated risks in early-stage investing, and for those exploring angel investing for beginners, it's rarely covered with the seriousness it deserves.

Social proof is a lagging indicator, not a signal of future returns. According to Harvard Business Review, cognitive biases like FOMO and social proof regularly lead angels to overvalue startups that already carry high-profile backers — meaning by the time a deal looks "safe," the best entry valuation has almost certainly passed.

The psychology behind a "hot round" is seductive. When a well-known lead investor is already in, the instinct is to treat their participation as validation. In practice, what it often signals is that price discovery has already happened (and not in your favor). Oversubscribed rounds compress future exit multiples before a single line of product ships.

Maintaining objectivity when deal pressure is high requires separating signal from noise. A useful discipline is returning to the diligence framework covered earlier: does the founding team demonstrate the learning velocity and market insight that justify the valuation, independent of who else is writing a check? If the answer isn't clear from fundamentals, the momentum itself becomes the thesis, which is a fragile foundation.

For angels navigating cross-border deal flow, social proof bias is amplified by geography. For example, a name-brand US lead VC can obscure weak unit economics in a Canadian market context.

Getting entry valuation right matters more than most angels acknowledge early on. That discipline connects directly to the next challenge: how many bets you need to place for the math to work in your favor.

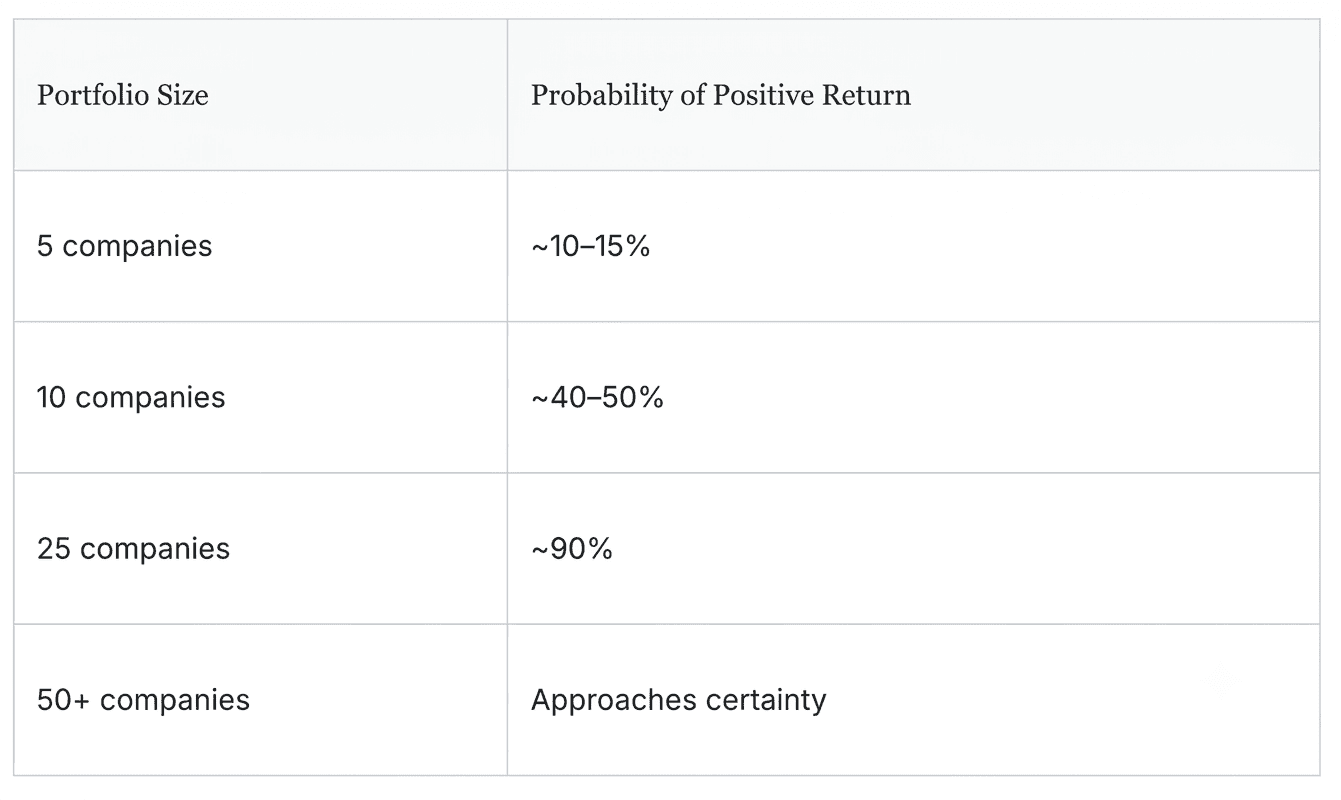

Portfolio Construction: The 25-Company Minimum

A portfolio of fewer than 10 companies isn't a diversified angel strategy; it's a concentrated bet against a power law that's stacked against you.

The math is unforgiving. In early-stage software investing, the majority of companies will return less than the capital invested. A portfolio of 5–10 companies almost certainly includes no breakout winner, which means the entire portfolio trends toward zero. The Techstars/Kauffman Foundation research makes the threshold clear: angels need a minimum of 20 to 25 investments to achieve a 90% probability of a positive return.

The logic behind the 25-company number is straightforward. Because a single outlier can return 20–50x and cover the entire portfolio's losses, you need enough shots on goal to statistically capture at least one. Spreading across 25 deals isn't about lowering conviction; it's about giving the power law room to work in your favor.

Capital allocation matters as much as deal count. A practical approach is to reserve 30–40% of your total angel budget for follow-on rounds in your top performers, rather than deploying everything into initial checks. This lets you double down on companies showing early traction without being shut out of their next round. Syndicates can help here by pooling capital through structured vehicles, which lets you maintain pro-rata rights at check sizes that would otherwise be inaccessible.

Finally, reset your time horizon. Angel investing is a 7–10 year commitment per company, not a 2-year flip. Liquidity events like acquisitions and IPOs happen slowly at the early stage. Building the right portfolio takes patience, and so does harvesting it. Once you've structured for the long game, the next question becomes how to extract more value than just capital from each position you hold.

Smart Capital: Increasing Your Value Post-Check

Writing a check is the entry point, not the finish line. The angels who generate outsized returns treat their capital as a credential, not the contribution.

As Reid Hoffman observed, "Your value as an angel isn't just your check; it's your ability to provide 'smart capital' through customer introductions, recruiting, and follow-on funding strategy." That framing redefines the entire role. Silent partners who wire funds and wait occupy the weakest position on a cap table. Value-add investors who open doors occupy the strongest.

The practical levers are specific. In practice, the most impactful angels focus on three areas: recruiting (making warm introductions to senior engineering or GTM talent), customer introductions (connecting founders to decision-makers inside enterprise accounts), and Series A prep (coaching founders on what institutional investors actually scrutinize in due diligence). Each of these compounds the initial investment rather than simply waiting for the market to do it.

The best founders understand this dynamic intuitively. They frequently optimize for the network density of the cap table over a marginally better valuation, because a well-connected $500K round can unlock a $5M Series A faster than a clean term sheet from a passive check-writer. The right angel network amplifies this effect substantially.

A syndicate structure extends what any single angel can deliver. Where one investor might have recruiting relationships in one vertical, a curated syndicate brings cross-sector operator networks, shared diligence infrastructure, and collective follow-on capacity. That's the accessible venture capital model Allied Venture Partners is built around: pooling operator expertise alongside capital so founders gain a network, not just a wire.

Putting all of these principles together, including portfolio construction, bias management, and active value creation, points toward a clear operational framework for long-term angel success.

The Bottom Line: A Framework for Angel Mastery

Angel investing rewards discipline over intuition. The angels who generate outsized returns follow a repeatable framework, not a lucky instinct.

The research is clear: committing at least 20 hours of diligence per deal is associated with a 5.9x return multiplier compared to deals where investors cut that process short. That's not a soft suggestion; it's the single most actionable lever available to any angel who wants to move from average to exceptional.

Here's the framework distilled into four principles:

Do the diligence. Minimum 20 hours per deal. Evaluate the market, the model, the competitive dynamics, and most critically, the team's capacity to learn and adapt under pressure.

Build for the Power Law. A portfolio of at least 25 companies isn't over-diversification; it's the statistical minimum required to give your winners room to compensate for the inevitable losses.

Back multi-founder teams. Solo visionaries are high-variance bets. Multi-founder teams with complementary skills and 'learning machine' mentalities consistently outperform across early-stage investment data.

Plug into curated deal flow. Sourcing quality deals independently is slow and inconsistent. A syndicate model, structured around shared diligence and operator networks, closes that gap efficiently.

What You Need to Know: The angels who fail aren't less intelligent — they're less systematic. Portfolio size, diligence depth, team selection, and deal-flow quality are the four variables that separate the top 2% from everyone else.

Putting this framework into practice requires more than good intentions; it requires infrastructure. That's where the right network becomes a genuine competitive advantage, and it's exactly what the next section covers. If you're ready to stop piecing together deal flow on your own, learn how we're structured to support accredited investors at every stage of that process.

Professionalizing Your Deal Flow with Allied Venture Partners

The syndicate model directly addresses the two gaps that cause most angels to fail: access to quality deal flow and the capacity to evaluate it rigorously. Solo investors often struggle to source consistently and rarely have the operator context needed to stress-test a founder's assumptions. A structured syndicate solves both problems at once.

Allied Venture Partners operates on exactly this premise. As one of Canada's largest angel investor networks, the platform connects accredited investors to curated North American software deals at the Seed and Series A stage (without charging membership fees). That fee-free structure removes a friction point that keeps many qualified investors on the sidelines, making accessible venture capital a practical reality rather than a tagline.

The deal-flow process is deliberate, not passive. Allied Venture Partners evaluates software and technology companies through a data-driven evaluation process, so the deals that reach investors have already cleared an initial screen for market size, team quality, and stage fit. Investors can build a diversified early-stage portfolio without having to build their own sourcing infrastructure from scratch.

For founders, the path is equally direct. The Pitch Us portal gives early-stage software companies a fee-free way to get in front of a diverse operator network and a pool of aligned capital — no gatekeepers, no upfront cost.

Whether you're an accredited investor looking for curated deal flow or a founder ready to raise your Seed or Series A round, Allied Venture Partners provides a clear on-ramp. Submit your pitch or join the syndicate now to put the frameworks covered in this article to work with a network built for exactly this stage.

Frequently Asked Questions

What is the power law in angel investing, and why does it matter?

The power law describes the highly skewed distribution of returns in early-stage investing: approximately 50% of all venture capital returns are generated by the top 2% of companies. This means a small number of breakout investments must carry an entire portfolio. Unlike traditional asset classes where diversification across average performers works, angel investing only generates strong returns if you can identify and access genuine outliers — and hold enough positions to capture them statistically.

How is angel investing different from venture capital?

The core structural difference is whose capital is at work. Venture capitalists manage pooled institutional funds with formal fiduciary duties to their LPs, while angels deploy personal capital with faster decision-making but full personal exposure to losses. The more practical difference is deal flow quality: solo angels frequently encounter adverse selection, inheriting rounds that institutional investors have already passed on. Syndicates close that gap by providing pooled diligence, operator networks, and co-investment alongside experienced lead investors.

How many investments do I need to make the math work?

Research from Techstars and the Kauffman Foundation puts the minimum at 20 to 25 companies to achieve a 90% probability of a positive return. A portfolio of 5 to 10 companies is statistically unlikely to include a breakout winner, which means the entire portfolio trends toward zero. The 25-company threshold isn't about lowering conviction — it's about giving the power law enough room to work in your favor.

How much time should I spend on due diligence per deal?

Research from Willamette University and the Angel Resource Institute found that angels who spend at least 20 hours on diligence per deal generate returns 5.9x higher than those who spend less. Effective diligence covers three areas: direct customer calls (two to five current or churned customers), a technical audit of the product architecture, and a review of cap table hygiene to catch structural issues before they become problems at Series A.

What makes a strong founding team at the early stage?

The most reliable signal is adaptability — founders who hold their vision tightly but update their tactics quickly in response to new information. The Startup Genome Report found that startups with two or more co-founders raise 30% more investment and grow their customer base nearly three times faster than solo founders. Solo founders aren't automatic disqualifiers, but they represent a statistical red flag that demands a stronger compensating factor, such as an exceptionally deep operator network or domain expertise.

What is "smart capital" and how does it affect my returns?

Smart capital refers to the non-financial value an angel brings to a portfolio company beyond the initial check — including recruiting introductions, connections to enterprise customers, and coaching on Series A readiness. The strongest cap tables are built around network density, not just dollar amounts. Well-connected angels can accelerate a company's path to its next institutional round in ways that a passive check-writer simply cannot.

How does FOMO affect angel investing decisions?

Social proof is a lagging indicator, not a forward-looking signal. By the time a round looks "safe" because a high-profile lead investor is already in, price discovery has typically already happened at a valuation that compresses your future exit multiple. The discipline that counters FOMO is returning to fundamentals: does the team's learning velocity and market insight justify the valuation on its own merits, independent of who else is writing a check?

What is a venture syndicate and how does it help individual angels?

A venture syndicate pools capital and diligence resources from multiple accredited investors around a curated deal flow, led by an experienced lead investor who has already vetted the round. This gives individual angels access to institutional-grade deal quality without requiring institutional-scale capital commitments. Syndicates also distribute the 20-hour diligence workload across a network, preserve pro-rata rights at otherwise inaccessible check sizes, and provide collective follow-on capacity for top performers.

Disclaimer: This article is provided for general informational and educational purposes only and does not constitute legal, financial, investment, tax, or professional advice of any kind. Allied Venture Partners LLC makes no representations or warranties regarding the accuracy, completeness, or currentness of this information, which is subject to change without notice. To the fullest extent permitted by law, Allied Venture Partners LLC, its affiliates, officers, directors, employees, and agents expressly disclaim all liability for any direct, indirect, incidental, consequential, special, or punitive damages arising from your use of or reliance on this content, including but not limited to any securities offerings, capital raises, regulatory compliance issues, enforcement actions, financial losses, or business damages. Securities laws are complex, fact-specific, and vary by jurisdiction. You are solely responsible for ensuring compliance with all applicable federal and state securities laws and should consult with qualified legal counsel, financial advisors, and tax professionals licensed in your jurisdiction before making any decisions or taking any actions based on this information. By accessing or using this article, you acknowledge that you have read and understood this disclaimer, assume all risks associated with your use of this information, and agree to indemnify and hold harmless Allied Venture Partners LLC from any claims arising from your use of this content.